Aurora Cannabis (NYSE:ACB) recently reported earnings and sales came up short. As such, Aurora Cannabis stock sold off. It’s been a painful run for cannabis stocks over the past few months as they desperately lack a catalyst to send their share prices higher.

Earnings clearly won’t be it for Aurora Cannabis stock at this point. However, there is one silver lining to the recent decline: no new lows.

That’s right. Sometimes good news can be found in bearish developments. Should ACB stock log a higher low, then it may be on the road to recovery. Let’s explore:

Revenue Miss

On September 11, Aurora Cannabis reported revenue of 98.84 million CAD. That missed analysts’ expectations by more than 4.5 million CAD. While that many not seem like a big deal, investors have to take the miss in context.

It’s the company’s second straight revenue miss and its fifth miss out of the last six quarters. Further, Aurora Cannabis doesn’t have the type of valuation that supports its stock price when it misses on top-line sales. That goes for most if not all of the cannabis industry, including Canopy Growth (NYSE:CGC), Aphria (NYSE:APHA), Tilray (NASDAQ:TLRY), Cronos Group (NASDAQ:CRON) and others.

In other words, these companies have incredibly high valuations that are all banking on equally incredible growth. And while sales quintupled year-over-year in the most recent quarter for ACB, it came up short of expectations.

It doesn’t help that margins have been under pressure as well.

It’s not that Aurora Cannabis has a poor balance sheet or that the cannabis market is hitting a dead end. It’s that sentiment is not bullish, and momentum is bearish for cannabis stock right now. ACB and others need some positive catalysts, and missing headline expectations isn’t one of them.

Trading Aurora Cannabis Stock

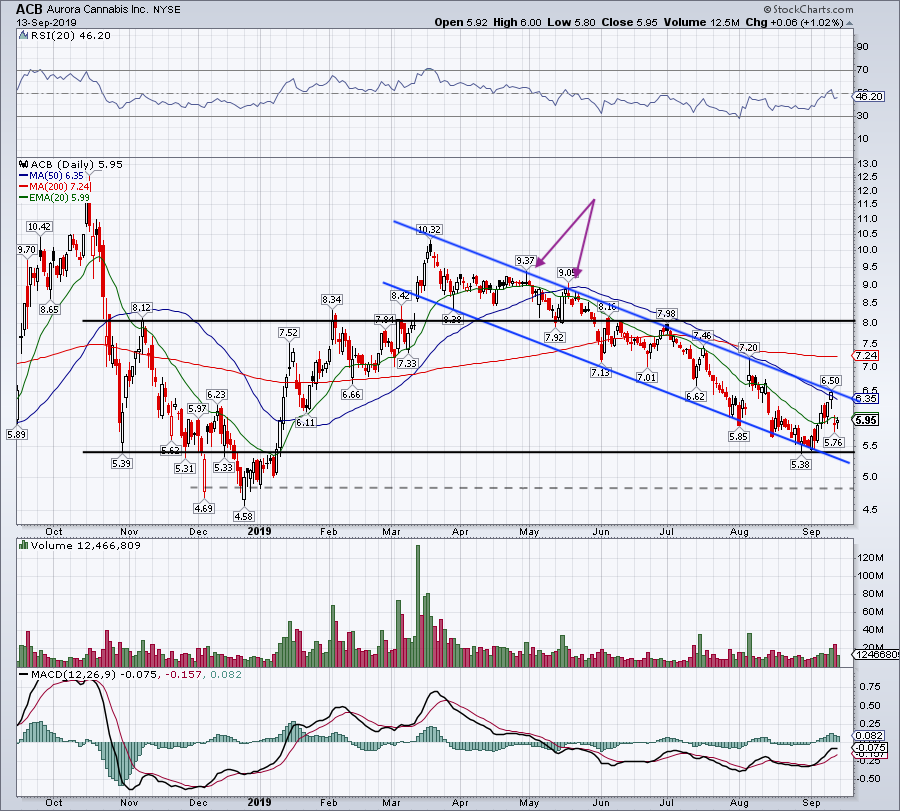

Ahead of earnings, Aurora Cannabis stock had rallied through the 50-day moving average. However, it ran right into downtrend resistance (blue line). Had the results been strong, investors may have been in store for a strong finish to the week.

Click to Enlarge

Now, shares are down about 8.5% from Wednesday’s close. With the fall, the ACB stock price is back below the 20-day and 50-day moving averages. When these two moving averages went from support to resistance is outlined very clearly on the chart via purple arrows.

That was a prelude to failing support that ushered in a wave of selling. Luckily for InvestorPlace readers, they saw this break months ago and have been able to sidestep some of the pain.

The post-earnings decline also solidified downtrend resistance. As we discussed at the top of the article though, the silver lining is that ACB stock has not made new 2019 lows — at least, not yet.

From here, bulls need to make sure Aurora Cannabis stock stays above $5.40. If this level gives way, a test of downtrend support becomes possible, as does a test of the $5 mark. Instead, if ACB stock can hold up and avoid a new low, it can start to work higher despite a lower-than-expected revenue result. Rallying on weaker-than-expected results can be viewed as a bullish development, as it may suggest all the bad news is priced in.

The simple way to evaluate Aurora Cannabis stock from here? Note the $5.40 benchmark. Below it is bad, above it is constructive.

Bottom Line on ACB Stock

Let’s not mince words here: Aurora Cannabis is very much a speculative “prove-it” stock. That is, it’s not a blue-chip name like Microsoft (NASDAQ:MSFT) or Apple (NASDAQ:AAPL). Nor is it a dependable staple going through a hard time like Boeing (NYSE:BA).

While Aurora Cannabis is one of the notable names in a high-growth emerging industry, it’s still a speculative name that needs to prove to investors that it can turn that revenue growth into cash flow and continue to expand with discipline. From CFO Glen Ibbott:

We continue to see strong growth in cannabis revenues in both medical and consumer categories. Our cultivation execution continues to drive production costs lower and improve gross margins. Aurora’s diversified product portfolio remains in demand with patients and consumers alike.

Aurora has seen a significant increase in assets, climbing from $1.43 billion at year-end 2018 to $4.2 billion in its most recent quarter. In the same time frame, total liabilities have increased from $253 million to approximately $850 million. While liability growth outpaces asset growth, its assets far outweigh liabilities.

ACB has staying power, at least in the short term. But what it and the recent of the cannabis space really need is a catalyst and better sentiment.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.