Shares of JD.com (NASDAQ:JD) have been obliterated over these past few trading sessions. Shares fell over 19% in just eight trading days, before landing at support earlier this month. This comes as trade-war tensions increase.

The Alibaba (NYSE:BABA) trade is crumbling in similar fashion, although shares could have a lot further to fall. The stocks are starting to stabilize, as investors parse through the financial and look for bright spots.

The simple truth is, equities are at the whim of the U.S.-China trade war. When the headlines are positive and investors are optimistic about its progress, stocks ride higher. In particular, Chinese equities are back in favor. When tensions are on the rise though, equities — especially JD, BABA and others Chinese names — are under severe pressure.

Let’s look at the charts of JD stock price.

Trading JD Stock Price

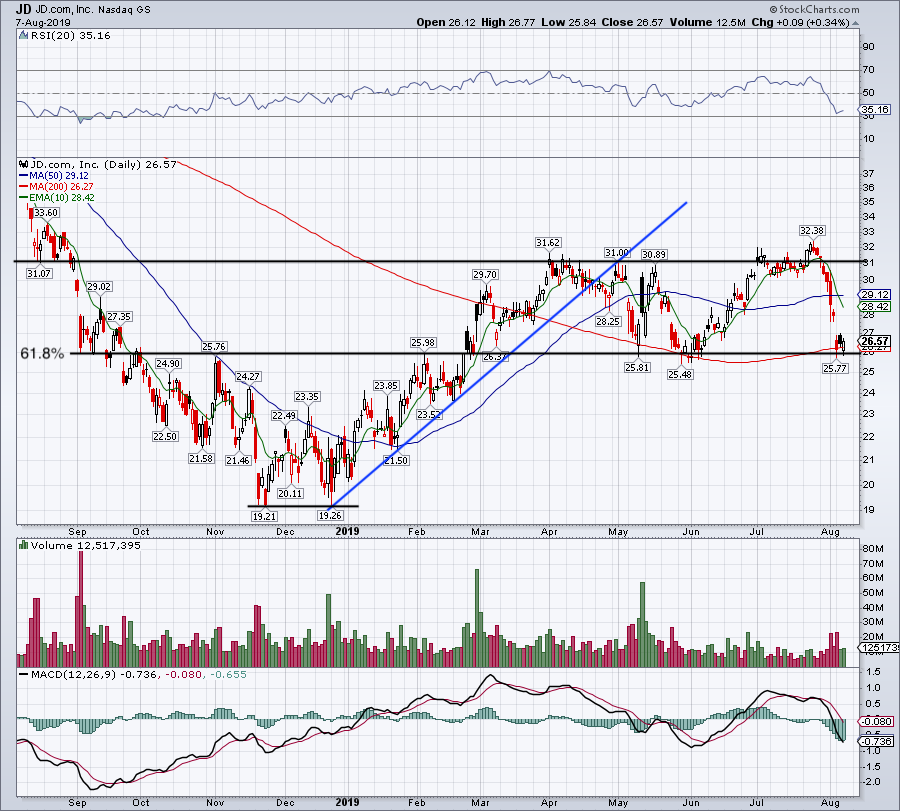

JD stock price is sitting on a very important level right now: $26.

Click to Enlarge

After putting in a double-bottom near $19.25 in November and December, JD stock began a steady uptrend in 2019. While $26 was initially resistance, it eventually gave way. $31 ultimately became range resistance, while pullbacks were met by range support at $26 — which remember, was prior resistance in January. This type of price action is constructive.

Since May, $26 has buoyed JD.com stock three separate times. It helps that the 200-day moving average is also near this area. When JD pulled back in May and June, the 200-day was in decline, but on its current test of the $26 area, the 200-day is trending higher.

However, $26 is more than just range support and the 200-day moving average. The 61.8% retracement for the one-year range rests at $25.93. So investors can clearly see why this area is so important.

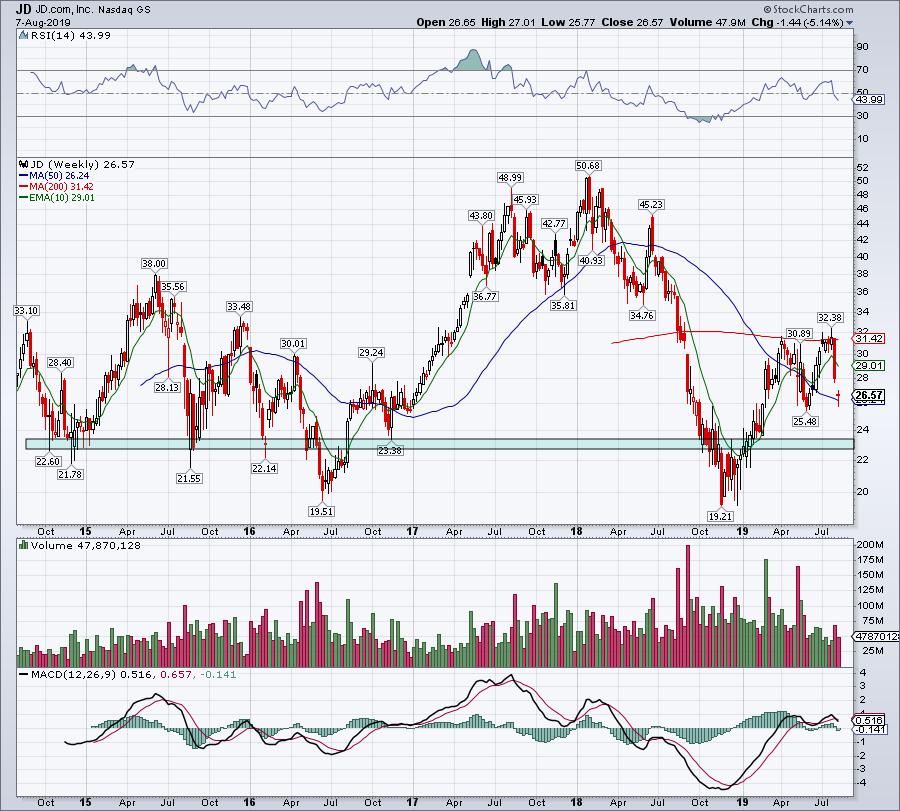

Click to Enlarge

If the trade news deteriorates notably from where we are today, this level may gave way. If it does, perhaps a decline into the $23 area is in the cards, as the long-term weekly chart below suggests.

Also notice on the weekly chart that the 200-week moving average is acting as resistance near $32, while the 50-week is acting as support. Yet another layer of support near the $26 mark.

Valuing JD.com Stock

The problem with JD? It’s not Alibaba. The latter has multiple growth levers it can pull, is quite profitable and has diversified its revenue stream. Other mega-cap tech companies — like Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) Amazon (NASDAQ:AMZN) and Microsoft (NASDAQ:MSFT) — have done the same things. Tapping into advertising, cloud computing and other segments to drive growth.

I’m not saying JD stock is a one-trick pony, but it lacks in size and momentum compared to BABA.

That said, it doesn’t make JD a bad company. Analysts expect sales to grow ~17% this year and next year. That goes alongside nearly 100% earnings growth in 2019 and ~50% growth in 2020.

The problem though? Valuation and the bottom line. As revenue continues to grow, the bottom line has really struggled. After losing more than half a billion dollars (-3.8B CNY) in 2016, JD was basically back to breakeven operation in fiscal 2017. Dropping back to a loss of more than $350 million in fiscal 2018 has derailed momentum, though.

While analysts are calling for non-GAAP earnings to almost double this year to 69 cents per share, that still leaves JD stock trading at almost 38 times earnings. Not exactly a bargain when one can buy BABA with ~50% better revenue growth and a price-to-earnings ratio that’s almost 40% lower.

So better growth and a cheaper stock? Got it. Still, that doesn’t mean JD stock is worthless or shouldn’t be owned. Those who want exposure to the Chinese e-commerce market may find it attractive. Just make sure it holds ~$26.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMZN and GOOGL.