Johnson & Johnson (NYSE: JNJ) was flying high in 2018 on its way toward yearly highs in the fourth quarter. That ascent ended abruptly on allegations that management knew its baby powder could be contaminated with asbestos. Despite thousands of product lawsuits already, the market decided that the liabilities are not priced into JNJ stock.

Now, after falling almost 15% from yearly highs, investors are wondering when the oversold conditions will end.

Before the powder hit the fan, JNJ posted strong third-quarter results. The company beat consensus earnings and revenue estimates with — wait for it — the consumer products unit posting higher operational growth across all of its franchises.

Management credits the relaunch of its iconic Johnson’s Baby brand in the U.S. for the strong quarter. The pharmaceutical sector outperformed peers. Medical devices continued to hold a market-leading position. More specifically, sales of medical devices in hospitals grew almost one full point year-over-year. In sum, JNJ is on pace to deliver growth above the market average by 2020.

JNJ by the Numbers

For the quarter, sales grew 3.6% to $20.3 billion. JNJ earned $1.44 a share, or $3.9 billion, up from $1.37 a year ago. If amortization expenses and special items are excluded, the company earned $5.6 billion, or $2.05 a share. At a 9.5% EPS growth rate, the stock trades at a PEG of around 2x. By comparison, The Procter & Gamble Company (NYSE: PG) has a 3.5x PEG and Pfizer Inc (NYSE: PFE) is at 2.4x.

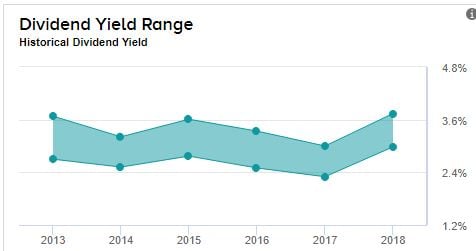

And as the JNJ stock price started falling in November, the dividend yield only went higher.

Source: TipRanks

JNJ Stock Clearly Undervalued

The exceptionally strong quarterly report suggests that the market is reacting too harshly to JNJ’s alleged knowledge on the safety of its baby powder. The company already has an idea on its related liabilities. This is after assuming that the company will settle and strike a deal with the plaintiffs. And since markets are typically exaggerating on the downside risks, they are forgetting on JNJ’s strengths in a slew of other sectors.

On the consumer front, the beauty segment fueled 6.5% growth. JNJ streamlined the business by divesting its Nizoral anti-dandruff product. Neutrogena delivered solid results as its facial moisturizing products resonated with consumers. It gained market share in the sun protection business.

The unit’s solid results were not limited to the U.S. markets. In the Asia Pacific region, Neutrogena had strong uptake. JNJ strengthened the unit’s resilience by acquiring Zarbee’s. The strong demand for allergy reliever Zyrtec, Imodium for digestive health and Tylenol plus Motrin in analgesics will continue in the current quarter and this fiscal year.

Valuation in Focus

The average price target of 11 analysts tracked by TipRanks

is ~$147.00. Morgan Stanley analyst David Lewis now has a hold rating and a $130 price target (as of Jan. 2). Amit Hazan at Citigroup rates JNJ stock the same but with a $139 price target.

Taking the fair value calculation further, if Johnson and Johnson’s revenue falls by a point to 5% and stays there, the stock would still have 14% upside. In a five-year DCF revenue exit model, after assigning a discount rate of between 8% – 9%, JNJ stock has a fair value of $146.60:

| FY Ending Dec. | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Revenue ($, 000) | 76,450 | 81,141 | 85,198 | 89,458 | 93,930 | 98,627 |

| % Growth | 6.30% | 6.10% | 5.00% | 5.00% | 5.00% | 5.00% |

| EBITDA ($, 000) | 24,634 | 29,331 | 31,335 | 33,122 | 35,711 | 38,376 |

| % of Revenue | 32.20% | 36.10% | 36.80% | 37.00% | 38.00% | 38.90% |

Source: finbox.io

Use JNJ as a Hedge Against Tobacco Stocks

Income investors cannot ignore the 33% drop in Altria Group (NYSE: MO), 56% drop in British American Tobacco (NYSE: BTI), or 40% drop in Philip Morris International Inc. (NYSE: PM). Anti-smoking laws and consumer trends could hurt the tobacco sector. That makes JNJ stock a perfect hedge against those shares. Strong performance for its JNJ’s antismoking aids picked up in Q2. Should momentum against smoking pick up in the U.S. and in international markets like Japan, tobacco stocks may continue underperforming. Conversely, JNJ’s anti-smoking unit will thrive even more in 2019.

Bearish sentiment may slow the rebound in JNJ stock but not forever. When markets look for value, JNJ will be on the top of the list.