Tesla (NASDAQ:TSLA) is betting on autonomous car service to improve its long-term growth outlook and the bullish sentiment towards TSLA stock. However, the market has not reacted favorably to Elon Musk’s prediction on autonomy and Tesla’s role in it. Tesla stock is down by close to 30% since Musk made bold predictions on robo-taxis and autonomous cars.

I am still bullish on Tesla stock, but there are a number of reasons why robo-taxis and autonomy might not solve Tesla’s margin and cash problem. In this segment, Tesla would be competing against giants like Alphabet’s (NASDAQ:GOOG, NASDAQ:GOOGL) Waymo, Nvidia (NASDAQ:NVDA), Intel (NASDAQ:INTC) and others.

Tesla should note the recent drubbing of Lyft (NASDAQ:LYFT) and Uber (NYSE:UBER) after their IPOs. Wall Street is sending a clear signal that the long-term growth of these platforms is not certain.

Transportation as a Service Is the Problem

In this decade, we have seen a flourishing of companies who are providing alternatives to car ownership. These companies have attracted billions of dollars in investment from venture capitalists and are now taking the IPO route. However, virtually all of them — Lyft, Uber, Grab, Ola, etc — are losing money. Lyft’s stock price history shows the waning attraction of this sector for Wall Street.

Decline in Lyft stock after its IPO.

One of the biggest reasons for the big losses from Uber and Lyft and their peers is how easy their services are to replace. Most commuters do not care about their ride-hailing option as long as they get lower prices. The ability to create customer loyalty is very low in this sector. The only way a ride-hailing company can guarantee good profits from a region is by becoming a monopoly or near monopoly. It is unlikely that the market forces will allow such a monopoly to exist for too long. Also, the governments and regulators in every region would prevent it.

Larger tech firms like Google and Facebook have been able to create a near monopoly in international regions because of the network effect and the high technical barrier to entry. Ride-hailing companies only have the benefit of a big cash balance which they can use to limit the growth of competitors.

If Tesla were to enter this industry through a robo-taxi service, it would inevitably see a similar service from Waymo or Intel within a few quarters. I expect companies will need to absorb huge losses to gain market share. In such a scenario, Tesla will not be able to match the investment of Google, Intel or any other major autonomous competitor.

Where Is the Competitive Edge?

As mentioned above, most commuters do not care about the ride-hailing service as long as they get cheap fares. Tesla might get an edge by branding its service as a fully electric and autonomous option. This will bring it closer to a sustainable transportation service. But other big car majors will also be planning on launching their own electric options.

Musk mentioned that the current cost for such a robo-taxi would be under 18 cents per mile and it will go down in the future. This seems quite attractive compared to the ride-hailing prices offered by Lyft or Uber (around $2 to $3). But again, the most important question would not be pricing but the competitive edge for Tesla.

If Tesla is given regulatory approval to launch such a service, it would be possible for Waymo and Intel to also get approval. Once this is done, it will be a question about a bigger cash balance. In this race, Tesla will obviously lose as the company is already cash strapped.

Tesla Stock Can Still Make a Bullish Run

Tesla’s biggest strength is the overall brand image created by the company and Elon Musk. Getting a first-mover advantage in autonomous ride-hailing segment might look appealing but it will not be able to leverage Tesla’s brand image in the long run.

At the same time, Tesla as a number of advantages which a traditional car manufacturer does not have.

Tesla has sold hundreds of thousands of vehicles in both domestic and international markets without big investment in advertisement. There is a strong brand following for the company. We should see new products and services by Tesla over the next few quarters beside the pipeline of new cars.

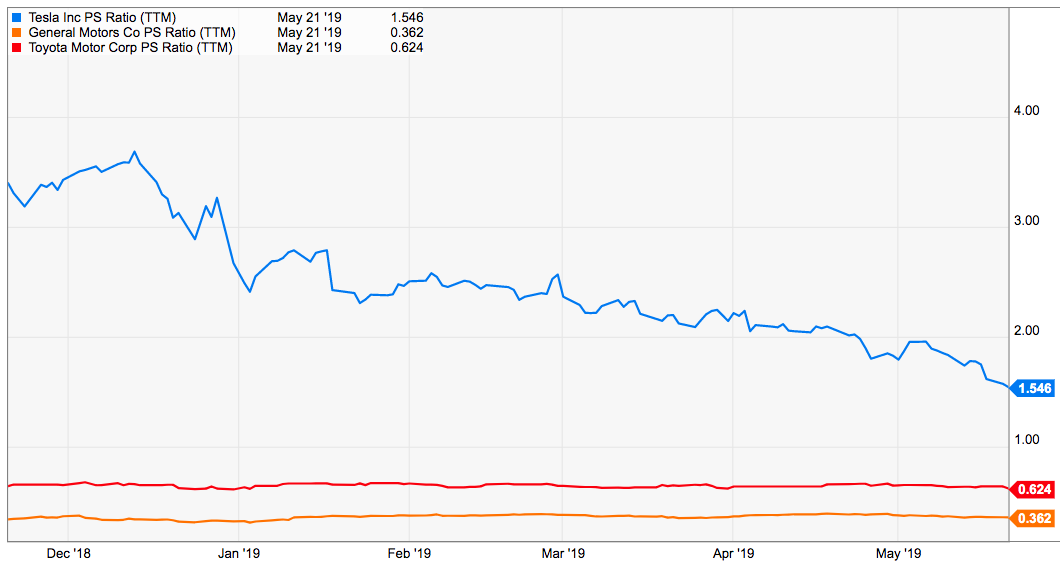

The recent pullback in the stock has brought the price-to-sales ratio of Tesla stock closer to traditional car manufacturers.

Move into Consumer Electronics

Tesla needs to focus on a new segment which can provide the company with healthy margins. Tesla should leverage its brand image to enter consumer electronic segment. Despite market saturation and heavy competition, Apple (NASDAQ:AAPL) is able to deliver big margins in its iPhone and iPad segments. These segments deliver enormous free cash flow and have a good moat against the competition.

Tesla has increased the electronics within its cars to remove many traditional gadgets. Tesla can leverage its brand and product development skills to launch new consumer electronic goods. The ability to outsource production in most of these devices will also reduce the burden on the company. I believe that Tesla’s search for healthy cash flow segments will eventually take it to consumer electronic industry which should be a big boost to Tesla stock.

Investor Takeaway

The past couple months have shown a big decline in the price of Tesla stock. Wall Street has not been impressed by the autonomy play announced by Elon Musk, nor its most recent earnings report. At the same time, the company has a brand image and technical capability which can beat many traditional players. This should give TSLA management enough choices to launch new products and services in the next few quarters. Consumer electronics should be one of the ideal choices for Tesla because this segment has strong brand loyalty and healthy margins.

Investors willing to bet on the brand and management skills of Tesla should find the current price of TSLA stock quite appealing.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.