The market hasn’t been cooperative for financial stocks lately.

A flattening yield curve, distressed high-yield debt and the possibility of the U.K. leaving the European Union (“Brexit”) have traders on edge. Add slowing growth and the threat of more defaults in China to the picture and 2016 look pretty grim for banks and other financials.

Already, we’ve exploited this weakness for several bearish profits in our SlingShot Trader alerts.

However, a lot of that bad news has likely already been priced in. So, should traders still be concerned or is there enough of a buffer to absorb more bad news without larger losses?

In many cases, the answer to that question is probably “yes”; however, there are still a few landmines within the sector that look ready to explode. Investors should avoid them, but traders should be ready to exploit them as a short opportunity.

Read on for the details, namely, the five stocks we most expect to fall into the bears’ crosshairs.

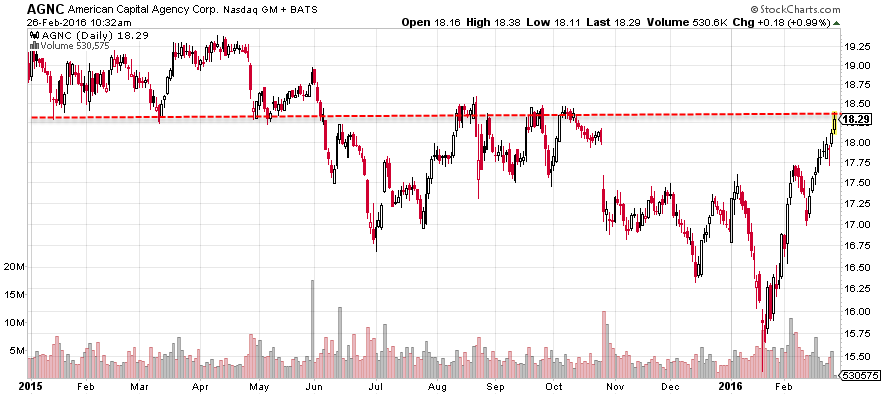

Crumbling Financials: American Capital Agency Corp. (AGNC)

Remember those infamous mortgage-backed securities and their comorbid credit default swaps that helped cause the financial crisis of 2008? Yeah, they still exist.

There’s an argument that the prevalence of “toxic” versions of these instruments are rarer, which is probably true but difficult to prove.

Part of the reason demand for these instruments was never really reduced after the crisis is the prevalence of cheap credit from the Federal Reserve’s quantitative easing campaigns. An incestuous group of public business development companies, REITs and management firms that specialize in leveraging and managing assets in this category has grown significantly over the last few years.

The underlying value proposition for these assets is that a company can borrow cheap capital, buy higher-yielding mortgage assets and keep the spread. Sounds good — but that leverage gets extreme and mortgages are subject to unexpected risks. Without getting into all the complicated details, companies using leverage to invest in mortgages tend to take a hit from interest-rate volatility, mortgage prepayments and flattening yield curves.

All of those issues are a problem now, and we expect they will remain an issue in the near term. Attempts to lower interest rates in Europe, Japan and China while the Fed flip-flops on whether it will continue raising rates in 2016 is a recipe for disaster in the mortgage market because it creates interest rate volatility and uncertainty. We think the decline in mortgage REITs is far from over, and the recent spike in buying has been overblown on falling volume/participation.

While just about any company in this sector looks bad, we think American Capital Agency Corp. (AGNC) shows signs of being the most overbought on unrealistic expectations. We think the stock is likely to experience a “dead cat bounce” off its 2015 highs. The above chart has been dividend adjusted to show you how close the price is to this key resistance level as risks rise in 2016.

Crumbling Financials: MidSouth Bancorp, Inc. (MSL)

The high-yield bond market was shaken up recently as some funds stopped honoring redemptions and default rates have doubled.

Instability in the debt issued by small oil companies has caused the worst of the damage. The size of this loan category isn’t on the same scale as the mortgage market of 2007–2008, however, it is still serious and has been affecting the values of banks holding this debt.

Some of the bigger firms, like JPMorgan Chase (JPM) and Goldman Sachs (GS), have already increased reserves against these loans, but they still represent a relatively small portion of their balance sheets.

Bank of America (BAC) only has 3% of its loan portfolio exposed to oil-related companies. The same cannot be said for a few regional banks, who loaded up on these loans while prices were good and yields were high.

MidSouth Bancorp, Inc. (MSL) is a good example of the problems created by a concentrated portfolio of loans in the oil sector. Approximately 20% of its loans have exposure to the oil market, and its geographic concentration in Louisiana and Texas means it has much greater indirect exposure to the oil market. With oil prices this low, Deloitte has estimated that 35% of all public oil companies could face bankruptcy in 2016.

These issues aren’t a secret, so MSL has already lost more than 50% of its value over the last year. However, we believe that what is happening now is just a precursor to further losses. Small banks like MSL have been consolidating recently as the major indices have stabilized, but this isn’t because the fundamentals have shifted.

Instead, we estimate that banks like this could lose much more value as international crude producers seize the opportunity to force high-cost producers out of the market.

Crumbling Financials: E*TRADE Financial Corp (ETFC)

One of the important contributions to a broker’s bottom line is the difference between what they earn on client deposits and what they have to pay to their clients. This yield spread is very similar to how banks earn some of their profits as well.

Over the last several years, trading costs have been coming down while the yield spread has failed to recover. Many brokers have partially offset these issues by offering new services, focusing on derivatives traders and accumulating larger deposits.

Anticipating that the Fed taper and subsequent rate hikes would finally unlock the value trapped within the narrow yield spread, investors have increased the premium in broker share prices.

The assumption that the Fed would hike rates four times in 2016, however, has shifted to the point that investors now expect a very low probability for any hikes this year.

In mid-February, brokers took off again as positive economic data shifted expectations to be a bit more optimistic. We believe this optimism is misplaced, and the Fed will have their hands tied by slowing global growth and aggressive currency devaluations in Japan, China and Europe.

We think brokers with unusually high value-multiples and weaker balance sheets are the most at risk. For example, E*TRADE Financial Corp (ETFC) could be hit hard if the shares can’t break long-term resistance near $25.

Heading back to long-term support near $20 seems likely to us.

Crumbling Financials: Assured Guaranty Ltd. (AGO)

The bankruptcy crisis in Puerto Rico last year is probably not over. Like Greece, the numbers we have from Puerto Rico’s government are very unlikely to be accurate, and it is almost a guarantee that the crisis will have a few echos in the near term.

There are a few companies on the hook for bond insurance in this crisis. While it may not be as bad for them as it was for American International Group (AIG) during the 2008 collapse, it is still a tough sector.

The stress of the Puerto Rico situation has abated somewhat, and the relatively stronger bond companies with exposure to the municipal bond market have stabilized. While we are likely to see more issues in the municipal market in the near future, the real problem is growth.

As the lending market tightens and existing high-risk loans (see our earlier comments about high-yield bonds) are discounted, bond insurance companies like Assured Guaranty Ltd. (AGO) won’t see a lot of growth in return for riskier industry fundamentals. As with a few of our previous examples, it’s not an issue of potential insolvency as much as it is an issue of growth.

Like you would expect, high-risk, low-growth industries tend to perform poorly in choppy markets. As long as repeating crises like Detroit and Puerto Rico lurk on the horizon, bond insurance companies are going to be stuck. AGO doesn’t have as much exposure to structured products like credit default swaps/obligations, but it has enough to keep investors wary.

We were interested to see AGO’s reaction after the company released earnings on Feb. 25. AGO beat profit expectations but lost the momentum within a few hours as the June 2015 gap created resistance. We expect companies like AGO to continue struggling for future gains as industry fundamentals deteriorate.

Crumbling Financials: State Street Corp (STT)

Not to get too political, but sometimes government regulation is good and helps create a transparent market with fewer systemic risks. We would imagine that most investors will agree. However, sometimes regulation can be bad and winds up hurting investors with unintended consequences.

We will let our readers decide whether the Department of Labor’s new proposed rules that retirement advisors will need to abide by a stricter set of fiduciary standards is good or bad for investors. As you might imagine, Democrats like Elizabeth Warren love the new rules, while Republicans hate it.

Without getting into the Byzantine complexity for how rules like this one will be interpreted (or enforced), it does seem likely to do one thing if it is implemented: make it more difficult for individual investors to add exchange-traded funds to a retirement portfolio. It isn’t that an individual investor won’t be able to buy an ETF; it’s that the incentives to their advisors may change so that they may be less likely to endorse these funds to their clients.

This rule change has not been put into effect yet, and counter proposals by Republicans may be a bit less onerous for financial professionals if they are adopted. However, regulation creates uncertainty, and companies like State Street Corp (STT), Prudential Financial Inc (PRU) and Fidelity are likely to take a hit. With that in mind, we expect fund companies like STT to break lower again in 2016.

“Red flags” like these are easy to spot with just a glance at the charts (and the headlines). But for many traders, it’s not so clear what to do about it.

So, here at SlingShot Trader, we’re giving you an opportunity to join us in “trading the news” for just $39/month with one month free — plus you’ll also get our special report, Blueprint for Options Success! (But hurry: this Flash Sale only lasts 48 hours!)

InvestorPlace advisors John Jagerson and S. Wade Hansen, both Chartered Market Technician (CMT) designees, are co-founders of LearningMarkets.com, as well as the co-editors of SlingShot Trader, a trading service designed to help you make options profits by trading the news. Get in on the next trade and get 1 free month today by clicking here.

Follow John Jagerson and Wade Hansen at Google+!