The numbers can’t be great this quarter. While life seems to be returning to normal, remember that Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL), Facebook (NASDAQ:FB) and other digital ad companies started off the quarter on weak footing. But that hasn’t stopped Facebook or GOOGL stock from running to new highs.

It’s actually pretty remarkable how willing the market has been to overlook the current situation. This isn’t a Department of Justice or European regulatory fine, where the government shakes one of these companies down for a few billion.

This is an enormous hit to the U.S. and global economies. Commerce is being disrupted and unemployment has surged. It’s true that the stock market is a forward-looking mechanism, but after fading 32% in a month, raise your hand if you were looking for a 63% rally in the Nasdaq Composite in just 17 weeks.

Google’s run is also impressive. Despite a prolonged hit to revenue, investors are willing to overlook the situation and bid GOOGL stock higher. The question is, should they?

Breaking Down GOOGL Stock

The novel coronavirus presents us with one giant issue in the investment world: unknowns.

We don’t know how long it will persist, how many waves it will have or how many cases there will be. Therefore, we don’t know how long it will impact the economy or commerce.

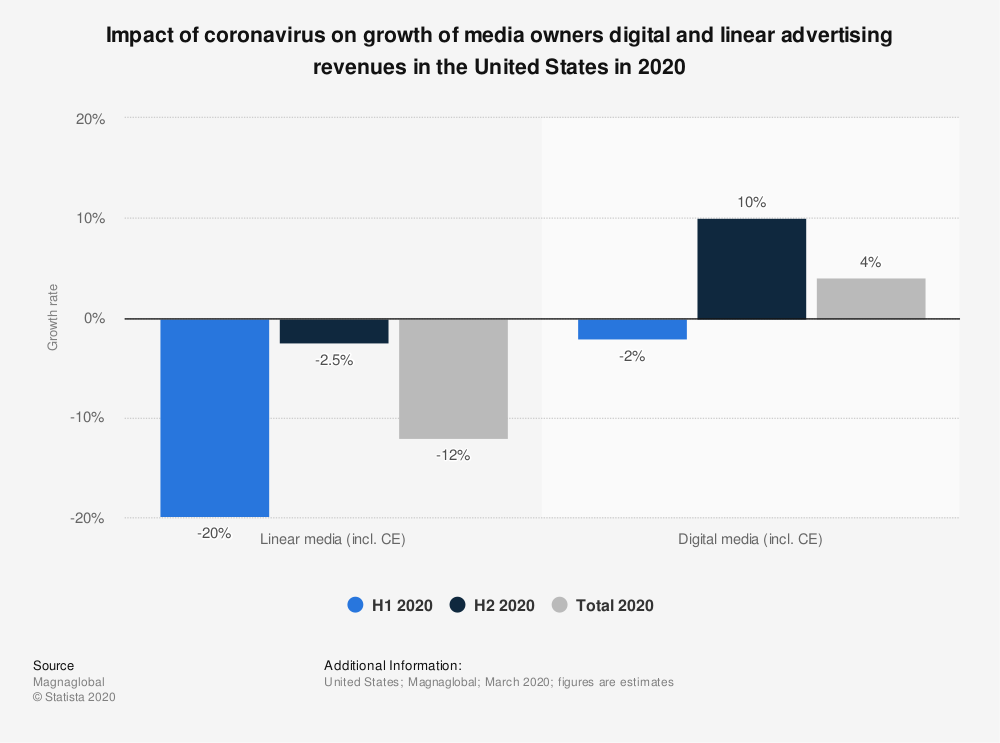

Click to Enlarge

However, we do know that it is driving consumers online and away from physical retail locations. Companies like Amazon (NASDAQ:AMZN) are bursting with demand. Brands like Nike (NYSE:NKE) and Lululemon (NASDAQ:LULU) are seeing a surge in online orders.

That’s a positive for a company like Alphabet. While ad revenue may still be pressured, there is demand among those buying ads. That’s going to support the company’s revenue, even if the growth is lumpier than usual.

Estimates have crept higher over the last few months, but 2020 is essentially setting up to be a wash for Alphabet.

Analysts expect 4.6% revenue growth this year before a rebound to 20.7% growth next year. On the earnings front, consensus expectations call for a 15% decline this year and 32% growth in 2021.

With YouTube and Google — the internet’s two most popular sites — Alphabet is in prime position to capture ad revenue growth when ad spending returns. With more people on the internet than ever before, Google will get paid one way or the other. That’s clear on the graph above, which highlights the discrepancy between linear advertising and digital advertising. The latter is more insulated and better protected amid the disruption.

Finally, Alphabet has a robust balance sheet. The company is sitting on $117.2 billion in cash and $147 billion in current assets. That’s against current liabilities of just $40.2 billion and long-term debt of less than $4 billion.

Evaluating Alphabet Ahead of Earnings

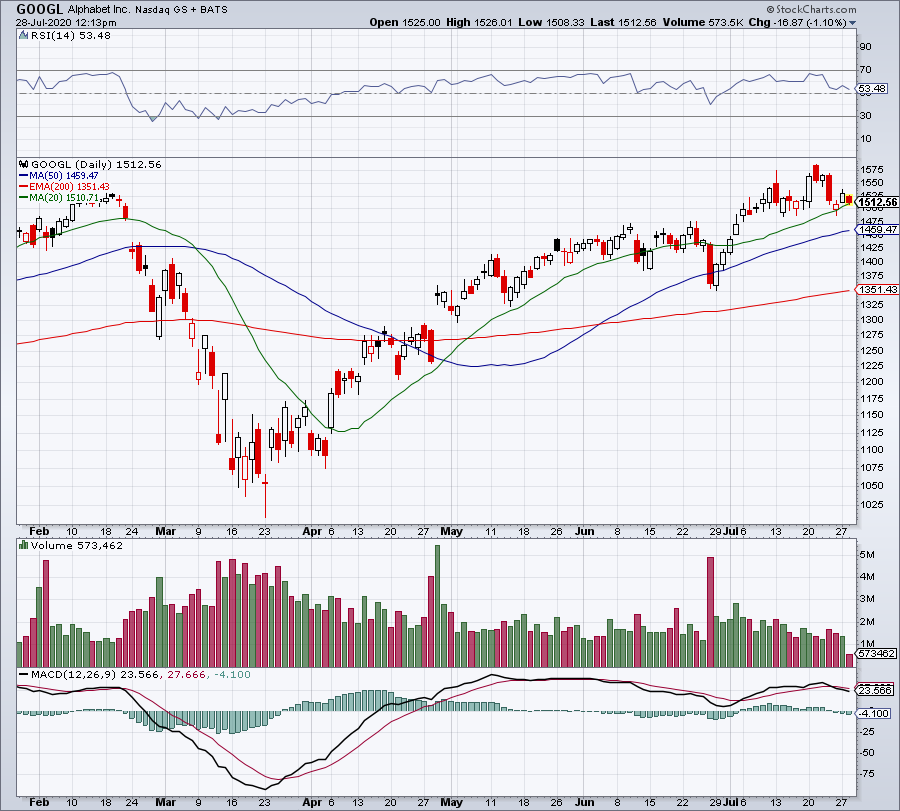

Click to Enlarge

When the company reports earnings on Thursday July 30, investors will want to know how the ad market is doing. They will want to know, with certainty, that Alphabet has seen a trough in business and expects it to continue that way.

Last quarter, CFO Ruth Porat said:

“Although we have seen some very early signs of recovery and commercial search behavior by users, it is not clear how durable or monetizable this behavior will be … As of today, we anticipate that the second quarter will be a difficult one for our advertising business.”

In essence, the second quarter will be tough, but there should have been stabilization. In the months since this report, which came in late April, we’ve seen a pretty sizable recovery in the economy. One to justify a run to all-time highs in GOOGL stock? Perhaps not, but that’s not my decision to make.

All I know is that Alphabet has a stellar business in its current form and with its work on the future — like with its self-driving car service Waymo — investors know the company is heading in the right direction.

Lastly, this stock is in a strong uptrend and I’m not one to bet against the trend until it changes. I’m a dip-buyer in GOOGL stock should shares fall on earnings.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.