It looks like athletic apparel stocks are starting to come back in fashion. Perhaps it’s the big selloff most of them have seen. Maybe it’s the fact that we’re coming into the second half of the year, where they can benefit from an increase in business. So is Under Armour Inc (NYSE:UA, NYSE:UAA) about to breakout or breakdown? Let’s look at UAA stock.

Under Armour bulls will argue that shares are a bargain now that they’ve fallen 50% since the start of 2016. The decline is even more devastating if taken from its former all-time highs in 2015.

After such a massive decline, UAA stock is worth a shot on the long side.

The Long and Short Cases for UAA Stock

The Long Case

A distribution deal with Kohl’s Corporation (NYSE:KSS) will act as a catalyst for stronger sales growth. Additionally, Under Armour’s trailing price-to-earnings ratio has been cut in half over the past 12 months, further making the stock attractive.

Short interest is also on the rise. It has more than doubled since January 2015 and it is up roughly 30% since the start of this year. Bullish investors will argue that when a good quarter comes around, short-covering will drive shares even higher.

The Short Case

Just because the price-to-earnings ratio was cut in half, doesn’t make it attractive. On a trailing basis, UAA stock still trades at 52 times earnings. On a forward basis, UAA stock still trades at more than 40 times earnings. Perhaps that would be acceptable if Under Armour were still growing sales at a clip north of 20% annually. But that isn’t the case, with analysts expecting revenue growth of 10.7% in 2017 and 13.3% in 2018.

If it were highly profitable, that would be one thing. But for years bulls said that sacrificing profits in an effort to invest in the company and grow the top line was the name of the game. Take market share and worry about profits later. That’s all fine when the top line is growing robustly. But at 40x forward earnings with little profit and mediocre sales growth, UAA stock seems like anything but a bargain.

Bears will also argue that partnering with Kohl’s may provide a spark, but aligning one’s self with a dying industry isn’t the wisest of moves. Unlike Nike Inc (NYSE:NKE), which

recently announced a trial run with Amazon.com, Inc. (NASDAQ:AMZN).

When it comes to the short interest, a short-squeeze could drive UAA stock higher. However, bears may also argue that despite the stock’s big decline, short interest has continually grown because there’s another shoe left to drop. If Under Armour fails to best expectations, more lows could be on the way.

Trading UAA Stock

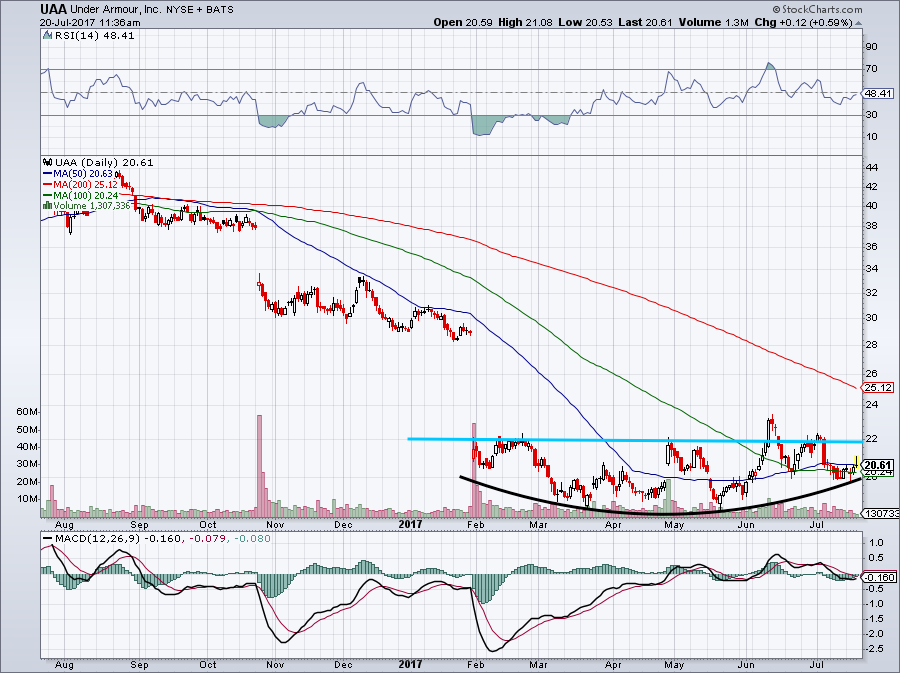

The charts are actually shaping up somewhat bullishly. The constant failures at resistance near $22 are discouraging, but the fact that UAA stock keeps testing it is good. There’s some clear support near $20, where Under Armour stock has found buyers over the past few months. It has also been basing really nicely over the past five to six months.

Could it fill the gap back toward $28? Of course, but the business needs to start doing a lot better. Simply meeting expectations may not cut it, given the stock’s still-lofty valuation. The biggest concern would be a retest and breakdown of the lows near $18.50. A decline to the lows would represent a near-10% fall. But a breakdown from there would likely accelerate the selling, causing overwhelming losses.

To be a buy, UAA stock needs to break out over $22 resistance.

Our Thoughts on Under Armour Stock

Click to Enlarge

We’ve already put our money where our mouth is and that’s with Nike. The stock is trading better, recently spiking on earnings at the end of June and even more recently on July 20th thanks to positive analyst coverage.

Morgan Stanley hit the stock with a $68 price target, pushing the stock back to its previous highs.

In fact, another analyst — this one Needham — also believes that Lululemon Athletica Inc. (NASDAQ:LULU) has solid upside. For their part, they have a hold on Nike and Under Armour.

But the point is kind of the same: Nike and even Lululemon look like better buys at the moment. Under Armour’s problem may be its brand. We recognize it’s a quality company with quality products. It won’t go the way of Starter or other discarded sports brands.

However, it’s not Nike. Demand out of Europe, China and quite frankly the rest of the world is still strong. It’s got the best athletes and is a major global icon. Because of that, NKE stock is worth a premium — and even then, it still trades at more than a 50% discount to UAA stock.

Under Armour may turn its woes around. It may even do so sooner than we think. But it might not, and as if that downside weren’t discouraging enough, there’s a better company with a stronger brand and a better value presenting itself.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a long position in NKE.