Like many names in big tech, Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) came roaring back to life. GOOG stock is up 26.2% from the lows. The rally has caused many investors to assume shares need to pause before going higher again, especially with earnings on Tuesday.

However, the rally in GOOG stock actually lags the broader market. Both the S&P 500 and the Nasdaq have outperformed Alphabet, rallying 29.7% and 30.2%, respectively. In fact, all of FAANG has outperformed Alphabet, too.

Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX) are each up almost 50% from the lows and hit new all-time highs this month. Apple (NASDAQ:AAPL

) is up 33% and Microsoft (NASDAQ:MSFT) is up 31.7%, while both stocks still sport market caps in excess of $1 trillion. Even Facebook (NASDAQ:FB) is up almost 40%.

In that respect, it feels like GOOG could be the catch-up play.

Earnings Concern

There is a worry when it comes to Alphabet, given how much of its revenue is driven by online advertising. The company may be seeing a big uptick in usage — ranging from Google.com to YouTube — but many in the industry believe increasing traffic will not be enough to offset digital ad declines. Unfortunately for investors, that’s probably true.

However, the stock market is a game of expectations. Investors know that January and February were mostly okay. In other words, it was business as usual. March was the real shake-up month here in the U.S., where businesses began to shutter and stay-at-home orders were put in place.

That carried over into the second quarter, where almost every business is surely off to a slow start. If Google tells Wall Street that it’s starting to see advertisement revenue trough and believes the second quarter will be the bottom, then the stock likely has upside.

The stock market is a forward-looking investment vehicle. Yes, it cares about the quarter that will be reported and how business is going right now. But it cares even more about how business will be doing in three, six, and nine months from now.

In that sense, it all becomes very simple. If investors perceive that business has or will bottom soon, will be in recovery next quarter and back to usual by year-end, then there’s a good chance they bid GOOG stock higher. If they believe this downturn will persist for some time with many unknowns in the way, then shares likely have downside.

Catch Up Trade?

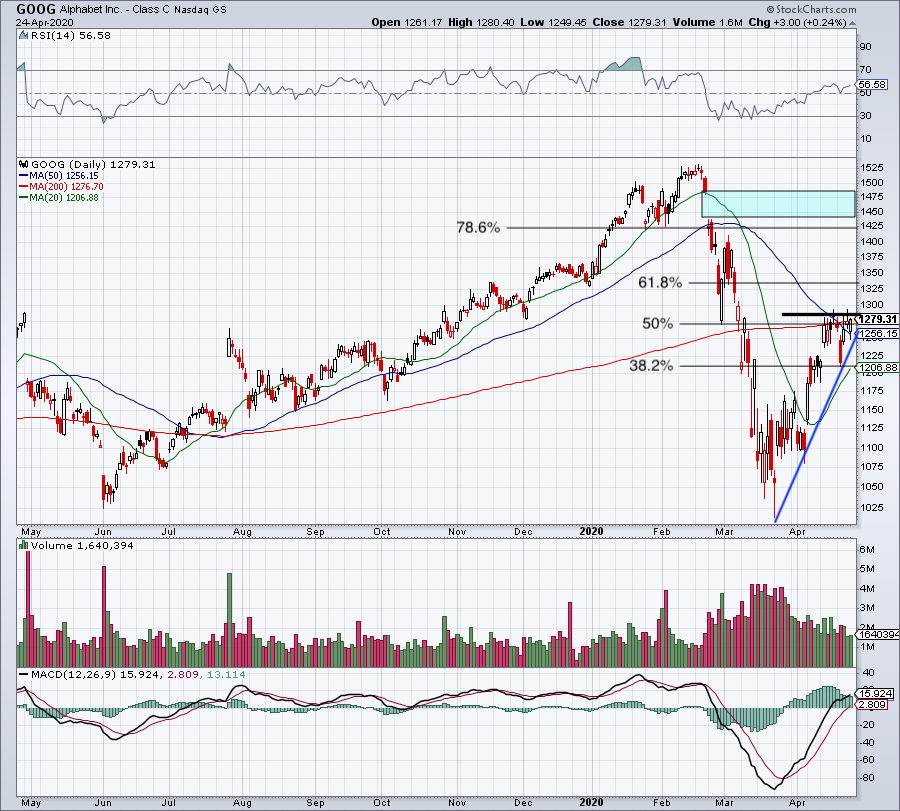

Click to Enlarge

I think GOOG stock can rally if we get a better-than-feared earnings report. The whole industry is worried about shrinking marketing budgets. Essentially, when other businesses are under pressure, so too are their advertising budgets. That negatively impacts Facebook, Amazon and Alphabet, among other social media and media platforms.

However, because the rebound has been so tepid when compared to its FAANG peers and the broader market, there’s upside potential here should the results not stoke widespread fears about the online ad market.

Technically speaking, investors have to love the way shares are bubbling below the 200-day moving average and this ~$1,285 area. For the last two weeks, GOOG stock has been chopping around in a relatively tight range, waiting for some kind of move to develop.

Currently over the 50-day and near the 200-day moving average, a break higher over $1,300 could put bulls back in control. That could happen in a pre-earnings rally (shifting more risk onto the long side) or it could happen as part of a relief rally after the print.

Earnings are a guess — no one knows how they will unfold. But if Alphabet gets some momentum, it has room to the upside as investors play catch-up vs. the field.

Bottom Line on GOOG Stock

Despite the likely short-term hit to business, it’s surprising more investors aren’t putting money to work in GOOG stock. First, the company has one of the strongest balance sheets out there. That type of certainty alone should be enough of a reason for investors to pick up a few shares of Google on the decline.

The company sports total cash of almost $120 billion vs. no current debt and just $3.9 billion in long-term debt. Current assets of $152.5 billion are more than triple the $45.2 billion in current liabilities. In short, Alphabet has enough cash to last until the end of time and that should create confidence in investors, not fear.

While GOOG stock faces short-term headwinds, it has long-term secular drivers in play — whether that’s online or on the road via its autonomous driving Waymo unit. At the end of the day though, it won’t pay to bet against Alphabet. Instead, bet on the long term.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.