For both good reasons and not so good, the airline industry has been under the spotlight. If there’s any consensus here, it’s that Southwest Airlines (NYSE:LUV) is the better bet. Thanks to a superior financial position relative to competitors, LUV stock has the best upside opportunity.

But how realistic is this assumption?

Over the last several weeks, the domestic airliners, which includes heavyweights like United Airlines (NASDAQ:UAL), Delta Air Lines (NYSE:DAL) and American Airlines (NASDAQ:AAL), have seen their share prices fly substantially higher.

The bullishness is not without fundamental justification. With states reopening their economies, along with robust retail sales which implies a resurgent consumer base, this is great news for LUV stock and its ilk.

Further, Southwest’s management team bolstered investor confidence, reporting improvements in passenger demand and bookings. Most importantly, load factors – basically, how full each airplane is – improved substantially from April. Additionally, the company expects more gains in June and July to 45% to 55%.

Given the encouraging signs in the underlying consumer economy and other industry-specific data, Cowen analyst Helane Becker gave an “outperform” rating on LUV stock with a $40 price target. With a current price of about $34.25, is now a good time to buy shares?

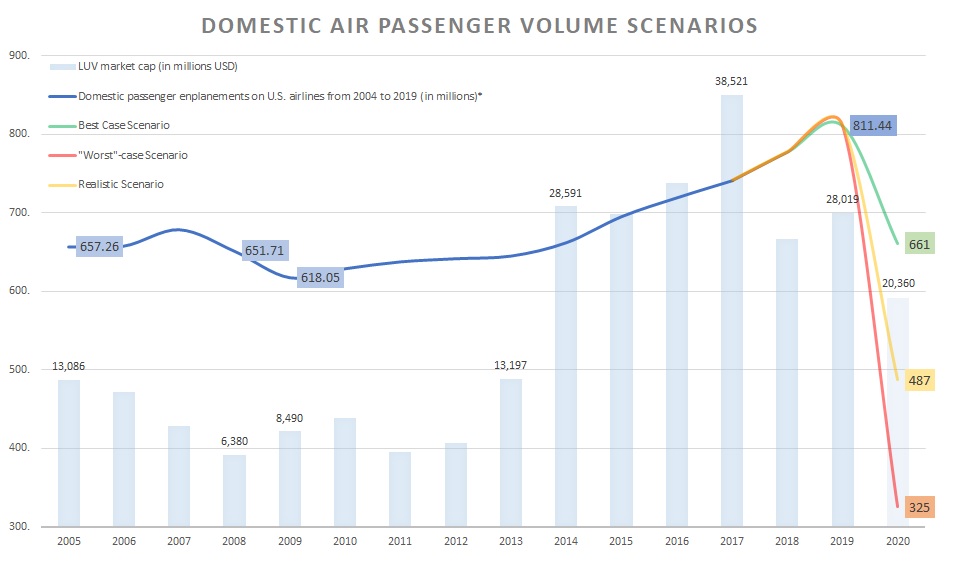

Honestly, it depends entirely on your outlook for domestic flights. Since LUV kicked in their afterburners in 2014, Southwest’s market capitalization per domestic flight passenger averages $40.88. A $40 price implies a market cap per passenger of $29. That’s a steal at

last year’s passenger volume.

LUV Stock Could Be a Buy if the Numbers Work Out

Of course, you can’t trade LUV stock in last year’s paradigm. And this is where Southwest and every airliner in the new normal becomes a tricky affair. Before getting involved in this sector, you should consider a few basic scenarios.

For me, the most intuitive way to forecast an airliner’s trajectory is to compare its market value to passenger demand. I decided to compare Southwest’s market cap per domestic flight passenger against overall domestic passenger volume.

To repeat, LUV’s average market cap per domestic passenger between 2014 to 2019 is $40.88. Essentially, this is my “anchor” point. An assumption of total passenger volume that drives this metric above $40.88 is overvalued and undervalued if the metric drops below it.

In my opinion, the best-case scenario for total volume is 661 million passengers, which is 81.5% of 2019’s volume of 811 million. Long story short, this forecast assumes that for the rest of the year, air traveler demand skyrockets. In this scenario, LUV stock is undervalued with a market cap per passenger of $31.

Click to Enlarge

Of course, this is a highly unrealistic forecast. Currently, average passenger volume (domestic and international flights) for June is less than 20% that of the year-ago level. If this dire trend plays out longer than expected, we could see total domestic volume drop to 40% capacity.

In that case, LUV stock is grossly overvalued.

Naturally, you may wonder what the present price of LUV implies for passenger volume given recent historical market cap per passenger metrics. Using the model above, Wall Street’s present valuation implies 498 million domestic flight passengers in 2020. That’s a 61.4% capacity, which is what I would consider a realistic scenario.

How to Approach Southwest Airlines

I just threw a bunch of numbers at you so allow me to summarize. Based on the model above, which is a model and not set in stone in any way, here are the basic takeaways:

- At the time of writing price of $34.25, LUV stock implies a 2020 domestic flight passenger capacity of 61.4% of 2019 levels. Roughly, this corresponds to a passenger volume of just under 500 million.

- To give yourself a better margin of success, you should consider buying LUV at a price point that implies a lower passenger volume. For instance, at $28.17, this implies volume of approximately 406 million, which is about 50% of last year’s volume. If passenger volume turns out to be 500 million or greater, you got yourself a deal.

- Interestingly, at LUV’s low for the year so far, this price point implies passenger volume of 324 million. That’s almost right in line with my estimate for a worst-case scenario of 325 million passengers, down 60% year-over-year.

Another interesting point is that the current 50-day moving average is $31.49. That’s reasonably close to my “safe-ish” price of $28. Therefore, if you must buy LUV stock, I’d consider getting shares within this range, not at $34-plus.

Take It with a Grain of Salt

As I said, whether you believe LUV stock is good deal depends completely on your assumption of air travel demand. If you knew for certain that passenger demand will enjoy a V-shaped recovery, you’d be crazy to not buy shares.

Of course, no one knows. Indeed, I’d go a step further and say that no one has even a confident forecast. It’s not about the forecaster but rather the unprecedented nature of this crisis.

But if I had to guess, I’d say that all airliners are overvalued at this point. While passenger demand overall has improved, they’ve shifted from comically untenable to garden variety untenable. Unfortunately, 20% capacity is not going to get you anywhere.

Also, I’m very worried about rising coronavirus cases. With many Americans treating the pandemic as fake news, it appears Covid-19 is teaching us a lesson. Also, the combination of nationwide reopening measures and surging protests have not helped in the least.

Should cases rise substantially, that implies greater consumer fear. And in that case, all (long) bets are off.

A former senior business analyst for Sony Electronics, Josh Enomoto has helped broker major contracts with Fortune Global 500 companies. Over the past several years, he has delivered unique, critical insights for the investment markets, as well as various other industries including legal, construction management, and healthcare. As of this writing, he did not hold a position in any of the aforementioned securities.