Although it was once exclusively in the realm of science fiction, the concept of a cashless society is steadily becoming reality. Recently, CNBC ran a segment featuring a technology journalist’s personal experimentation with an implanted payment chip.

The month-long experiment essentially turned the reporter into a human digital payments processor.

The month-long experiment essentially turned the reporter into a human digital payments processor.

While the technology was functionally limited to retailers with the appropriate infrastructure, the underlying message was crystal clear. People want convenience, and that more than likely means a bright future for the digital payments industry.

For investors, that future is a lot closer to us today than it ever has been. On Tuesday, shares of companies specializing in digital payments and services — Paypal Holdings Inc (PYPL), Square Inc (SQ) and Moneygram International Inc (MGI) — had one of their best single-day performances for the current month. SQ stock in particular had a great run, gaining 7% on high volume.

The markets have been less-than-favorable for digital payments on a broader scale, but there is a lot of compelling evidence that this is nothing more than growing pains.

Digital Payments Are the Future

First off, digital payments are finding increasing acceptability among both consumers and businesses. This is evidenced by nearly a quarter of a million U.S. retailers that accept the digital payments system of Apple Inc. (AAPL).

In addition, the digital currency bitcoin — which was once an obscure and legally controversial phenomenon — is being accepted by honest-to-goodness mainstream businesses. On the commerce side, industry giants like Microsoft Corporation (MSFT) and SAP SE (ADR) (SAP) are realizing the importance of interconnectivity and cloud computing. By default, that’s bullish for digital payments.

Second, cybersecurity is big business, in large part due to the ever-present threat of identity theft. Unfairly or not, traditional payment platforms like credit and debit cards have received plenty of negative publicity regarding security breaches.

Here, the digital payments industry has a critical advantage. Unlike credit cards, companies like PYPL offer consumers a central location where sensitive information is stored. Thus, PYPL acts as a trusted intermediary between buyer and seller. No personal information other than contact and shipping data is shared, helping to ensure security.

Credit card companies may fire back and state that online transactions facilitated by their products have the best legal protection. That’s true but such insurance is not cheap.

Also, the physical medium of payment cards can be its own vulnerability. For example, an international gang made off with $19 million from a coordinated heist in Japan using counterfeited debit cards at automatic teller machines. While the victimized institution, South Africa’s

Standard Bank, will book the costs, the ramifications of the incident will be far-reaching.

Finally, traditional banking will likely undergo a paradigm shift brought along by demographic trends. Currently, around 11% of American households don’t have a checking account. That’s typically attributed to a combination of low income and lack of financial education.

However, a poll conducted two years ago revealed that 39% of millennials would consider using alternative financial services like digital payments. That’s a significant departure from older demographics, and points towards growing mainstream acceptance of financial technologies.

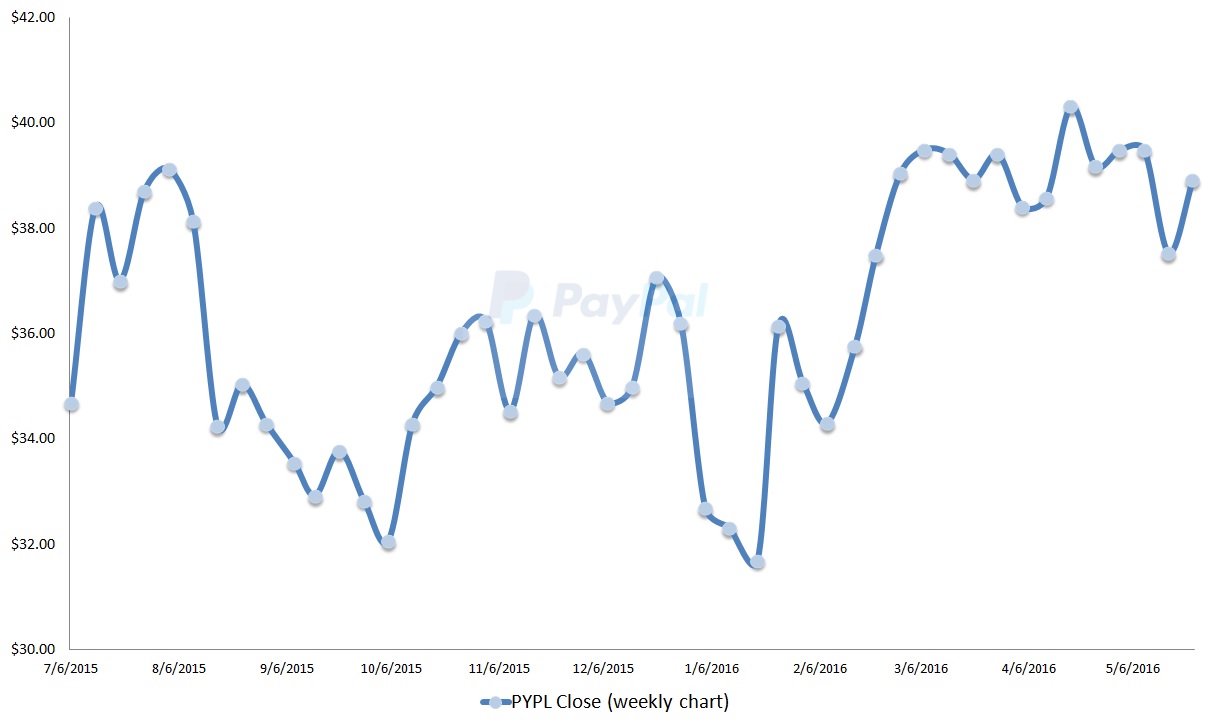

Of companies in the digital payments sector, PYPL should turn out to be the biggest beneficiary.

Click to Enlarge

It has considerable brand-name recognition due to its lengthy time as subsidiary to eBay Inc (EBAY). Also, in its first quarter of fiscal year 2016 earnings report, PYPL showed significant growth in both the top- and bottom-line.

Yes, PYPL stock is admittedly choppy, but let’s face facts here — you’re not going to see this kind of financial expansion in mature markets like credit cards.

What’s particularly impressive is that PYPL has been able to accomplish its earnings beat in the face of greater competition. Even better, it’s a balanced improvement across key metrics — total digital payments volume, new accounts applications, and mobile transactions are all trending strongly. A rising tide is lifting all boats, and that’s a net positive for everyone — including rival competitor SQ.

Running two companies can’t be easy for SQ head Jack Dorsey, especially if the other company is Twitter Inc (TWTR). Nevertheless, I think investors should look at the bigger picture for SQ stock.

Click to Enlarge

Sure, company shares are down 23% year-to-date, and the financials aren’t the prettiest thing on Wall Street. But we shouldn’t discount the fact that, very much like PYPL, SQ is a growth company.

Again, where else are you going to find annual sales growth of 49% and quarter-over-quarter growth of 51%?

But the biggest argument for SQ stock is the underlying industry’s tailwind. Banking is changing. Business is changing. And thanks to demographics, the culture is changing.

Like bitcoin, what seems like an oddity is becoming the normal way of doing things. Paypal’s earnings release brings home the point that the smart phone is transitioning to the “smart wallet.” Considering the convenience and ease of use of SQ products, that’s a huge advantage.

In addition, the fact that SQ and PYPL can simultaneously achieve high growth rates means that there’s more than enough room in the digital payments sphere.

That’s music to the ears of MGI investors, where shares have mostly traded sideways for the year.

Click to Enlarge

Adding to woes are the troubled financials. For its Q1 earnings report, MGI produced middling results. Earnings per share came in at -7 cents, while revenue moved up slightly more than 1% against consensus forecast. Over the last three years, MGI stock has lost 68% of its market value.

However, MGI has an opportunity to turn things around. Aside from their money transfer business, MGI provides digital payments and other financial services for both “unbanked” and “underbanked” communities. In fact, the latter category represents an eye-popping segment of the U.S. population — one-third, or roughly 108 million people.

That surprising statistic is nothing compared to the global percentage of people who either do not use or have access to traditional financial institutions. According to some studies, 50% are unbanked. Research conducted by the World Bank pegs the number at 2.5 billion.

Of course, a vast majority of the figures come from poverty-level communities. But with the general increase in emerging market development, it’s very conceivable that MGI could service regions that big banks can’t reach.

In fact, that’s exactly what MGI is doing. Through a partnership announced earlier this month, MGI will provide mobile digital payments services to consumers in El Salvador. According to data from the World Bank, “mobile wallets have helped the country to nearly triple the percentage of adults with financial accounts in the last five years.”

Not only does this promote financial inclusion — and more business for MGI — mobile services are becoming the norm in developed nations. Simply put, “brick-and-mortar” banking is out, and digital payments are in.

As with any new industry, there will always be unforeseen issues and challenges. But the existence of such shouldn’t be the principal arbiter of an investment decision.

Although companies specializing in digital payments have suffered through enormous volatility, the tide is turning in their favor. More importantly, it’s a global phenomenon that has seen greater market penetration and consumer acceptance.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.