Earnings season is working out reasonably well for U.S. stocks so far. The S&P 500 set an all-time closing high on Friday, and then posted a 0.56% gain on Monday.

Of course, there’s still work left to do. Key earnings reports from the likes of Apple (NASDAQ:AAPL) and Facebook (NASDAQ:FB) loom. But the fear in the last couple of weeks has been that history would repeat. Stocks plunged at the beginning of last year’s fourth quarter and fell sharply during the heart of last quarter’s earning season.

So far, investors have shrugged off those fears. And there’s some logic to the gains. The U.S. economy, and the U.S. consumer, both remain strong. External risks like the trade war and Brexit persist. But they should be resolved at some point, leaving potential catalysts for more upside in the not-too-distant future.

Of course, this also is the eleventh year of both a bull market and an American economic recovery. A downturn on both fronts, too, should arrive at some point. Valuations have recovered since last year’s sell-off, with cyclical stocks in particular posting huge gains in 2019.

This week’s three big stock charts focus on a sector that highlights the potential risks and rewards of the broader market: the airline industry. Stocks in the space, like the market as a whole, seem cheap enough that the rally can continue. But external pressures create risks both near-term and long-term — just like the rest of the market.

Boeing (BA)

Boeing (NYSE:BA) quite obviously has risks beyond those facing the rest of the market. The pair of 737 MAX 8 tragedies have weighed on BA stock since March. That said, the first of our three big stock charts still highlights broader market questions. For BA stock itself, however, there’s one pressing question at the moment:

- When does Boeing stock finally break? Costs related to the 737 MAX 8, between fines, legal liabilities, and contractual payments to customers no doubt will reach well past $10 billion. That’s admittedly a manageable figure, as it represents likely less than 10% of a current $191 billion market capitalization. And Boeing continues to insist that the MAX will return to service this quarter, though increasingly frustrated customers seem to believe otherwise.

- From the chart, it seems like investors aren’t quite sure what to think. A longer-term downtrend has held since March. But August lows have held as a bottom, and even a sell-off following last week’s Q3 report attracted some buyers. At 16x forward earnings, BA stock is cheap enough that it can rally once investor attention turns back to long-term prospects.

- That shift in attention, however, requires two catalysts. First, Boeing has to actually get the 737 MAX in the air. Second, bulls need to be correct in arguing the lack of competition for Boeing and rival Airbus (OTCMKTS:EADSY), combined with increasing developing market demand for air travel, will allow the company to resume growth. In other words, the case for BA stock comes down to execution and cooperation from the global economy. That’s the case for many stocks at the moment. But at this point, investors willing to take economic risks elsewhere in the market may be far less willing to bet on Boeing’s execution improving.

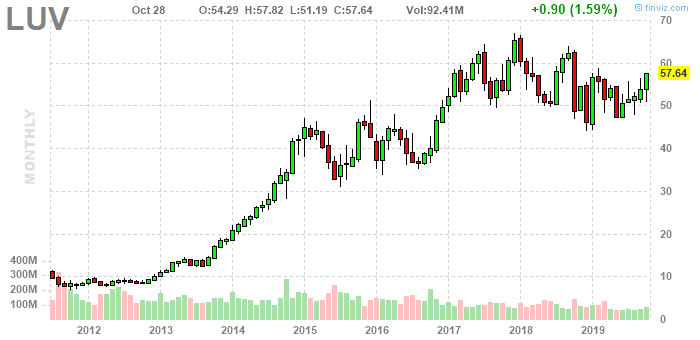

Southwest Airlines (LUV)

Southwest Airlines (NYSE:LUV) is one of those frustrated Boeing customers. In fact, Southwest was the world’s largest operator of the 737 MAX 8. The grounding has created significant costs, including some $210 million in the third quarter alone. Those costs will continue for several more months: the company already has pulled the plane from its schedule through February.

But thanks to a Q3 earnings beat, investors are starting to look ahead for LUV stock. Shares now have bounced 20% from August lows, and the second of our big stock charts shows more potential upside ahead:

- From a near-term standpoint, LUV stock clearly is headed in the right direction. Investors have tacked on more gains to the 5.7% gain posted the day of the Q3 report. Steadily higher highs and a stock well clear of moving averages suggest that strength could continue.

Click to EnlargeFrom a longer-term perspective, there’s still reason for upside here. February highs at $59 offer the next level of resistance, but Southwest Airlines stock still sits well below past highs. There’s little reason at the moment to believe that LUV stock can challenge late 2017 peaks above $65.- Fundamental arguments buttress that case. Competition in the U.S. airline industry finally seems rational, to the point that Berkshire Hathaway (NYSE:BRK.A,NYSE:BRK.B) finally reversed field and bought airline stocks. That includes Southwest, which has sparked rumors that Berkshire might actually buy the entire company.

- Meanwhile, LUV stock, at less than 12x FY20 consensus earnings per share estimates, is cheap enough to rally. That’s particularly true given that those estimates include residual impacts from the MAX 8. It might be LUV stock, not BA stock, that could be the more attractive play on the plane’s return to service.

Delta Air Lines (DAL)

For Delta Air Lines (NYSE:DAL), the broad case seems similar to that of LUV stock. DAL stock in fact is even cheaper, at 8x forward earnings. Delta has a bigger international business, which should give it more exposure to developing markets. Rational U.S. competition should be a benefit as well.

But both technically and fundamentally, DAL looks potential weaker at the moment:

- The last of our big stock charts isn’t nearly as attractive. DAL stock has pulled back from July highs, with its third quarter update at the beginning of the month sending the stock down 4.7%. Recent gains do suggest some optimism, as DAL has cleared the 20-day moving average. The 200 DMA presents a clear near-term challenge, however.

- Meanwhile, Delta actually has no exposure to the 737 MAX. Counterintuitively, that may be a risk. The lack of the MAX has helped near-term results — but creates tougher comparisons next year. While rival airlines can “get back to normal” and see higher growth, Delta already is at normal. Recent trading suggests that “normal” hasn’t been quite good enough.

- To be sure, DAL still is intriguing. $52 turned from resistance earlier this year to support, which suggests some protection to the downside. 8x forward EPS is a multiple that can expand, even if airline stocks generally receive below-market multiples. As a member of one of the few value sectors that has failed to rally since the 2016 election, DAL stock is a particularly intriguing choice for investors who believe the broad market still has several years of upside.

- But the valuation discrepancy to LUV highlights two key issues. First, the lack of a Boeing-related catalyst. And second, lower trust in Delta against a low-cost leader that has been of the market’s best stocks for some four decades now.

As of this writing, Vince Martin has no positions in any securities mentioned.