There’s no sugar coating it: Cannabis stocks have had a tough ride in the second half of October. Collectively, the group was hammered as the overall markets took a hit. Surprisingly though, many cannabis names held up fairly well — Aurora Cannabis (NYSE:ACB) included.

That’s as recreational marijuana became legal in Canada in mid-October. Several stocks broke out just ahead of the event, only to reverse lower and join the major selling theme of the market. It set up as one great sell-the-news event, something we weren’t surprised about when we looked at Canopy Growth (NYSE:CGC) earlier in the month.

With many cannabis stocks making major moves lower, it no doubt brought some investors back to the table. They want to know, is it time to buy cannabis stocks, and specifically, is ACB stock a good one to buy?

Valuing Aurora Cannabis Stock

The company’s growth is actually pretty solid, with ACB stock racking up $55 million in sales for fiscal 2018, which ended on June 30. That was a tripling from the prior year’s $18 million in sales.

While that’s great from a sales perspective, I worry about cost control in getting to that point. For instance, cost of goods sold (COGS) increased nearly 6-fold, from $2 million to $11.7 million. SG&A expenses swelled from $17 million to $72 million and total operating expenses increased from $27.7 million to $135.3 million.

Because of “other income” on the income statement, it skews net income to the positive side, implying the company earned almost $72 million last year. On the surface, that looks like 46% net profit margins, but that’s not the case by any means. So investors need to be aware of that before they take these surface numbers at face value.

Between 2017 and 2018, total debt went from $63 million to over $200 million while total cash went the opposite direction, from $159 million to $89 million. However, current assets of $219.7 million do trump current liabilities by quite a bit, with the latter standing at $75.1 million.

So where does that leave us? With ACB stock commanding $6.7 billion market cap, it’s not cheap. Coca-Cola (NYSE:KO) has said it’s out as a buyer or partner to the industry right now, but could PepsiCo (NYSE:PEP) be into cannabis? How about other alcohol giants like Boston Beer (NYSE:SAM), Molson Coors (NYSE:TAP

) and others, the way Constellation Brands (NYSE:STZ) took a massive stake in Canopy Growth?

For me, Canopy is the “surest” bet in the business and that’s why if I had to bet on one, it would be with them. But that doesn’t mean others can’t buy or take stakes in ABC, Tilray (NASDAQ:TLRY) and others.

Trading the ACB Stock Price

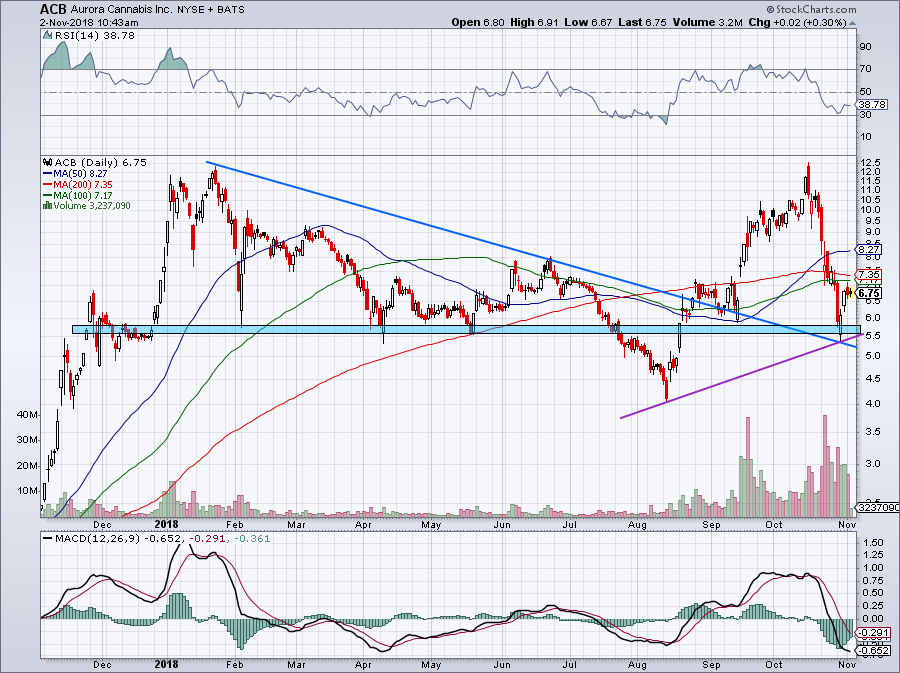

Click to Enlarge

Even before the legalization pop in mid-October and even after the bounce from sub-$6 a few days ago, ACB stock is still down from early October. So where does that leave us?

Since it’s bumping into the underside of the 100-day and 200-day moving average, now may not be the best time to go long Aurora Cannabis if you are bullish. However, I would feel more comfortable stepping into this name in the mid-$5 range.

From there, the risk-reward is much, much better. First, there’s the backside of downtrend resistance (blue line), which has been significant over the past year. There’s also uptrend support (purple line) and a notable level of support between $5.50 and $5.75. Losing all three levels would be a sign that investors need to bail on their long position. Above all three major moving averages and the $10 mark is back in sight.

Thus, there is attractive risk/reward between $5.50 and $6.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.