Twilio (NYSE:TWLO) has been on a tear so far this year, with TWLO stock up a robust 136%. That fact alone will turn a number of investors off, but should they ignore Twilio?

With a market cap of just $5.4 billion, there’s always the possibility that Twilio can go higher. With a limited number of shares or if an interested acquirer comes sniffing around, TWLO stock could have upside. For example, Salesforce.com (NASDAQ:CRM) has an equity stake in the cloud-based tech company.

Twilio is a name I had on my watchlist in 2017 and, for whatever unfortunate reason, it just sort of fell off the radar. That’s too bad too, as shares have gone from sub-$25 in February to more than $55 today. Still, analysts think there’s upside left — plenty of it in fact.

Piper Jaffray and Rosenblatt analysts just recently slapped a $70 price target on TWLO stock, implying more than 27% upside from current levels. While there are a number of price targets between $50 and $65, Argus takes the cake with its $75 price target from Thursday. It implies that TWLO stock can run another 36% — should it do so, it would sport a market cap north of $7.25 billion and give Twilio new all-time highs.

Valuing TWLO Stock

Everyone loves a hot tech stock, but there are a lot of critics when it comes to valuation. We don’t need to look any further than Netflix (NASDAQ:NFLX) or Amazon.com (NASDAQ:AMZN) to know that’s true.

It’s not much different with TWLO stock.

Analysts expect Twilio to lose 9 cents per share this year and earn just 7 cents cents per share next year. But this isn’t an earnings story right now — it’s still very much a growth story. Current revenue estimates call for 36% growth this year and another 23% growth next year.

Further, trailing cash flow from operations (OCF) is in positive territory, while free-cash flow (FCF) is at its highest levels and just below break-even. Should FCF turn positive and both metrics continue higher, it will be an important feather in Twilio’s cap. In my view, cash flows are one of the most important metrics for young Software as a Service and tech companies.

The reasoning is simple. Most investors value stocks on earnings, but because TWLO and many others have no earnings, they can’t be valued that way. Instead, investors value them on sales and in many cases, they all seem expensive. For instance, shares of Twilio trade at roughly 10 times this year’s revenue.

That’s a no-touch in most people’s mind.

But by only looking at sales valuations, we would rule out names like Visa (NYSE:V) and Facebook (NASDAQ:FB) simply because they appear high. However, these names have such attractive margins that the sales-based valuation is simply a misrepresentation of their worth. Admittedly, Twilio does not have the same margin profile as V and FB. But should its cash flows turn positive and trend higher and its margins improve, there’s a case to be made for owning TWLO stock.

Trading TWLO Stock

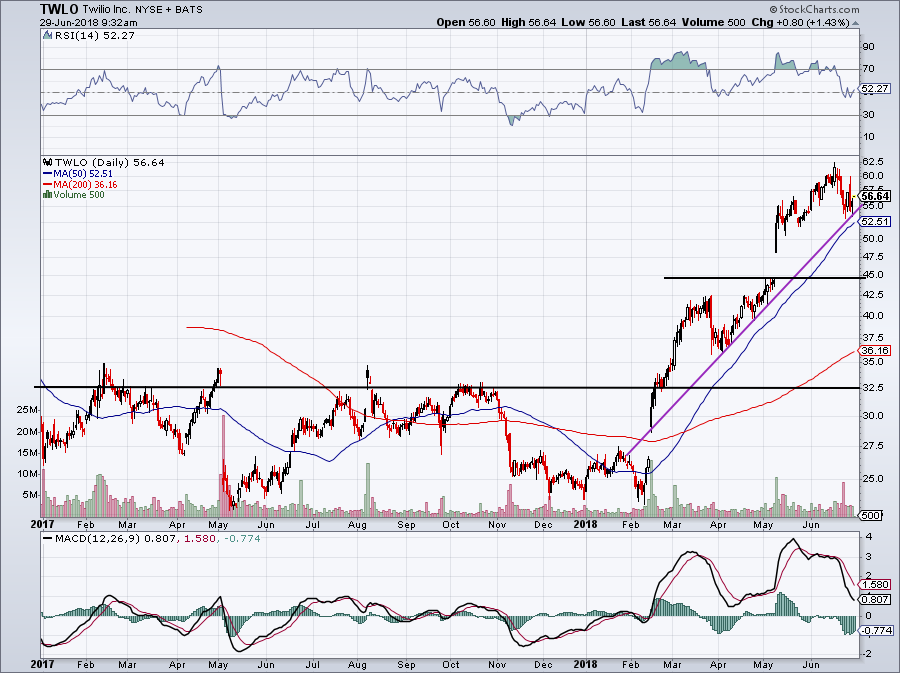

Click to Enlarge

That said, TWLO stock was much more attractive earlier this year when it was down below $30. Between the $32.50 to $35 area, TWLO was ready to run. Our trend-line of support (drawn in purple) highlights the sharp rally it’s been on since February. Now near $56.50, the 50-day moving average currently rests about $4 per share or 7% below current levels at $52.50.

It seems extreme, but I would love a pullback to the $45 area. This would bring TWLO stock back down to the last area it traded near before its giant gap-up in May. While it’s not pictured on the chart above, a look at its long-term chart shows that $45 was also a significant level a few years ago.

This would make for a great risk/reward spot for bullish investors, particularly given Twilio’s admittedly rich valuation at current prices. That said, TWLO stock has to fall below trend-line support first. Shares could surely continue their momentum in the second half of 2018, but a shot to get long on a deeper pullback would be great.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in CRM and V.