Staples, Inc. (NASDAQ:SPLS) is a hard nut to crack. During its heyday — essentially, the entire 1990s decade — you couldn’t find a better investment than SPLS stock. From start to finish, the office supply retailer generated 1,800% in profits. On average, nineties investors could expect nearly 48% in average annual returns.

Fast forward about 12 years, and it became brutally obvious that Staples stock was no longer a Wall Street darling. Even worse, SPLS didn’t look like it would ever regain its throne. With the emergence of e-commerce sites like Amazon.com, Inc. (NASDAQ:AMZN), the entire retail landscape was undergoing a paradigm shift.

More significantly, the PC market also changed dramatically. Increasingly, digitalization meant that computer software could be purchased and activated online. The justification for physically driving to an SPLS store was nullified, killing off an important revenue source. Thus, Staples stock began to fall apart.

An often overlooked fact is that the broader office supplies business is doing very well. The producer price index for supply manufacturers has jumped 4% in the past two years. The issue is on the distribution side. There’s just not enough room for everyone, causing recurring headaches for SPLS stock.

Big-box retailers like Best Buy Co Inc (NYSE:BBY) or Wal-Mart Stores Inc (NYSE:WMT) will sell office supplies, and everything else. Limiting yourself to just a specific sector is an impossible business. That’s why the Office Depot Inc (NASDAQ:ODP)

merger proposal made sense.

Unfortunately, that’s a no-go, and the focus for the upcoming Staples earnings report on Tuesday is what it can do minus the ODP speculative tailwind. Can SPLS stock pull off a positive surprise?

Mixed Atmosphere for the Staples Earnings Report

For its Q1 fiscal 2018 report, analysts forecast an earnings per share target of 17 cents. Not much variance exists for Staples stock. At the low end, the estimate is set at 16 cents, while the high is at 18 cents. Against the year-ago level, the consensus increased by one penny.

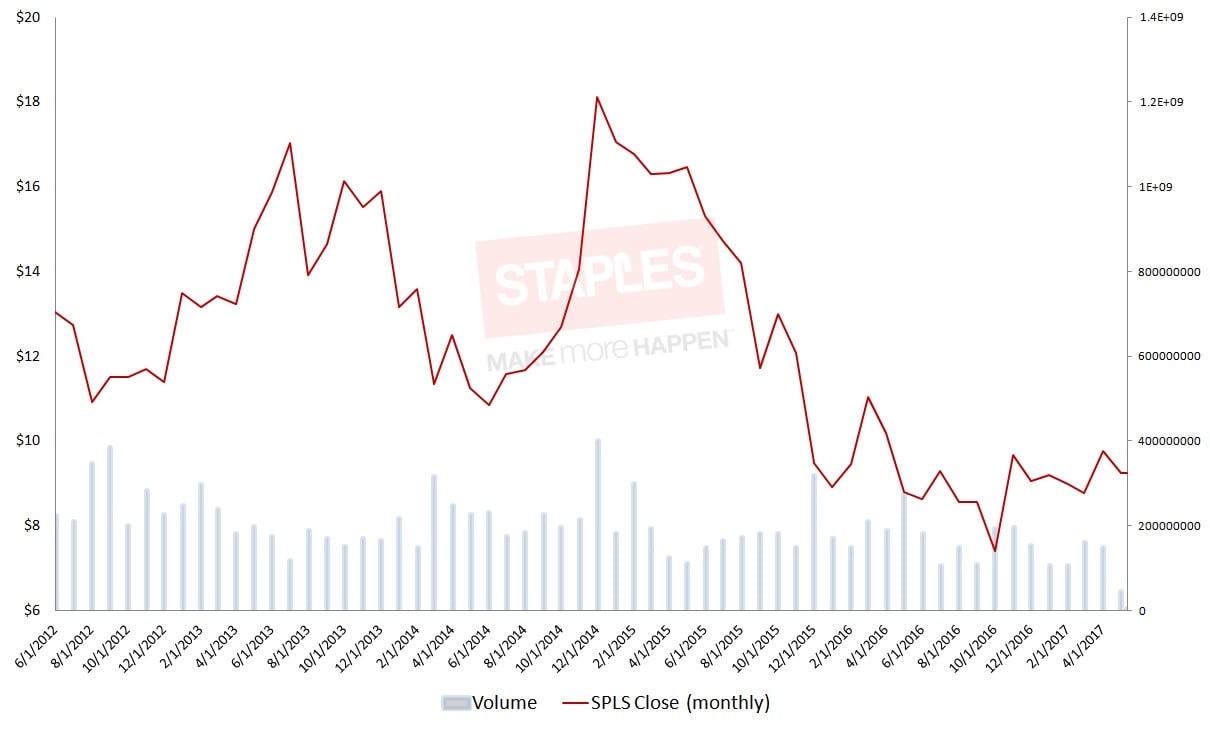

Recent Staples earnings reports were mixed. In their fiscal 2017, SPLS stock had bagged one beat, two draws, and one miss. Overall, the markets responded erratically in 2016. SPLS shares had a peak-to-trough differential of 54%. It was a trade only suitable for speculators, given its feast-or-famine nature. For the year, the retailer ended up with a 5% loss.

Of course, management will be looking to make a case for itself in light of the ODP merger rejection. Cost discipline is the company’s most impressive effort. According to Zacks Investment Research, SPLS “is employing a more efficient customer coverage model, focusing on lowering indirect procurement costs, enhancing supply chain and increasing mix of Staples’ brand products.” Furthermore, the company has cut a number of underperforming stores.

Whether or not Staples stock can advantage its cost savings will come down to sales growth. For Q1, analysts are forecasting between $4.4 billion and $5 billion, with consensus pegged at $4.5 billion. Unfortunately, revenue is where previous Staples earnings reports fell short. In Q4, the company badly missed consensus, while the full year 2017 also fell considerably short.

Although the improvements should be commended, investors gambling on an earnings beat may want to reconsider. According to Zacks, “stiff competition, soft international sales and sluggish demand for paper-based office products due to technological advancements remain major woes for Staples.” I think the deck is stacked too deeply against SPLS stock.

SPLS Stock Is Too Wild to Recommend

Click to Enlarge

For starters, the company shares are like a pinball machine. It could swing north or south based on news, rumors, or rumors of news. In that regard, the Staples earnings report may not mean much.

More critical is disconcerting industry developments. The U.S. Bureau of Labor Statistics reported a 7% PPI loss for office supply retailers over the past two months. That’s exactly the type of news that Staples stock does not need at all.

This recovery is an intriguing storyline. It’s about perseverance and the ability to adapt to changing conditions. Sadly, I’m not too sure if a Hollywood ending will occur for the SPLS stock faithful. To their credit, the improvements are remarkable. However, the retail industry may have changed too much to matter.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.