Just like flying, Spirit Airlines (NYSE:SAVE) is the best bargain when it comes to airline stocks. And did you know, SAVE stock has been one of the best performers over the past few months?

Over the past one and three months, Spirit stock is down 11% and up 20%, respectively. That’s better than a handful of its peers, including Delta Air Lines (NYSE:DAL), United Airlines (NASDAQ:UAL), American Airlines (NASDAQ:AAL) and Southwest Airlines (NYSE:LUV).

However, when we zoom out to the year-to-date and one-year timeframes, that outperformance vanishes. Down 61% in 2020, SAVE stock is in the middle of the pack — third best in this group of five. The one-year look yields a similar result, down 62% and again in the middle of the pack.

So why is this one worth a closer look? Simply because the airlines have made it through the worst quarter they are likely to face. Airport traffic is creeping back up as the country continues to reopen. Let’s look at Spirit Airlines more closely.

Breaking Down SAVE Stock

When Spirit Airlines reported earnings on July 22, the company beat on revenue but missed on earnings. Put simply, the quarter wasn’t good. Spirit reported a loss of $3.59 per share as revenue plunged more than 86%.

Remember though, it’s not about the numbers, it’s about the trajectory. Meaning, it’s about guidance, management’s outlook and where the business is heading from here. In the case of SAVE stock, obviously a massive loss and tremendous drop in revenue does not exactly scream, “Buy! Buy! Buy!”

However, investors are feeling more comfortable with airline stocks now that Q2 is behind them. While management is candid about the situation — Delta said it will take a few years for a sustainable recovery — they also underscored two important themes.

First, liquidity is satisfactory as most of these companies should have enough in the bank to make it through the current crisis. Second, the worst is likely behind the industry. For Spirit specifically, this is encouraging for shareholders: “[W]e were encouraged by our June results and believe they illustrate that when leisure travel demand rebounds and stabilizes, our leading low-cost structure positions us well to be among the first to return to profitability.”

Most airlines saw severe cash burn in March and April, but were able to lower that burden in May and June. Spirit did even better. Excluding a few minor non-operational metrics, “on an average daily cash basis, we were break-even for the month of June,” management said.

At the end of March, current assets and current liabilities both stood at $1.23 billion. In the quarter that just ended in June, Spirit had current assets of $1.66 billion vs. current liabilities of $1.27 billion. In other words, it can cover its short-term obligations, easing concerns about its liquidity.

Bottom Line on Spirit

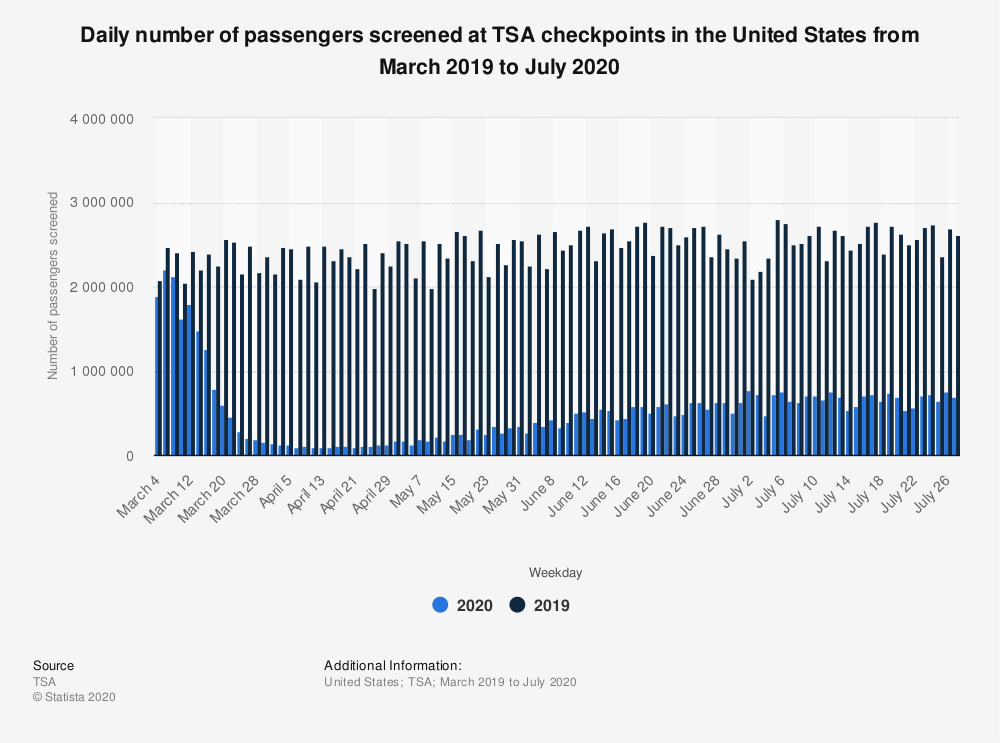

Click to Enlarge

I like SAVE stock for a few main reasons. First, from an operation perspective, the company was able to mitigate cash burn last month. That’s outperforming most of its peers. Speaking of outperformance, its stock has been beating its peers over the last few months.

Third, its liquidity is fine and fourth, as airline traffic returns, Spirit should be one of the early candidates to start flipping a profit.

Of course, we always run the risk of rising novel coronavirus cases pressuring airline traffic. The chart above shows a healthy rebound in airline traffic. However, the rebound leveled off in July as consumers seem to be in a wait-and-see mode.

United Airlines just announced it may need to furlough more pilots than originally expected. The company said that, “In recent weeks, bookings have stalled, and we continue to see an impact of the recent increase in covid-19 cases on our business.”

The risk here is obvious: A rise in or persistent elevation in coronavirus cases may keep the pressure on the airlines.

Eventually though, the world will fly again — air travel isn’t going anywhere. In the meantime, SAVE stock seems like one the best positioned to weather the storm.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.