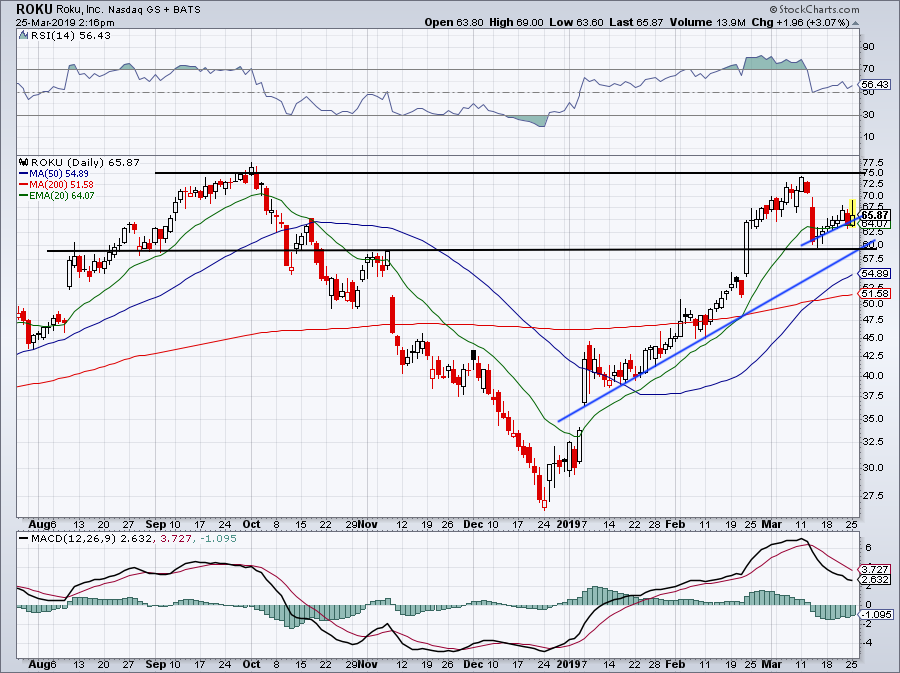

Roku (NASDAQ:ROKU) is showing some signs of fading momentum, but that’s more attributed to its massive rally over the past few months. Despite the recent correction, Roku stock is still up more than 135% from its December lows. While the stock may be losing some momentum, the business most certainly is not.

The company’s most recent earnings report shows as much. After a beat-and-raise quarter in November, Roku stock was hammered. Despite just hitting a 52-week high near $75 a month prior, investors buried this name.

They had no business doing so, and it came down to the fact that high-valuation growth names were under fire. Shares bottomed near $27 on Christmas Eve and went on a rapid rebound.

Despite just about doubling from its December lows into its February earnings report, Roku Inc stock gaped higher and surged after another beat-and-raise quarter. Like the stock price, this momentum can only continue for so long on a short-term quarterly basis.

However, the momentum in streaming is very clear, and it’s why we have names like Disney (NYSE:DIS), AT&T (NYSE:T), Amazon (NASDAQ:AMZN), Netflix (NASDAQ:NFLX) and now even Apple (NASDAQ:AAPL) involved in this theme.

Click to Enlarge

So Why Acquire Roku Stock?

Simply put, Roku stock is spearheading the charge in video streaming. The shorts are very quick to point out that Roku stock carries a $7 billion valuation and will generate just $1 billion in revenue this year. It doesn’t generate robust free cash flow or profits and its streaming device and TVs will become commoditized hardware.

Everyone else — Netflix, Disney, Amazon — has streaming platforms with either their own content, licensed content or a combination of both. Roku’s is different in that it acts as a hub for all of these different platforms. Its simple interface and reasonable price has drawn in a large number of buyers, helping it grow its market share.

In a recent survey among streaming users, almost 70% of them used Roku devices. This easily outpaced the Amazon’s Fire TV at 36.6% and Apple TV at 28.4%. The total does not add up to 100%, because many cord-cutters use multiple devices. For instance, almost 30% of respondents stream through a smart TV as well (another large category for Roku).

Where did Alphabet’s (NASDAQ:GOOGL, NASDAQ:GOOG) Chromecast come in? At just 16%. Of all the major devices, this was easily the worst.

Why Alphabet Should Consider Buying Roku

The first reason is obvious: Google is getting its butt kicked in streaming devices and while this isn’t its bread-and-butter business, gaining a larger threshold in this secular theme would be a win. An acquisition of Roku would instantly make Google the leader in streaming devices, rather than one of the losers.

The second reason? The company can actually afford it. Alphabet has one of the market’s strong balance sheets and last quarter, it only got stronger. As Uber and Lyft IPO, GOOGL — which has a stake in both — will reap even more cash. As of last quarter, GOOGL was holding $109 billion in cash and short-term investments. It has another $13.8 billion in long-term investments. On the liabilities side, GOOGL holds just $3.95 billion in total debt.

The third reason? Roku isn’t a commoditized hardware player like the bears make it seem. In fact, Roku’s renewed focus on advertising and services revenue is exactly why a company like GOOGL should be interested.

The company saw revenue climb 46% year-over-year last quarter. Of that, Platform revenue (services and advertising) surged 77% vs. Player revenue, which climbed just 21%. Platform gross profit jumped 72% to $109 million while Player revenue fell 70% to $2.9 million. Essentially, management knows the company’s opportunity is the platform and not in player sales, but growing market share of the latter adds momentum to the former.

Active accounts rose 40% in the quarter and streaming hours surged 69% to 7.3 billion hours. This is a land grab and it would be wise for someone to capitalize on Roku Inc stock while it’s under $10 billion. With Alphabet’s YouTube and YouTube TV offerings, Roku could make a great addition to its video business.

The Final Case for Roku Stock

Roku has serious momentum in Platform revenue and has a massive lead in player market share. As it grabs more market share, Platform revenue and profit will continue higher.

As if it weren’t positioned perfectly in the streaming video theme — which feels like is hitting a tipping point — Roku’s financials are in order too. Roku Inc stock carries no debt, while total current assets of ~$433 million easily outweigh total current liabilities of $194 million. Finally, the company is free cash flow neutral and so long as momentum continues, should eventually turn free cash flow positive.

As Roku stock rallies, it is getting more expensive. This could take M&A off the table, but you never know.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he was long AAPL, GOOGL, AMZN, and ROKU.