Target (NYSE:TGT) is one of the lucky retailers out there. In a sector that has been unequally impacted by the novel coronavirus, TGT stock is among a handful of those that continues to do well.

Target is joined by names like Walmart (NYSE:WMT), Home Depot (NYSE:HD), Lowe’s (NYSE:LOW), Best Buy (NYSE:BBY), and Costco (NASDAQ:COST), among others.

At first, some of these names — like Walmart, Target and Costco — were pandemic plays. Consumers flocked to these businesses for food and essential items. Eventually the focus shifted to things to do and buy during a pandemic. That’s where Lowe’s and Home Depot thrived.

Still, more families turned to at-home solutions, which has kept demand elevated at many of these high-quality big-box retailers. Simply put, buying home items, video games, groceries, and other things have kept Target running smoothly.

Business in Demand

It helps that many of these big-box retailers have also shifted toward an omni-channel approach. Keep in mind, this strategy shift has been a multi-year process. It’s not the result of Covid-19 — the latter just happened to accelerate the adoption rate of this service.

Now though, Target, Walmart, and others are seeing robust online sales. It’s helping to drive revenue growth at a time where retail is under pressure. Contrast that to bankruptcy names like J.C. Penney (NYSE:JCP) or department stores like Macy’s (NYSE:M).

These retailers and many others are suffering as consumers pull their spending money from this part of retail and allocate it to different areas. Back-to-school spending should give this area a jolt, though. On the plus side, TGT stock should benefit from back-to-school shopping, too.

In short, Target finds itself in demand amid a global pandemic. From an investment standpoint, that’s all we can hope for.

TGT Stock Has Growth

When it comes to growth, Target is a bit of a mixed bag. On one hand, consensus estimates were calling for revenue of about $78 billion at the start of the year. Those estimates are now just a hair below $83 billion. If Target ends up generating that much in revenue this year, it will represent just over 6% growth year-over-year. In fiscal 2021, analysts expect a slight improvement, with sales up 1.6%.

That’s the good news.

On the downside, Target is actually forecast to absorb a 22% drop in earnings this year. That’s as various Covid-19 expenses add up. In contrast, current consensus expectations call for a 36% rebound in earnings in 2021 to $6.76 per share. If achieved (or exceeded), that will be greater than 2019’s result of $6.39 per share.

Some back-of-the-envelope math pegs TGT stock at a forward valuation of roughly 20 times earnings. That’s not a bad price to pay given the disparity between the haves and the have-nots in the retail space. It’s also not bad given that Target still boasts revenue growth in a difficult environment (which should continue with or without elevated case counts of Covid-19).

Of course, it helps that Target pays a dividend yield just north of 2% at a time dominated by low-interest rates. For instance, the 10-year Treasury bond pays a yield of less than 0.6% at the moment.

Target Stock Could Rally Into Earnings

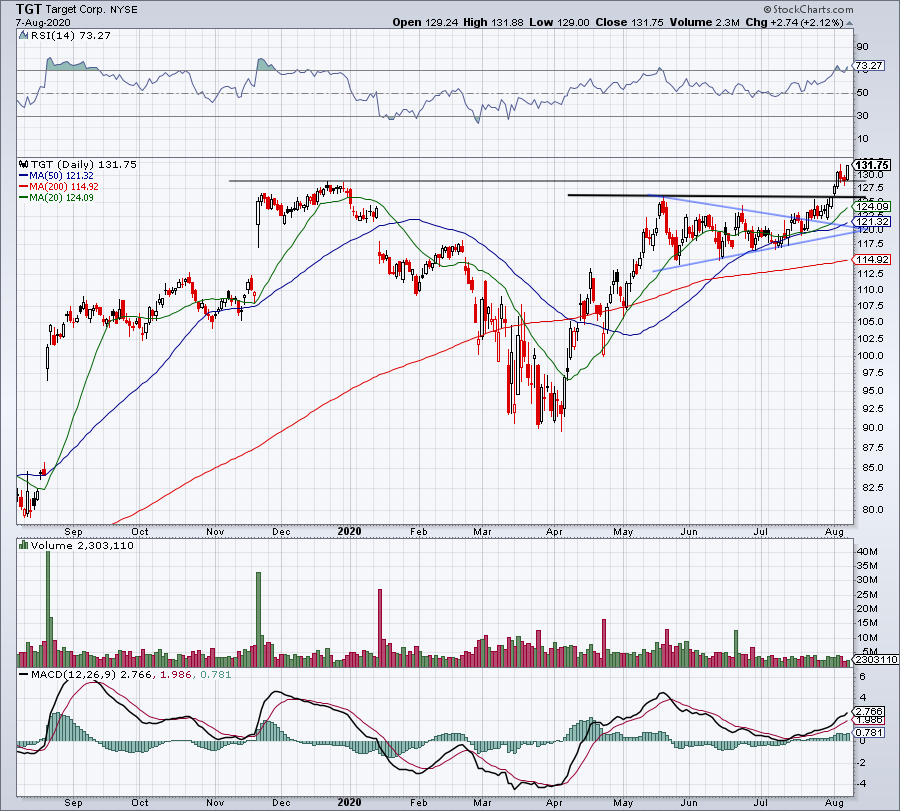

Click to Enlarge

Shares of TGT stock are right near all-time highs as investors continue to bid this name higher. With earnings set for August 19, shares may continue to run up ahead of the event.

As you can see on the chart above, the stock is maintaining above all of its major moving averages. Shares recently broke out over $125, the high from May. Then Target took it a step further and cleared the 2019 highs.

If the broader market cooperates, TGT stock could maintain momentum higher.

If shares continue higher, look to see if Target can get to $138, which is the 123.6% extension. Above that puts $143.77 in play, which is the 138.2% extension. On a dip, I want to see $125 hold as support along with the 20-day moving average.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.