Target (NYSE:TGT) is the Rodney Dangerfield of the retail world; it gets no respect. Target stock is down 12% since reporting its third-quarter results on Nov. 20, and TGT stock has plunged 22% from its early November high.

Its third-quarter results weren’t bad. Indeed, the retailer’s earnings were up nicely year-over-year, and its same-store sales growth was robust. Neither was robust enough to satisfy investors, however, who chose to see the glass as half-empty.

Give Target stock time, though. Assumptions and pessimism may be weighing on Target stock right now. But this usually-overlooked retailer actually has several more levers it can pull to better compete with its bigger rivals like Amazon.com (NASDAQ:AMZN) and Walmart (NYSE:WMT).

The Turnaround Few See

Many of Target’s current challenges were of its own making.

TGT largely let Amazon become a monster without really challenging it along the way. Now it’s playing catch-up. Its 2013 data breach, though not the biggest ever, was certainly a high-profile embarrassment. In 2016, the retailer elected to make all of its fitting rooms and restrooms non-gender, spurring a relatively effective boycott. And, for years now, TGT has struggled to maintain the kind of “cheap chic” vibe that boosted its results, elevating Target stock and helping make the company what it is today.

Take a closer look at the company’s recent and projected performance, though, and you’ll see that many of its merchandising missteps have been fixed.

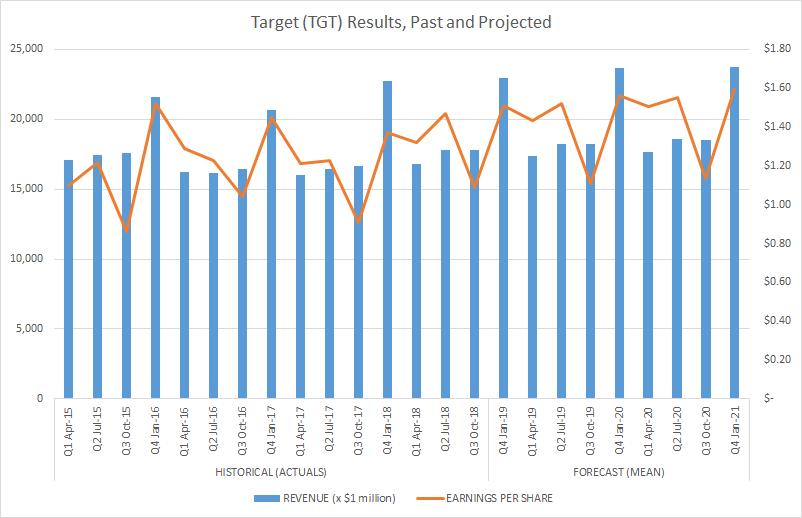

Last quarter’s numbers provide ample evidence of Target’s progress. Though its earnings fell short of expectations, the company’s operating profit of $1.09 per share was remarkably better than the year-ago figure of 90 cents. Target’s same-store sales growth of 5.1%

missed analysts’ consensus estimates of 5.2%, but its Q3 same-store sales growth came in above that of WMT.

Target stock may have simply been a victim of unreasonably high expectations. That, or investors were rattled by the decline of its gross margins from 29.6% in the year-ago quarter to 28.7% last quarter.

The decline was ultimately caused by investments that TGT made in its growth in general and the growth of its digital sales in particular. Those investments had to be made, however, given that its rivals like Walmart and even Costco (NASDAQ:COST) are making similar investments.

Largely lost in the post-earnings melee was the fact that the company’s comparable digital sales surged a hefty 49% last quarter, indicating that its investments are already paying off.

Although online sales are still only a tiny part of Target’s revenue mix, they are growing quickly. Bank of America Merrill Lynch analyst Robert Ohmes wrote late last month “The impressive sales acceleration reported by both Walmart and Target in the most recent quarter implies both company’s expanding omni-channel initiatives are resonating with shoppers,” adding “This growth has outpaced that of other brick and mortar retailers as well as online players like Amazon, and has been supported by the rapid expansion of buy-online, pick-up in store options at both retailers.”

Ohmes believes that Walmart and Target gained market share during this year’s Black Friday/Cyber Monday weekend; that was definitely an impressive feat for TGT, in light of Amazon’s ever-growing dominance and Walmart’s rekindled growth initiatives.

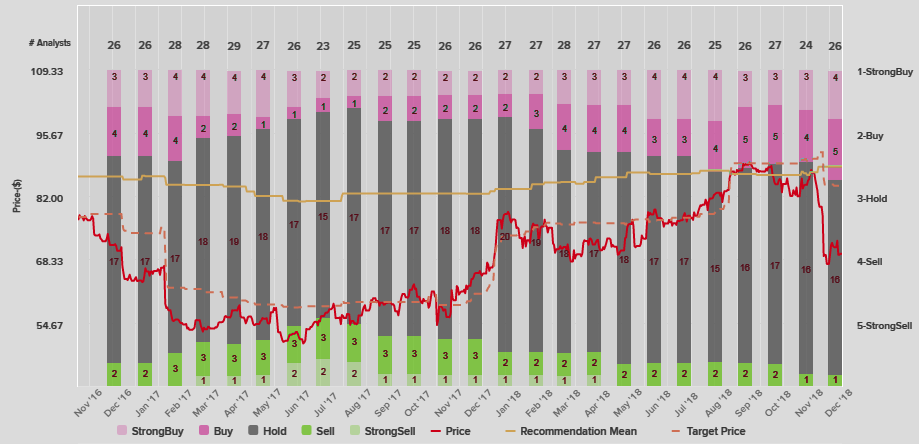

While retail investors have tortured TGT stock since early November, analysts haven’t flinched. The pros collectively expect the company’s recent, impressive growth to last for the foreseeable future.

Click to Enlarge

Though the consensus analyst price target of $84.47 on Target stock is lower than it was a month ago, it’s still 30% above the current price of TGT stock. Analysts could have dialed back their price targets on TGT in a big way, but they refrained from doing so. And in the last month, analysts’ ratings of Target stock have become more bullish

Click to Enlarge

The Bottom Line on Target Stock

While TGT stock’s forward price-earnings ratio of 12.1 is also a good reason to own Target stock, until the majority of the trading crowd is ready to believe in TGT stock, the shares could remain suppressed. Welcome to the game.

Still, Target’s results can’t be overshadowed by doubts about Target stock forever. The company is doing its job, and the short-term pain of thinning margins it’s feeling right now should ease in 2019. After the company announced its third-quarter results, CEO Brian Cornell told analysts: “I will say that we are optimistic about our ability to deliver profitable growth next year and beyond.”

Given how harshly investors have punished companies for even the most modest of shortcomings recently, it’s unlikely that Cornell would allude to a forecast that he’s not confident he can meet.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.