If you’ve never bought a biotech stock before, I don’t blame you. When I made my first-ever biotech bet in my early 20s, things turned out as you might expect:

The company declared “inconclusive” Phase 2 trials, and the stock went to zero. (Thankfully, my second try turned out better).

But biotechs are also some of the best Moonshots out there. Bring a successful drug to market, and your stock will go from $4 to $200; Covid-19 vaccine maker Novavax (NASDAQ:NVAX) achieved this feat in 2020. You learn to live with the duds along the way because the winners more than compensate.

Once in a long while, the odds are tipped even further in investors’ favor. On Monday, gene-editing firm Intellia (NASDAQ:NTLA) announced positive Phase 1 trial results of its treatment for a rare inherited liver disease.

It’s a game-changer.

We’re not just talking about CRISPR technology in crop breeding anymore — a market that is 0.6% of U.S. gross domestic product (GDP). Instead, we’re looking at healthcare, a segment that sucks up 17.7% of American GDP. And Intellia’s success marks the first time in-vivo gene editing has been proven safe for human use.

Today, we’ll take a closer look at the winners of the gene therapy race and the firms that are losing out along the way.

Rising Stars: CRISPR Biotech Firms

It’s rare to see your Mr. Moonshot excited about anything besides… well… Moonshots. But Intellia’s Phase 1 results were extraordinary. Drug platforms can take years to develop — it’s the reason why scientists were stunned that two companies created working mRNA vaccines at the same time to combat Covid-19.

This weekend heralded even more good news for biotech. In a landmark Phase 1 trial, Intellia proved that gene editing could be safe (and potentially effective) at treating genetic orders. Its shares are up more than 50%.

And it’s not too late to jump in. NTLA’s success doesn’t stem from its efficacy — MIT scientists have used in-vivo CRISPR technologies on mice since 2014. Instead, the treatment’s proven safety means those benefits could soon translate into human treatments too. That’s excellent news for the “big-3” of gene editing treatments.

- Intellia (NTLA). In addition to liver disorders, the gene-editing firm is also researching in-vivo treatments for hereditary angioedema and hemophilia.

- Editas Medicine (NASDAQ:EDIT). The seven-year-old company is working on several in-vivo candidates for ocular diseases and ex-vivo for sickle cell and cancer therapies.

- Crispr Therapeutics (NASDAQ:CRSP). The largest CRISPR biotech startup already has four ongoing clinical trials in hemophilia and cancer-beating drugs. Other research includes treatment for Type 1 diabetes, cystic fibrosis and Duchenne muscular dystrophy.

Of course, it won’t be smooth sailing. Competition risks from mRNA vaccine makers are rising, particularly in oncology. And a lot can still go wrong in later phase CRISPR trials. But any winner could easily see their shares triple overnight.

Falling to Earth: Mega-Cap Pharma

Feel bad for Alnylam Pharmaceuticals (NASDAQ:ALNY) shareholders. Intellia’s good news sent its mRNA competitor’s shares down to $155 at one point.

But the existential healthcare crisis runs deeper. Shares of large-cap healthcare companies have stalled. U.S. pharmaceuticals, represented by the IHE (NYSEARCA:IHE) exchange-traded fund (ETF), have risen only 28% in the past five years. Meanwhile, biotech and healthcare providers have motored ahead with 86% and 111% gains, respectively.

The problem? Large-cap pharma companies are finding it harder than ever to profit from small-molecule drugs. Companies like Pfizer (NYSE:PFE) have struggled for years to replace cash cows like Lipitor and Viagra. The consolidating healthcare insurance market has also made it harder for drug firms to raise prices.

In its place, pharma has increasingly relied on M&A (mergers and acquisitions) to fill its pipeline. Investors haven’t been pleased.

On Monday, shares in Regeneron (NASDAQ:REGN) sank 1% even as its partner, Intellia, notched double-digit gains. Investors are presumably worried Regeneron will now have to make an M&A offer that Intellia shareholders can’t refuse.

My advice? Steer clear of legacy drug firms; buying biotech is a more direct way to tap into upside. And what if you want exposure to the marketing side of pharma? Consider higher-margin pharmacy benefit manager (PBM) companies instead.

By the Numbers: Drug Development Costs

| $78 million | The average cost of running Phase 1/2/3 clinical trials on an oncology (cancer) drug. |

| $985.3 million | The total cost of bringing a new drug to market after adding marketing and development costs, according to the NIH. |

| $119 million | The median amount of cash and short-term investments that biotech companies hold. Biotech firms typically carry enough money to run clinical trials but rely on larger pharma companies for marketing, production and distribution. |

| $9.8 million | The median revenue of a U.S. biotech firm, according to data from Thompson Reuters. Larger pharma companies typically buy up revenue-generating biotechs, leaving pre-revenue ones on the market. |

Interesting Reads: Of Penny Stocks and Moonshots

Quant-based Mark Hake turns his attention to seven penny stocks to buy. His list is as interesting as it is diverse.

Could Workhorse (NASDAQ:WKHS) make a comeback? Joanna Makris makes a strong case of how the company’s management can still turn the ship around.

When is a “recall” not a recall? When the Chinese government wants to send a message. Another piece by Joanna Makris this week takes a look at what that means for Tesla (NASDAQ:TSLA) bulls worldwide.

Eric Fry and InvestorPlace’s CEO Brian Hunt consider whether tech investors should worry about inflation. Hint? Don’t let fear stop you from doing the right thing.

Closing Thoughts: Who Wants to Be a Biotech Investor?

There are two types of people who invest in biotech companies.

The first is the thoughtful researcher. They’re the ones who understand how clinical trials work, know which pathways are the most promising, and can size the market of each potential new drug. They operate much like professional gamblers — wagering precise amounts based on the probability of each drug’s chances of success.

The second is the momentum trader. These investors focus on the price action that the first group creates and ignores the science behind the companies.

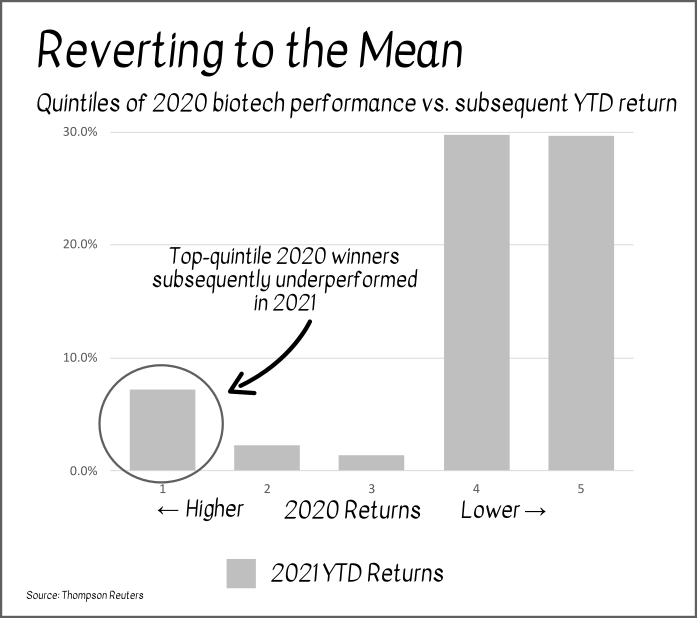

If you’ve ever wondered why the second group seems so rare, that’s because momentum traders don’t last long in biotech. The top-performing biotech stocks tend to reverse in price; Phase 1 trials only prove safety, not whether the drug works nor how profitable a drug will become.

Mindless Moonshot investing might be fun in assets such as cryptocurrency. But if you’re going to buy some biotech, make sure to bring your big due-diligence guns along.

FREE REPORT: 17 Reddit Penny Stocks to Buy Now

Thomas Yeung is an expert when it comes to finding fast-paced growth opportunities on Reddit. He recommended Dogecoin before it skyrocketed over 8,000%, Ripple before it flew up more than 480% and Cardano before it soared 460%. Now, in a new report, he’s naming 17 of his favorite Reddit penny stocks. Claim your FREE COPY here!

On the date of publication, Tom Yeung did not have (either directly or indirectly) any positions in the securities mentioned in this article.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing.