Welcome to Smart Money! My name is Eric Fry, and I’m glad you’re here.

Wall Street has sold investors on the idea that they should start with “micro” analysis – the idea that they should make investment decisions by comparing things like price/earnings ratios, income statements, or other company details.

But I do the opposite. I start with “macro” analysis.

I look for big-picture trends that drive huge, multiyear moves in entire sectors of the market.

I’m talking about trends that can spin off dozens of triple- and even quadruple-digit gains in just a few years.

Catching just one of these trends – at the right time – can help anyone accumulate enough capital to finance their dreams and an enviable retirement…

When investors use a global macro strategy, they identify investment opportunities from a broad, global, top-down perspective, rather than by examining stocks one by one (a micro, bottom-up perspective).

And today, I want to highlight my Top 7 Stocks for 2026, each of which capitalizes on a powerful megatrend.

Let’s get started…

Top 2026 Stock No. 1: Freeport McMoRan

Freeport-McMoRan Inc. (FCX) is the world’s largest copper miner. The terms “copper miner” and “artificial intelligence” do not obviously relate to one another. But in the case of Freeport, they do.

Freeport has been using a machine-learning model at its Bagdad copper mine in Arizona to boost production. This model uses data from sensors around the mine to “tailor” the ore-processing method to each of the seven distinct types of ore that come from the mine.

The company has found success with AI at Bagdad, and down the road, Freeport’s AI technology could enable the company to tackle more complex projects, and to extract value from places where its competitors cannot. That advantage could become incredibly valuable in a world that’s starving for metals like copper.

Though recently, despite copper and gold prices flirting with all-time highs, Freeport stock has been narcoleptic.

The cause of Freeport’s underperformance is no mystery. A massive mudslide inside its Grasberg copper-and-gold complex in Indonesia killed seven workers and forced an immediate shutdown. This awful tragedy also delivered a serious financial shock. Production dropped sharply, and the company took a well-publicized reputational hit.

With the cause understood, the fix underway, and the production recovery path mapped out, investors can finally treat the event for what it is: a horrible but temporary setback.

And that means Freeport can once again be valued on what it really is – a premier copper-and-gold producer, positioned in front of a decade-long supply squeeze.

To better understand the stock’s potential from the current price, it helps to step back and take a look at the big picture.

The Copper Supercycle Is Here

Copper has always been the wiring of the world. But suddenly, the world is demanding more wiring than it has at any point in history. Every macro trend that feels futuristic, electrified, digitized, or decarbonized runs straight through a fat bundle of copper.

- Power grids and data centers. The International Energy Agency (IEA) expects U.S. electricity demand to grow around 2% per year from 2025 to 2007, roughly double its previous forecast, as AI data centers, semiconductor fabs, and other large industrial loads connect to the grid.

- U.S. utilities. According to Morningstar and the Edison Electric Institute, utilities are now planning roughly $1.4 trillion of grid and generation capex between 2025 and 2030 — about twice what they spent in the prior decade — as they race to add transmission, substations, and firm capacity for this new load.

- AI and cloud computing. A modern hyperscale data center is essentially a copper-and-aluminum exoskeleton wrapped around racks of silicon. These facilities consume enormous volumes of copper wiring, busbars, and switchgear. Estimates suggest data centers alone could require hundreds of thousands of tonnes of copper per year by 2030, with individual AI-focused hyperscale facilities consuming up to 50,000 tons each.

- Electric vehicles and renewables. EVs use roughly two to three times as much copper as internal-combustion vehicles once you count motors, inverters, and charging networks. Wind, solar, and battery installations are even more copper-intensive on a per-megawatt basis than traditional generation. Layer on microgrids, distributed generation, and 5G towers, and you get a steadily expanding, globally diversified demand base.

Not surprisingly, the copper market is tilting toward long-term deficits. The International Copper Study Group (ICSG) expects today’s refined-copper balance to flip into a deficit of roughly 150,000 tonnes next year, as mine production growth slows and concentrate availability tightens. UBS anticipates an even larger deficit of 400,000 tonnes.

Copper is one of the most vulnerable links in the global supply chain for the energy transition and AI build-out. Without more than $200 billion of new investment, the world simply won’t have enough copper. For context, Wood Mackenzie estimates that total copper-mining investment over the past six years reached only about $76 billion.

So, the short-term story is simple; demand is growing faster than expected, supply is growing slower than expected, and the market is already slipping into deficit.

Right Place, Right Time

Freeport is maximizing this opportunity by boosting copper production in every way possible. For example, the company has developed cost-effective methods for extracting commercial quantities of copper from waste rock through advanced leaching techniques.

Freeport expects to produce about 300 million pounds of copper from this source in 2026, then ramp production to 800 million pounds by 2030. That level of production would drop about $1.6 billion to the bottom line – roughly 20% of current pre-tax income.

Importantly, these sizeable incremental profits amount to “found money.” They come from mine stockpiles that had been considered worthless until recently. Altogether, the stockpiled material at all of Freeport’s copper mines contains about 39 billion pounds of copper – all of which was “unrecoverable” by traditional leach methods.

Also a Gold Stock — A Really Good One

Freeport also carries an enormous amount of “hidden” gold leverage. Investors treat the company as a pure copper proxy, but the company also ranks as a major gold producer. In the most recent quarter, FCX produced nearly 300,000 ounces of gold, and its realized pricing was nearly $1,000 an ounce higher than the prior year – from $2,262 to $3,123. The gold price has jumped another $1,000 since the end of the third quarter!

Every $100 move in the gold price equals roughly $150 million in annual EBITDA. Therefore, if gold continues trending toward $5,000, it would provide a powerful secondary tailwind to Freeport’s already-expanding cash flow.

Freeport expects to generate around $12 billion of EBITDA in 2026, a transition year while Grasberg production is still in recovery mode. But assuming copper and gold prices remain close to where they are today, that figure could rise above $17.5 billion per year by 2027. At that level of profitability, the stock would be trading for less than four times 2027 EBITDA – about one-third the current valuation of the S&P 500 Metals & Mining Sub-Index.

This depressed valuation offers an attractive opportunity to capitalize on a temporary dislocation. Freeport’s world-class Grasberg mine stumbled just as copper and gold began pressing toward record highs.

Top 2026 Stock No. 2: Alcoa

If power is the blood circulating through data center infrastructure, metals are the bones.

In effect, every ton of metal pulled from the ground is a claim on the AI buildout.

Unlike software-as-a-service (SaaS) vendors or chip designers, metals companies don’t need to guess which AI model wins or which agent framework dominates. They just need to deliver the raw materials that make the entire ecosystem possible.

Aluminum demand is accelerating. Every high-voltage line that feeds an AI data hub consumes one to two tons of aluminum per megawatt delivered. Each new stretch of long-distance transmission deepens the world’s appetite for this versatile metal. From 104 million tons of demand in 2024 to an estimated 120 million by 2030, global aluminum consumption is set to grow almost as relentlessly as copper’s.

That spells good news for Alcoa Corp. (AA), the largest U.S.-based aluminum producer.

Toward the end of 2025, Alcoa’s prices reached a new three-year high. After suffering a tariff-induced selloff earlier in the year, Alcoa’s shares have been trending higher, and I expect that uptrend to gain momentum – driven not only by firmer aluminum prices, but also by the company’s exceptional fundamentals.

Alcoa is not just the largest American aluminum producer, but it is also among the world’s most environmentally progressive. Producing aluminum requires immense amounts of electricity, and that energy intensity is reshaping the industry.

Increasingly, companies such as Tesla Inc. (TSLA) are seeking to source their aluminum from clean-energy smelters powered by hydro, nuclear, or renewables. That shift is elevating low-carbon producers like Alcoa and Norsk Hydro ASA (NHY) to the top tier of the aluminum world.

Today, renewable energy powers roughly 87% of Alcoa’s smelting operations and about 70% of Norsk Hydro’s. This alignment with the global push toward decarbonization gives both companies a durable strategic advantage, and positions them not merely as metal producers, but as critical enablers of the cleaner, more electrified world AI will depend on.

In the end, the market may reward not those who build the virtual world, but those who power it. The data revolution will always need its dreamers, but it will depend on the miners that turn metal into the blood and bones of artificial intelligence.

In the race for AI supremacy, the hyperscalers may scorch their balance sheets, but the miners will still be cashing the checks. While hyperscaler shareholders wrestle with wafer-thin cash cushions and swelling debt, the power and metals firms operate with clearer economics.

Their business models are not theoretical. They are measurable and proven.

They don’t need to care whether GPT-7 outperforms Gemini Ultra or whether OpenAI’s next model hallucinates less than Anthropic’s. They get paid every time a new data hall lights up, every time another transformer hums, every time a ton of copper vanishes into a conduit.

Therefore, for investors seeking exposure to the AI Revolution without betting on which version of intelligence wins, a mining company like Alcoa offers a compelling opportunity.

Top 2026 Stock No. 3: Savers Value Village

Thrifting is “all the rage” among Generation Z. Two out of five items in the average zoomer’s closet are secondhand.

That’s the first reason to consider investing in Savers Value Village Inc. (SVV), but far from the only one. As the largest “for-profit” thrift store operator in North America, the company is perfectly positioned to capitalize on the Gen Z thrifting phenomenon.

Savers Value Village didn’t simply bolt a thrift operation onto a traditional retail model. It has specialized in thrifting since 1954, when founder William Ellison opened the first Savers store in San Francisco. The idea was radical for the time: partner with local nonprofits to collect donations, pay them for the goods, and then sell those goods in a clean, organized retail environment.

For decades, the company quietly grew under private ownership – expanding across the U.S., into Canada, and eventually into Australia – while perfecting the operational model. The stores never looked like the musty thrift shops of old. They looked like real retailers: wide aisles, sorted racks, organized departments.

By the 1990s and 2000s, Savers had become the largest for-profit thrift chain in North America, with a business model that turned donations into both community funding and shareholder returns.

Today, Savers Value Village runs 300-plus stores across the U.S., Canada, and Australia, is staffed by 22,000 team members, and processes billions of pounds of donated goods annually. What looks simple on the sales floor is the product of 70 years of supply-chain engineering.

To support its business, Savers has built one of the most creative and durable sourcing models in retail. For example, the company pairs nearly every Savers store with a Community Donation Center (CDC).The company’s nonprofit suppliers use these on-site donation centers to drop off used clothes, shoes, books, and household goods.

Unlike charities that simply accept items, Savers pays its suppliers by the pound for these donations. As a result, local charities get steady funding without the overhead of running stores, while Savers secures a consistent stream of inventory.

In select markets, Savers supplements CDCs with GreenDrop donation stations. These freestanding pods or trailers extend the network and make donating easier.

After Savers collects these donations, its employees sort, price, and rack the sellable items. Merchandise hits the floor fast and cycles through quickly. Products that don’t sell at retail are bundled and resold into the global wholesale reuse market. That “multi-exit” monetization process converts “waste” into incremental revenue.

This model means Savers doesn’t rely on closeouts or liquidation deals. It owns its supply chain, from the donation bin to the cash register. That’s why it can keep prices dramatically below discount retail – 40% to 70% lower, according to management’s checks.

The Moat: Industrial-Scale Treasure Hunting

Thrifting has always been about the “hunt.” What Savers Value Village has done is industrialize the hunt without killing the fun.

- Frequency and freshness. Savers cycles through its inventory about 15 times a year, which is an extraordinarily rapid rate. That’s nearly double Walmart Inc.’s (WMT) inventory turn and about five times faster than Lululemon Athletica Inc.’s (LULU). Effectively, Savers offers entirely new merchandise every three weeks.

- Scale married to local tailoring. With hundreds of stores, the company can apply data through its 6-million-member loyalty program to optimize assortment, flow, and seasonality at the local level. It can backstock off-season goods, drip them out at the right time, and flex floor space to match neighborhood demand.

- Multi-monetization. Unsold inventory isn’t a liability. The company exports, recycles, or wholesales it to create an incremental revenue stream, while also keeping landfill diversion part of its brand story.

- Brand halo. Because Savers funds local nonprofits, the firm operates with a built-in community goodwill advantage compared to traditional clothing retailers. Every drop-off becomes a story about supporting charity and sustainability – soft power that purely commercial resale apps don’t have.

- Capital efficiency. New stores are highly accretive. Each new store generates 15% to 20% profit margins, on a stand-alone basis.

Taken together, these elements create a moat that few competitors can cross. Traditional retailers can bolt on “resale corners,” but they can’t replicate Savers’ 70-year infrastructure of donations, partners, and processing know-how.

Given Savers’ business model, there’s plenty of room for the company’s growth to accelerate. In its most recent quarter, for example, U.S. same-store sales soared 6%, which is double or triple the growth rate of most clothing retailers.

Looking ahead, the company should benefit from several factors.

- Because Savers operates fewer than 400 stores in North America, it has massive expansion potential across the U.S. and Canada. Many mall landlords court them as anchor tenants.

- The thrift supply chain is tariff-free, which means Savers does not need to waste precious resources absorbing tariff expenses or trying to rejigger its supply chain.

- Savers finds itself in the right place at the right time. Gen Z has embraced thrifting because it is affordable, unique, and sustainable. Capital One Shopping reports that 83% of zoomers have purchased or are interested in purchasing secondhand.

Not surprisingly, the secondhand clothing market is growing five times faster than the overall apparel industry. According to ThredUp, the U.S. secondhand market grew 14% in 2024, compared to just 3% for the broader apparel market. Online resale was even stronger – up 23%. Analysts expect the U.S. resale market to nearly double by 2029, reaching roughly $40 billion.

That’s not a niche. That’s an empire in the making.

Savers is on track to earn about $0.50 per share next year, and $0.65 per share in 2027. That steady growth rate would give the stock a valuation of 25 times 2026 earnings and 20 times the 2027 result.

Although this valuation is not the “deep discount” variety you might find on the racks of a Savers store, it is below the sector average. Further, if the company accelerates its expansion plans and/or boosts its profit margins as much as I anticipate, earnings could surprise on the upside.

Top 2026 Stock No. 4: Yeti

Yeti Holdings Inc. (YETI) may be the ultimate non-AI stock – a brand that celebrates everything artificial intelligence cannot replicate: the physical, the analog, the sensory, the real.

When you buy a Yeti product, you aren’t buying an algorithm or a convenience; you’re buying a campfire under the stars, beers that stay cold all weekend, and the quiet assurance that your cooler can outlast a grizzly.

And it works.

The brand flourished during the pandemic and its immediate aftermath, when the outdoors became both refuge and recreation. But as life returned to “normal,” consumers drifted back to indoor habits, and Yeti’s sales softened. Its stock followed suit. From a high of $108 in late 2021, the stock tumbled to a low of $26.61 earlier this year. But a powerful and sustainable turnaround may be underway.

Looking ahead to 2026 and beyond, five important factors could produce a meaningful profit rebound, potentially making Yeti a timely stock to own today…

1) New Product Launches: Re-Energizing the Core

One of Yeti’s most compelling potential catalysts is its increasingly vigorous product engine. The company has shifted from incremental tweaks to a rapid cadence of innovation. It launched more than 30 new products this year across drinkware, coolers, bags, packs, and outdoor gear lines.

2) International Sales Momentum: Unlocking a Growth Lane

Yeti is no longer just a U.S. niche brand. International markets are providing a vibrant new sales channel. Over the first half of 2025, year-over-year international sales rose 11% – driven by strong performance in Europe and early traction in Asia.

Management is targeting 15-20% growth in international for full-year 2025, and sees Asia as the key. If international can scale from today’s 18% revenue share toward 25%-30% over several years, growth will increasingly come from non-mature geographies that tend to produce higher profit margins than U.S. sales.

3) Tariff Headwinds Easing: A Structural Tailwind

Tariffs have caused a serious headwind for Yeti. But the company has responded by pivoting decisively away from China-based production. By the end of 2025, it expects fewer than 5% of its products will face tariffs tied to China.

4) Strong DTC & Channel Mix: High Margin & Control

One of Yeti’s biggest structural shifts is in channel mix. DTC sales via yeti.com, flagships, and customization rose 2% during the first half of the year and now account for a hefty 56% of net sales.

Thanks to DTC, Yeti has more control over pricing, inventory, margin capture, and brand experience. And because DTC is a margin engine, even if some categories struggle or sales soften, the business retains flexibility. The margin base is more resilient, cushioning volatility in wholesale or geography-specific pressure.

5) Strategic Partnerships & NFL Licensing: Brand Amplification

Brand strength and community are more than a vanity exercise. They translate directly into sales leverage. Yeti has aggressively extended its reach through events, content, and sports partnerships. In the second quarter alone, it hosted 70 global events like chef-led outdoor dinners and Stampede activations. Additionally, its “Yeti Presents” media arm (85 films, 33M views, 2.6M watch-hours) compounds brand pull beyond traditional commerce.

However, the most promising current partnership is its new NFL/Fanatics licensing deal. Yeti now offers licensed drinkware and coolers for all 32 NFL teams (and many MLB, NHL, NCAA programs), available across yeti.com, Yeti stores, wholesale, team/league sites, Fanatics.com, and live events. This sweeping partnership gives Yeti a massive new “sports fandom” distribution vector.

Putting the pieces together, here’s why Yeti strikes me as a timely, underappreciated opportunity…

- Re-accelerating growth. If new products and category diversification begin contributing meaningfully (bags, gear, food containers, shaker bottles), Yeti can escape its reliance on drinkware or soft coolers.

- International lift. A scalable international business mitigates cyclical risk in the U.S. and unlocks new growth zones.

- Margin compounding. As tariff drag fades and mix shifts toward premium items, margin expansion could drive outsized earnings leverage.

- Channel strength. A DTC-lean business gives more control, durability, and margin protection than a wholesale-only model.

- Brand moat via partnerships. The NFL/Fanatics deal gives Yeti a mainstream branding amplifier and distribution channel that few outdoor brands can match.

From a valuation standpoint, Yeti currently trades around 10 times gross earnings (EBITDA), which is less than half its median valuation level of the last six years. Therefore, if the business can prove a path back to 15% revenue growth with margin expansion, the stock could double from current levels.

Management itself is backing its optimism with company plans to repurchase $200 million in stock. Meanwhile, Yeti sits with a strong net-cash balance sheet, leaving room to invest in go-to-market, expansion, and innovation.

If Yeti achieves the growth recovery management expects, the stock should earn about $2.75 a share next year and $3.10 in 2027. At those levels of profitability, the stock would be trading for 15 times 2026 earnings and 14 times the 2027 result.

Those numbers tell a simple story: The market is still pricing YETI as if its best days are behind it, while management is operating as if the next chapter has already begun.

The gap between those two perceptions creates opportunity.

If Yeti merely executes on its stated plan – expanding internationally, widening its product canvas, rebuilding gross margins, and monetizing its new partnerships – the earnings power embedded in the business could surprise to the upside. The stock doesn’t need heroics; it just needs momentum and time.

As tariffs fade, new products proliferate, and NFL partnerships draw millions of new eyes, Yeti may once again prove that in an age of virtual everything, authenticity is still a growth industry.

Top 2026 Stock No. 5: PayPal

This titan of the digital payments industry traces its history to 2000, when Elon Musk merged his online bank, X.com, with Peter Thiel’s software company, Confinity, to form PayPal.

The merged entity started spinning gold almost immediately for Musk and Thiel, as the inventive pair sold the company to eBay just two years later for $1.5 billion.

Then in 2015, eBay spun out PayPal Holdings Inc. (PYPL) as a separately traded company, which it has remained ever since. (Interestingly, 2015 was also the year that Musk and Thiel partnered up again to form OpenAI, the company that would go on to create ChatGPT.)

During the last several years, the tally of active accounts on PayPal’s platform has swelled 63% to 435 million, while the annual volume of processed payments on its platform has doubled to a whopping $1.37 trillion.

PayPal’s dominant position in the “branded checkout” segment has powered most of that growth. The “PayPal/Venmo” checkout button you might see when shopping online is an example of that business. Around 80% of the top 1,500 retailers in North America and Europe feature PayPal in their digital wallets.

But PayPal is not taking its success for granted. The company is fortifying its market leadership by integrating leading-edge AI and machine-learning processes into key aspects of its operations. For example, the company uses AI to detect fraudulent transactions and to boost the approval rate of valid transactions.

Buy Now, Pay Later

PayPal’s growth strategy relies on three key initiatives…

- Strengthening its core “branded checkout” solution…

- Growing its “unbranded checkout” solution…

- And developing and integrating AI processes that increase merchant sales, boost customer “stickiness,” and/or reduce operating expenses.

Branded Checkout is the foundation of PayPal’s business because of its high-margin fee structure. This business segment accounts for about one-third of the Total Payment Volumes (TPVs) the company processes, but it produces more than half of its total revenues.

PayPal is the market leader in branded online checkout with 35 million merchants on that platform. Although the company does not possess the commanding 99% merchant acceptance rate of legacy credit card companies like American Express Co. (AMEX) and Mastercard Inc. (MA), it has the largest acceptance rate of any “alternative payment method” provider. This category of payment solutions includes direct debit transactions, prepaid debit cards, and eWallets like PayPal, Venmo, Google Pay, and Apple Pay.

In 2020, PayPal launched a new “Buy Now, Pay Later” (BNPL) feature to bolster the appeal of its branded checkout offering.

Since launching BNPL, PayPal has issued loans to nearly 30 million customers. In 2022 alone, PayPal processed more than $20 billion of BNPL loans – up 160% from the prior year.

PayPal’s momentum in this market should propel it to undisputed leadership… and that’s no small matter in a sector that is growing as rapidly as BNPL consumerism.

BNPL-financed transactions now account for more than $300 billion in transactions worldwide.

Unlike its competitors, which must win new business to establish a BNPL relationship with a merchant, PayPal can deliver BNPL capabilities as a “bolt-on” to an existing relationship.

PayPal simply incorporates BNPL functionality into the existing checkout protocol. It is not a “new sale.” PayPal added BNPL capabilities to its existing relationship with Microsoft Corp. (MSFT). Online shoppers at Microsoft’s Xbox Store can now access BNPL if they wish.

Prudently, PayPal is working to “externalize” these loans by selling them to a third party, rather than retaining them on their own balance sheet. By selling the loans, PayPal removes the risk of holding bad loans.

The company took a giant step forward toward achieving that goal when it struck a deal to sell up to €40 billion of BNPL loans to the global investment firm KKR.

Under the terms of the agreement, KKR acquired PayPal’s existing European BNPL portfolio, along with future originations of eligible BNPL loans. PayPal will continue to conduct all the customer-facing activities of the loans, including underwriting and servicing.

This major transaction not only removes a large dollop of credit risk from PayPal’s balance sheet, but it also frees up capital to accelerate BNPL originations in Europe and/or to conduct shareholder-friendly activities like buying back stock.

PayPal expects to generate about $1.8 billion in net proceeds from this transaction and states that it will use a portion of the proceeds to boost its 2023 share repurchase program to $5 billion. In 2022, the company repurchased $4 billion in stock, which reduced the share count by about 3%.

Paving the Way

Now, PayPal is getting ready to dominate a new market…

Agentic AI commerce.

Starting in 2026, OpenAI will integrate PayPal’s wallet and payment technology into ChatGPT’s “Instant Checkout” experience. This will allow users to complete purchases directly inside the chatbot.

PayPal controls the full checkout user interface and authentication flows. That means an AI agent can open sessions, request approval, store consent, and authorize transactions, all within a single session.

That makes it far easier to monitor AI agents and add appropriate guardrails. And if an AI makes an honest mistake, PayPal can easily reverse the transaction without going through merchant banks. It’s a one-stop payments shop.

In other words, agentic e-commerce will be a game-changing technology, even if the details are not yet fully known.

Perhaps the most remarkable aspect of PayPal today is its valuation.

The San Jose, California-based company is priced more like a zero-growth merchant bank than a fintech platform. A post-Covid slowdown in e-commerce spooked markets, and investors were concerned that PayPal had chased unprofitable businesses during the boom years.

This is an exaggeration of PayPal’s “demise.”

Over the next three years, analysts expect this fintech company’s revenues to grow 19% and its profits to rise 31%. And if AI agentic commerce truly takes off, we will see these growth numbers occur at an annual pace instead.

Top 2026 Stock No. 6: Dutch Bros

If you live in the Pacific Northwest, you probably know this company and have frequented one ofitsdrive-through coffee kiosks. If you live anywhere else in the U.S., you probably haven’t… but you will.

This Starbucks-like juggernaut from Grants Pass, Oregon. got its start in 1992 when a couple of brothers opened an espresso-vending pushcart down by the railroad tracks in the downtown area.

Since then, Dutch Bros Inc. (BROS) has opened nearly 900 stores across 17 states. But the company’s new CEO, Christine Baron, a former VP from Starbucks Corp. (SBUX), has plans to expand the company’s U.S. footprint to more than 4,000 stores over the next 10 years.

If you read a Reddit message board about this company or talk to anyone who frequents one of its stores, you realize quickly that Dutch Bros is not merely a place to buy coffee to go. It is a destination.

Its product offerings and overall vibe elicit the same sort of cultlike devotion that Chick-fil-A or In-N-Out Burger do.

Dutch Bros is especially popular with the millennials and Gen-Zers who tend to buy highly customized, sweet coffee drinks, and/or energy drinks. The company offers a wide array of both, including the company’s own “signature” energy drink called “Rebel.”

The company’s formula for success is working. As the chart below shows, its same-store sales have been trending sharply higher, while Starbucks’ have been sliding lower.

In fact, many high-profile companies in the quick-serve restaurant space are suffering from declining or sluggish sales trends.

Looking ahead, Dutch Bros will pull two main levers to generate rapid growth…

- Expansion. This process is already well underway. The company has opened at least 30 new stores each quarter for 11 straight quarters. In the first quarter of 2024, it ramped that tally to 45 new stores, including its first-ever openings in Florida. Additionally, Dutch Bros is planning to open stores in four new cities in the U.S.

- Mobile ordering. Incredibly, mobile ordering has not been part of the Dutch Bros growth story. Instead, it generates about 90% of sales from “old-school” drive-through or walk-up ordering. The company added mobile order-ahead functionality to its app in 2024, which sets the stage for a potential sales boost per unit.

Every decade, a “magical” restaurant-based firm seems to appear. McDonald’s… Starbucks… Subway… Panda Express… these brands seem to grow like wildfire.

On the fundamental level, popular food service companies succeed simply because people like the product. People will drive for miles for the food. And don’t you dare criticize any of these popular restaurants in front of their fans.

But there’s also a financial reason why these firms grow so quickly: cash flow.

By bringing in more customers and generating higher profits per store, these stores often break even faster than competitors. Theoretically, that means popular chains can double their footprint every couple of years by simply channeling their internal cash flow to build new stores, which generates more cash flow. Two stores turn into four… which turn into eight… 16… and so on.

Dutch Bros also has a phenomenal business model because it is even more capital-light than rivals. As a drive-through coffeeshop, the firm has no hot kitchen, no public bathrooms, and no inside seating area. According to third-party estimates, startup costs per location can be as low as $150,000 – less than half of the cheapest strip mall Burger Kings.

Meanwhile, each location is a profit-spinning machine. In the third quarter of 2025, total revenue increased 25.2% and the company-operated shops’ gross profit was $82.4 million, an 18.4% jump from the year before. The company does not publish cash-on-cash returns, but back-of-envelope calculations suggest that new locations are breaking even in under three years.

The result is a multi-bagger opportunity hiding in plain sight. Dutch Bros plans to increase its store footprint with a combination of existing cash flows and cash-from a $150 million debt issuance in the first quarter of 2025.

Similar internally driven growth rates could arise going forward, which means Dutch Bros will grow exponentially until it finally saturates its relevant markets, perhaps sometime in the 2030s.

Top 2026 Stock No. 7: Devon Energy

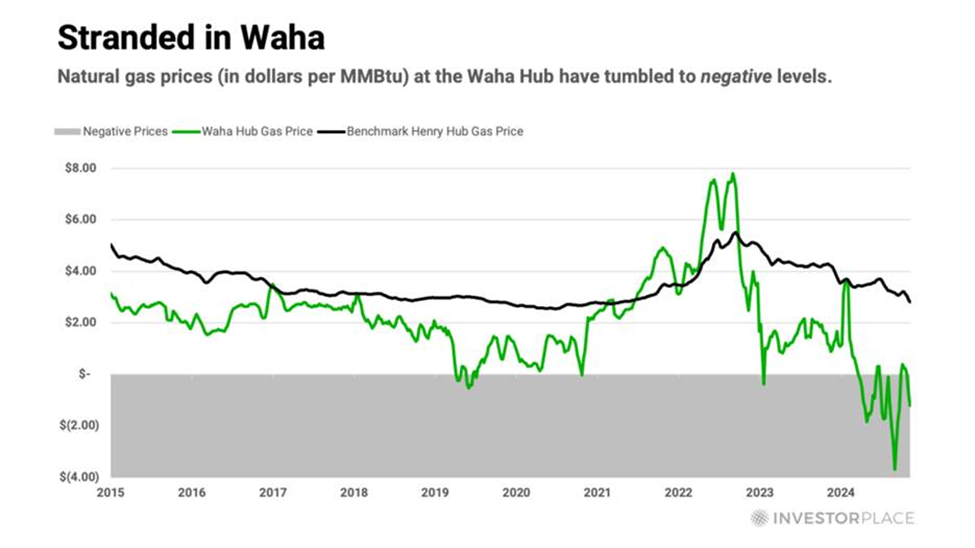

Not all natural gas is created equal. Its location greatly affects its value.

For example, the Delaware Basin’s natural gas, much like a long-distance sweetheart, is geographically undesirable.

Today, natural gas prices in the Delaware Basin, in far west Texas and southeast New Mexico, are depressed for one obvious reason: Gas has nowhere to go. The pipelines that run from the upper Permian Basin to hubs near the Gulf of Mexico do not have enough “offtake capacity” to transport all the gas the region produces.

In the parlance of the oil & gas industry, this excess production is called “stranded gas,” and it is so worthless that producers must find ways to dispose of it. The producers who have permits to burn off the gas simply “flare” it at drilling sites. Otherwise, they must pay companies to truck it away, like dumpsters full of old mattresses.

But the economics of producing natural gas in the Delaware Basin may be on the verge of a major transformation – one that will flip today’s negative gas pricing into solidly positive pricing.

A company called Devon Energy Corp. (DVN) is ideally positioned to benefit from that prospective transformation. It is the fourth-largest natural gas producer in the Delaware Basin, and it has been investing heavily in natural gas transport and processing facilities.

One of those facilities is the 580-mile Matterhorn Express Pipeline, which opened for business in 2024. This new pipeline, in which Devon holds a 12.5% stake, transports up to 2.5 billion cubic feet per day of natural gas from the Waha Hub to the Katy area near Houston.

Following close on the heels of the Matterhorn, Devon’s new 365-mile Blackcomb Pipeline will enter operation in 2026. It will transport gas from West Texas to the Agua Dulce Hub in South Texas, near Corpus Christi.

Importantly, Devon has contracted for significant offtake capacity on both pipelines, which is why the company is planning to ramp up its natural gas production from the Delaware Basin over the next few years.

Devon might also benefit from a new “wildcard” source of natural gas demand: data centers.

As the big tech companies build ever-larger and ever-more-numerous data centers, they are struggling to secure the dedicated power supplies these centers require.

For example, Dominion Energy Inc. (D), the utility that serves Northern Virginia’s “data center alley,” announced in October 2024 that it “expects the time it takes to connect large data centers to the electric grid to increase by one to three years, amid a surge of requests, bringing the total wait time to as long as seven years.”

Because of power bottlenecks like these – both current and prospective – the big tech companies are turning to every and any possible power source to satisfy their needs.

But over the near term, natural gas will take the lead in supplying the additional power. According to Goldman Sachs, natural gas will satisfy 60% of the power demand growth from AI and data centers, while renewables will provide the remaining 40%.

As a result of this growth, data centers could boost the demand for natural gas to fuel U.S. power plants by 20% to 45% over the next four years, according to Wells Fargo research. The midpoint of that estimate would be equivalent to doubling the current production from the Delaware Basin.

The natural gas market offers three major advantages over competing technologies…

- It is abundant.

- It is cheap, especially in the Delaware Basin.

- It is a proven technology with relatively rapid permitting processes.

Data center demand for natural gas could become especially acute in the Delaware Basin, with a new “Data Center Alley” potentially blossoming in that region.

To be clear, data centers will not immediately impact the economics of natural gas production in the Delaware Basin. However, this wildcard source of demand, combined with the two new pipelines coming onstream, could produce significantly higher and sustainable natural gas pricing throughout West Texas.

This likelihood is not lost on the heavy hitters of the U.S. oil & gas industry. They have been falling all over each other to acquire drilling acreage in and around the Delaware Basin. Because this region, which extends from West Texas into southeastern New Mexico, is less developed than the eastern Permian, it contains vast, untapped reserves.

Devon Energy was ahead of the game. Way back in January 2021, Devon kicked off this land-grab in the Delaware Basin by launching a $5.75 billion takeover of WPX Energy. After completing the deal, Devon possessed a massive 400,000-acre land position in the Delaware, along with significant production.

Five years later, Devon is attempting to cash in. The company is devoting about 60% of its capital investment budget to drilling projects in the Delaware.

Devon Energy’s share price does not reflect any upside potential from these new activities… nor much upside potential from any of its other activities.

But as Delaware gas prices trend higher, in the context of stable-to-rising energy prices, Devon’s share price could soar from current levels.

Moving Forward

I’m so glad that you decided to further your journey to wealth by joining Smart Money.

While these seven stocks are sure to fortify your portfolio in 2026 and beyond, those aren’t the only benefits of this free e-letter…

Nearly every Monday, Wednesday, Thursday, Saturday, and Sunday, you’ll receive an email from me wherein I’ll share insights on the latest market megatrends, how to hedge against inflation, which stocks you should avoid, and more.

Get started by visiting your Smart Money website here.

Regards,

Eric Fry

Editor, Smart Money