Today, keeping safe amid the novel coronavirus crisis is a priority for many people as they are restricted to home. That said, investing in solid healthcare stocks is perhaps one way to reinforce that priority.

I wanted to find cheap, but sturdy healthcare stocks that would be worthwhile investments. To be sure, this is the opposite of investing in a speculative new coronavirus cure stock. Well, it’s almost the opposite. Investing in a financially healthy, but now cheap healthcare company is one way of supporting these companies.

These companies want solid, long-term investors who won’t force them into speculative ventures, or disastrous acquisitions.

I found five medium to large capitalization healthcare stocks that are financially profitable, but also very cheap. For example, these stocks have price-earnings (P/E) ratios that are at 10 times earnings or below.

In addition, they all pay dividends, and the dividends are well-covered by earnings. In fact, their average dividend yield is about 4% or so.

Lastly, each one of these companies are heavy free cash flow (FCF) generators. For example, the level of FCF compared to the stock price is around 11% or greater. This is called their FCF yield.

This ratio is important because FCF is what pays for the dividend, software, capital expenditures and debt reduction. It also allows a company to increase its cash balance, as well as pay for acquisitions.

So, here are the five healthcare stocks that have low P/E ratios and ample yields:

- CVS Health (NYSE:CVS)

- Walgreens Boots Alliance (NASDAQ:WBA)

- AbbVie (NYSE:ABBV)

- Bristol-Myers Squibb (NYSE:BMY)

- Cardinal Health (NYSE:CAH)

With all of that in mind, let’s dive in.

Hot Healthcare Stocks: CVS Health (CVS)

Click to Enlarge

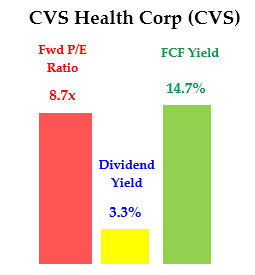

CVS Health is an $80 billion market cap stock that has over 9,900 retail drug stores land 1,100 MinuteClinic locations. To put it succinctly, CVS Health is thriving in the midst of the coronavirus crisis in the U.S. Moreover, CVS stock is cheap at just 8.7 times expected earnings.

For example, CVS Health’s revenue was up 8.3% to $66.8 billion in Q1. Moreover, its free cash flow grew to more than $2 billion from a loss of $38 million in FCF last year.

This is a very strong company. Despite the pandemic, people are shopping at CVS more. It also reported that 90-day prescriptions have risen, and people are also filling their maintenance prescriptions earlier.

This is due to CVS Health’s late 2018 acquisition of Aetna, a giant health insurance company. In fact, CVS CEO Larry Merlo said one purpose of the deal was to increase “personal contacts and deeper collaboration with their primary care physicians.”

Moreover, CVS kept its guidance for the coming year. It also expects a strong second quarter, aided by reduced expenses at Aetna. This means that the stock trades for a very cheap P/E ratio, below 9 times forward earnings.

Additionally, CVS’s dividend is very secure. The dividend yield is 3.3%, but the FCF yield is much higher at almost 15%. This means that there is plenty of FCF to pay the dividend.

All in all, this is a great healthcare stock for the long-term investor.

Walgreens Boots Alliance (WBA)

Click to Enlarge

Walgreens is a $36 billion market cap stock in the pharmacy business. It has more than 18,750 stores in 11 countries, as well as over 400 distribution centers. In the U.S., it has 9,277 stores under the Walgreens and Duane Reade name.

Moreover, Walgreens had a great second quarter. Its revenue was up 3.7% to $35.8 billion compared to Q2 2019. However, its gross, operating and net earnings were down year-over-year. The company has been in a store optimization program since 2018 in an attempt to reduce costs and close 750 poorly performing stores.

Much of the lower earnings results were from non-cash related expenses. For example, its cash flow from operations increased over 100% to $2.5 billion in the first half of its fiscal year.

In addition, free cash flow grew more than 400% to $1.8 billion as a result of its restructuring efforts. This means that the company has a very good FCF yield. FCF will be more than $5.2 billion this year, the same as last year. This gives the stock a FCF yield of over 14.5%.

Moreover, its dividend yield is very attractive at 4.4%, which is well covered by the FCF yield as mentioned above.

The company did not provide any future guidance post the coronavirus pandemic effect on their business after the quarter ended on February 19. Prior to this, they were expecting a flat performance compared to 2019.

Nevertheless, I suspect that performance may not suffer very much based on the guidance given by CVS Healthcare. As discussed above, people have been using prescriptions a lot more. This is essentially a very good business situation for a drug store chain like Walgreens.

Walgreens is a sturdy, value stock that is worthy of investigation by value investors.

AbbVie (ABBV)

Click to Enlarge

AbbVie is a large $127 billion market cap drug stock. I have written before about AbbVie and its fast-growing dividend per share. ABBV stock is cheap with a forward P/E ratio of just 8.7 times. In addition, its dividend yield is very attractive at 5.5%.

Moreover, AbbVie’s $63 billion purchase of Allergan — expected to close shortly — will boost earnings and dividends and push ABBV stock higher. Allergan is well known for its Botox and other beauty products. And on May 5, AbbVie received antitrust approval in the U.S. for the acquisition.

According to Reuters, the deal will help AbbVie to diversify its earnings and “buys time” before its arthritis drug Humira goes off-patent in 2023. The deal is expected to close this month.

That said, look for analysts to begin upgrading the stock as it starts to post combined partial earnings during Q2 and fully consolidated Q3 for the two companies.

Meanwhile, I expect, based on last year’s FCF, the FCF yield is at least 10% — fully covering the dividend of 5.5%. This is an interesting value stock.

For example, the company has provided an EPS outlook of between $9.61 and $9.71

for 2020. That puts the stock well below 9 times earnings at today’s price. That said, this is a very attractive price for a solid, above-average dividend-paying stock.

Bristol-Myers Squibb (BMY)

Click to Enlarge

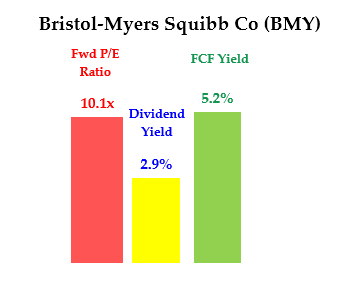

Bristol-Myers Squibb is a large $141 million market cap drug company which is also very cheap. Its forward P/E is about 10 times and its dividend yield is attractively priced at 2.9%.

In mid-November 2019, Bristol-Myers Squibb completed the acquisition of Celgene for $80 billion. In addition, a contingent value right (CVR) for $9 per Celgene share was issued, trading under the symbol CELGZ on NASDAQ.

Moreover, Bristol-Myers Squibb reported strong growth in Q1 on May 7, including 13% higher revenue with its Celgene division. This is a pro-forma calculation assuming the acquisition occurred on Jan. 1, 2019. Much of this increase came from the Celgene acquisition and its cancer drug, Revlimid.

The company projected that its 2020 earnings will reach between $6 per share and $6.20. That puts the stock on a forward P/E of just 10 times at the mid-point of its outlook.

My estimate is that the FCF yield is over 5% based on its trailing 12 months-FCF. This more than covers the dividend which also has an attractive yield of almost 3%.

Value investors should look further at BMY stock, especially as the combination of both companies. Moreover, the company said that the coronavirus pandemic increased its sales by about $500 million. So this event is acting as a catalyst for the company.

Cardinal Health (CAH)

Click to Enlarge

Cardinal Health is a $15 billion market value integrated health services company. It owns hospitals, pharmacies, surgery centers, clinical labs and physician offices. However, 75% of its revenue comes from generic drug distribution business.

Cardinal Health is cheap based on its involvement with opioid class action lawsuits. That said, Seeking Alpha reported in February that both sides are trying to reach a national settlement soon. It appears that payouts will be lower than expected. That said, CAH stock could rise as the worst seems to be already discounted in the present market valuation.

Another author in Seeking Alpha has written that Cardinal Health is expected to have good results based on its sales of personal protection equipment.

As of mid-February, the company had provided an outlook of earnings per share of between $5.20 and $5.40 per share. And when the company reported earnings on Monday morning, they reaffirmed that fact.

So far, it has not adjusted that increased estimate from the last time it provided guidance. Sales of its PPE and other pandemic-related products may have boosted its earnings.

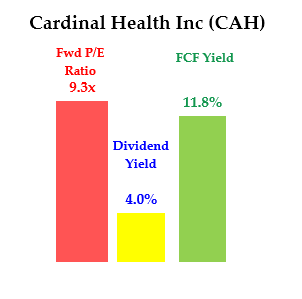

Overall, CAH stock is cheap at 9.3 times forward earnings, a dividend yield of 4% and an estimated FCF yield of 11%. Therefore, CAH stock is worth a careful look by value investors for these reasons.

Healthcare Stocks Summary and Conclusion

If you look at the table below, you see that this group of five healthcare stocks offer attractive valuation metrics for the careful investor. As a group, these stocks offer an average price-to-earnings ratio of below 9 times earnings, plus a dividend yield of 4%. Here is the table:

Moreover, the dividends are well covered since the average free cash flow is over 11%, which is higher than the 4% dividend yield.

Look to invest in these companies at attractive points over the next month or so. The reason is the valuations seem to offer an acceptable margin of safety for most value-oriented investors. Some of the companies are going to report their earnings outlook within the next few days. It might even be worthwhile to take a stake before those numbers emerge.

Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks. Subscribers receive a two-week free trial. As of this writing, he did not hold a position in any of the aforementioned securities.