Beaten-down stocks can be the best friend of those with the patience to hold through ups and downs. Well-established companies that have products with staying power will rarely disappoint you over a multi-year investment period. Wall Street often takes things too far when a business faces bearish pressure. However, the opposite is also true. It is always better to pounce on the former opportunity – buying undervalued stocks is a more fruitful endeavor than shorting overvalued ones.

The good thing about buying undervalued stocks compared to shorting overvalued stocks is that time is on your side. As the broader market and economy grow, so will these well-established companies. As the old Wall Street adage goes, “The stock market is a device for transferring money from the impatient to the patient.”

Moreover, we had quite a dovish Jerome Powell, at least according to Dudley. The Federal Reserve Chairman’s stance seemed clear on there being no more rate hikes going forward. Even if inflation comes in hot, the Fed is likely to simply hold steady. He also indicated that the Fed would still cut rates even if wage growth remained high. All of this dovish monetary policy stance makes me optimistic about the following three undervalued stocks.

Intel (INTC)

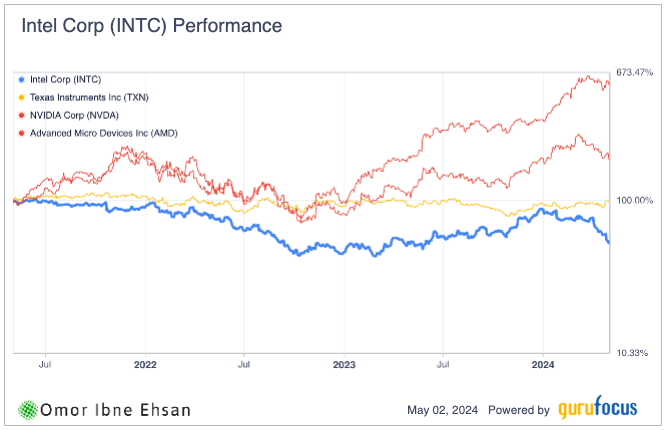

Intel (NASDAQ:INTC) had a very bad month. The stock is down 31% over this past month and is down 13% since just Thursday. The semiconductor industry, in general, hasn’t been keeping up very well. Momentum seems to have faded, and many big-name semiconductor stocks have come crashing down.

Click to Enlarge

Intel’s sustained turnaround has been entirely reversed in just one month after the release of its first-quarter earnings, which revealed revenue of $12.72 billion, an increase of 8.8% year-over-year, but still a 0.44% miss. Moreover, the company’s second-quarter revenue outlook fell short of estimates. A month before that, Wolfe Research analyst Chris Caso reiterated an “underperform” rating and a $31.00 price target for Intel. Susquehanna lowered its price target for Intel to $40 from $42. Citi also cut its price target for Intel, but opened a “positive catalyst watch.”

Despite all the bearishness, I think INTC stock is an excellent long-term play. As the old adage goes, “be greedy when others are fearful.” The business was declining badly just two years back, and now sales growth has turned solidly positive. Expectations were certainly higher than they should have been due to recent AI mania and the market rally. But even with the miss, you cannot argue that Intel is in worse shape than it was during the 2022 selloff. As such, prices coming back down to those levels seem like a bargain to me.

Lightspeed Commerce (LSPD)

Lightspeed Commerce (NYSE:LSPD) provides point-of-sale and e-commerce software to retail businesses. This stock has been one of the most bearish names in the market. Indeed, LSPD stock has been depressed since the company’s late-2021 selloff, and is up just 5% over the past year.

However, I have high hopes for Lightspeed Commerce. Not everyone would agree that it is one of the most undervalued stocks, but I believe taking a contrarian view is not a bad idea at all here, especially after the return of Dax Dasilva as CEO. The company recently announced cost reductions, a share repurchase program, and a reaffirmation of its focus on profitable growth. Lightspeed is now undergoing a shift of focus to its payment solutions.

Regardless, institutional investors are yet to be impressed, as LSPD stock has faced a slew of price target cuts. I personally remain bullish on this company, as the stock price has an established floor and lots of upside potential if management manages to outperform. Analysts expect earnings per share to rise from 16 cents to $1.14 from 2024 to 2028, along with revenue growing almost 300% in the next six years. Thus, I think paying the premium here is worth it.

StoneCo (STNE)

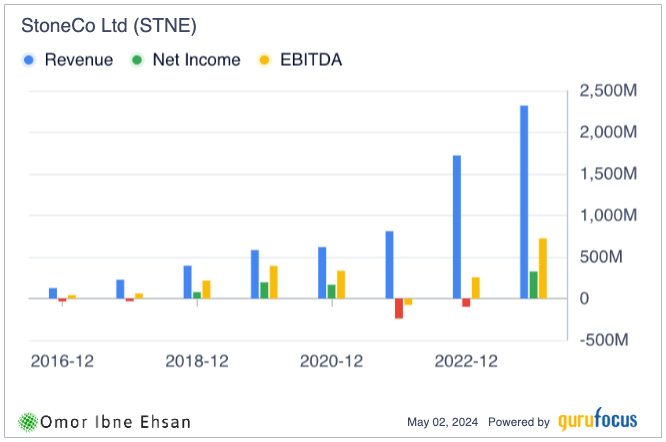

StoneCo (NASDAQ:STNE) is in almost the same boat as Lightspeed Commerce regarding stock price performance. STNE stock has been rangebound around $10 to $20 for the last two years, though it is up over 30% in the past year. I think this upside trend could continue as its financial technology and software solutions become more popular in Brazil.

Brazil was one of the least-penetrated regions in terms of online banking, fintech, and e-commerce just a few years back, but it has become one of the biggest markets for companies like StoneCo. We are now seeing significant growth, with StoneCo’s 3-year revenue growth rate at 51%, better than 93.4% of its software peers. Moreover, it has maintained a net margin of 14%. Margins have lagged sales growth, but I think this could be a catalyst that drives shares back up significantly once margins expand.

Click to Enlarge

You’re paying just over 11-times forward earnings for all the growth here, which makes this one of the most undervalued stocks in the fintech space. Goldman Sachs (NYSE:GS) upgraded StoneCo to “buy” from “neutral” and raised its price target to $21 from $12 in January, which has been correct thus far. I believe STNE stock changing hands at $35 or higher could be in the cards by next year, barring any significant downturn.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.