International Business Machines (NYSE:IBM) has been struggling not just for a few months, but for years. It’s one of the old tech stocks that just never seemed to find its mojo, as IBM stock price has climbed just 20% over the last ten years.

Other “dinosaur” tech plays have done much better during that time. VMWare (NYSE:VMW) and Oracle (NYSE:ORCL) have rallied 156% and 270% over the past ten years, respectively. Microsoft (NASDAQ:MSFT) has exploded more than 430% in that time and let’s not even look at the FAANG names.

That said, International Business Machines stock is still here and not in the graveyard like so many others. Let’s look at some pros and cons of this 108-year-old company.

Low Valuation, Low Growth

IBM stock trades at a rather paltry 11.1 times this year’s earnings. That’s not its lowest price-earnings ratio ever, but it’s pretty darn low for a tech company. For comparison, MSFT and VMW both trade with P/E ratios in the 20s, while Oracle trades at about 14 times its earnings.

Oracle’s P/E may not seem like much of a premium to that of IBM, but if the latter was to suddenly trade at 14 times its earnings, IBM stock price would rally about 25%.

However, while IBM stock may have a low valuation, it also generates painfully low growth. Analysts, on average, expect its earnings to fall 7.2% this year before rebounding 4.9% in 2020. On the top line, analysts, on average, predict another down year in 2019, calling for a 2.1% decline. In 2020, average estimates call for a 4.1% increase, though.

During a down 2019, it’s hard for investors to “back up the truck” on IBM stock i.e. buy a lot of it. But with growth expected to return in 2020, perhaps more investors will buy International Business Machines stock as we get closer to the next fiscal year.

High Dividend, Little Return

The dividend of IBM stock currently yields about 4.5%. That’s a very solid yield, no matter what type of stock we’re talking about. At the same time, though, that high yield is indicative of the lack of demand that’s plaguing IBM.

If demand for the shares was higher, the yield would be lower and IBM’s performance would be much stronger than a sub-2% compound annual growth rate over the last decade.

At the end of the day, the type of investor you are will determine your view of International Business Machines stock. If you’re only focused on income, then IBM stock can be attractive. Its payout is solid, but its lack of return over the last decade is a con. I personally would rather buy a stock with a yield between 2% and 3% if it can potentially deliver a much better total return.

So while the dividend is a pro, IBM’s total return is a con, but for some investors, one metric may matter much more than the other.

Better Use of Cash

For many years, investors were banking on buybacks of International Business Machines stock to boost IBM stock price. That didn’t really materialize, even though its management bought back huge amounts of stock every year.

Over all those years, IBM could have been grabbing small- and mid-cap companies that would have been game changers today. Obviously hindsight is 20/20, but names like Adobe (NASDAQ:ADBE) or Salesforce (NASDAQ:CRM) could have potentially been in IBM’s arsenal now.

Instead, it took until 2018 for IBM to buy Red Hat. The $34 billion deal wasn’t bad, but it feels like too little, too late. Red Hat is a solid company, but IBM paid about ten times 2018 sales for it. Further, Red Hat is barely profitable, although it does have a solid subscription revenue base.

At the end of the day, it’s a solid asset, but IBM paid a big price for it and missed out on many opportunities over the last five to ten years. Instead, it opted to buy its own stock, which proved to be a very poor investment decision.

Trading International Business Machines Stock

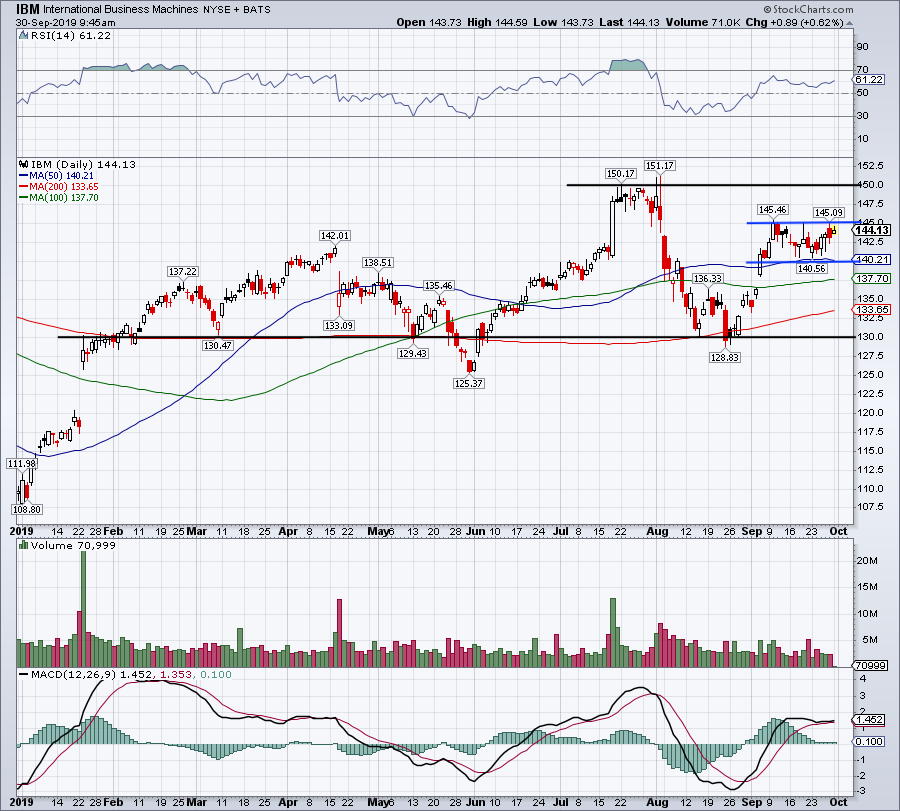

Click to Enlarge

When looking at a six-month chart of IBM stock price, investors can see that the shares have been relatively range-bound since the stock surged in January.

During that time, range support has shown up around $130, while $150 was resistance in July. Currently, International Business Machines stock is moving in an even smaller range, between $145 resistance and $140 support. Further, IBM has a 61.8% retracement at $141.31 and a 78.6% retracement at $145.65.

We now have a setup.

IF IBM breaks below its $140 support and the 78.6% retracement level, the shares will likely drop to their 200-day moving average. If it drops below that, it can reach its $130 range support. If it breaks out over $145 and the 61.8% level, then the $150 resistance is on the table.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.