Judging which growth stocks are good long-term bets is trickier than you might expect. These fast-moving businesses can be hard to forecast, and changes in their broader industries could quickly lift up (or sink) these growth names in short order. However, there is one metric you need to keep in mind above all else: profitability. This is by far the most important factor, a lesson I’ve learned the hard way.

Investors should avoid scooping up growth stocks that are far from achieving profitability and don’t have the cash to fund their way through the losses. On the surface, these businesses may seem cheap, but once that cash inevitably runs out, you’re likely to see those shares being diluted to zero in the blink of an eye.

On the other hand, buying up businesses that are already profitable or are close to generating profits and have a long growth runway is a much better idea. You’ll have to pay a premium for these stocks, but it is more than worth it in the long-run as they’re unlikely to fail you. With that in mind, let’s look at two growth stocks to sell and one to buy right now.

Virgin Galactic (SPCE)

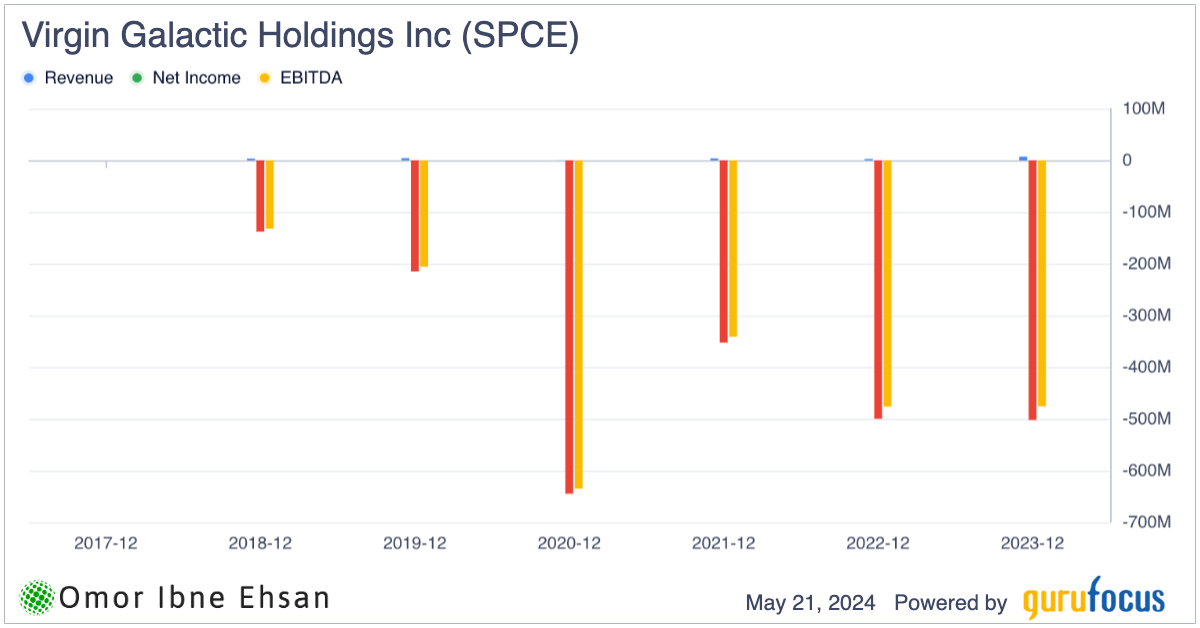

Virgin Galactic (NYSE:SPCE) is down 90.4% over the past four years for a reason. And I think that the reason is that the company is simply too ahead of its time. The company’s latest financial results clearly show the challenges of achieving its ambitious goals. Generating only $2 million in revenue this quarter while free cash flow declined further to -$126 million in Q1 is not a good look. Analysts expect this company to generate profits in 2028. It has $867 million in cash left, which won’t cover it for more than two years at this rate. Indeed, these losses do not look sustainable at all.

Click to Enlarge

Despite repeated delays during its design period, the projected timeline for the Delta spaceships seems optimistic. Even if Virgin is able to surmount the technical hurdles we’re likely to see over the next few years, the space giant will still be constrained by limited launch capacity compared to management’s lofty revenue projections. It remains to be seen how they will scale operations successfully to justify current levels of cash burn.

With cash reserves rapidly diminishing and no profitability in sight until well into the next decade, this is definitely one of the top growth stocks to sell in my books.

ChargePoint (CHPT)

ChargePoint (NYSE:CHPT) seems to have hit a growth ceiling, and big competition is likely to be seen ahead from Tesla (NASDAQ:TSLA) and other EV charging companies. This company has been swimming in the red for the past few quarters, and even if interest rate cuts come soon, their impact will take many more quarters to help ChargePoint out.

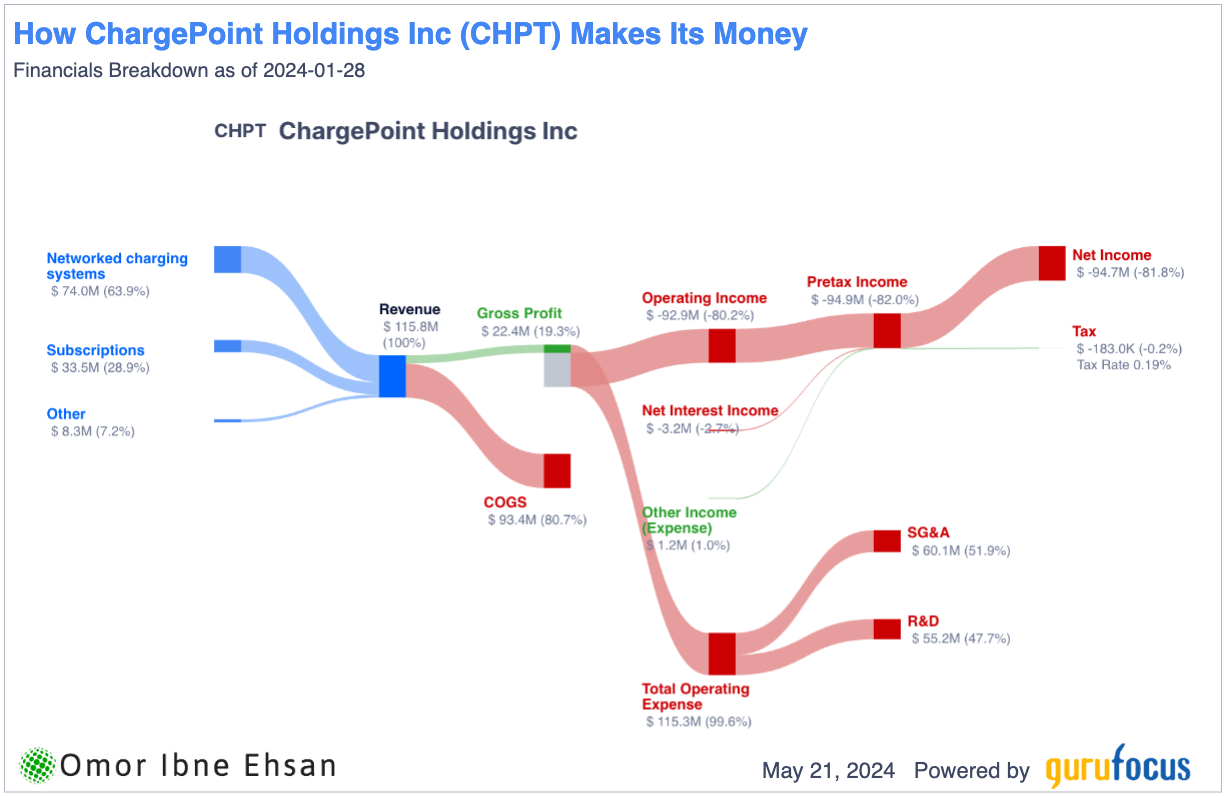

Indeed, the company’s Q1 report was obviously disappointing. Total revenue came in at $116 million for the period, down 24% and missing analysts’ projections. ChargePoint continues to fight an uphill battle, as more customers delay investments in electric vehicle charging stations and networks. Sales were especially soft in their commercial division that works with car dealerships and partners over in Europe.

However, this actually isn’t my biggest concern. As I said earlier, profitability matter the most. The company’s net profit margin actually declined by almost 59% to -81.8%.

Click to Enlarge

As a result, ChargePoint is forced to dilute existing shareholders continuously. Analysts see profits on the horizon (two years from now), but I doubt that’ll happen, considering the big misses.

It’s clear ChargePoint is trying to streamline costs, but downsizing can only do so much.

Hims & Hers Health (HIMS)

Hims & Hers Health (NYSE:HIMS) is an up-and-coming telehealth company. It has been a standout performer recently, and its stellar performance is too good to ignore. The company recently announced plans to introduce $199 weight loss drugs. Thus, it should be no surprise that shares have gone vertical as of the time of writing.

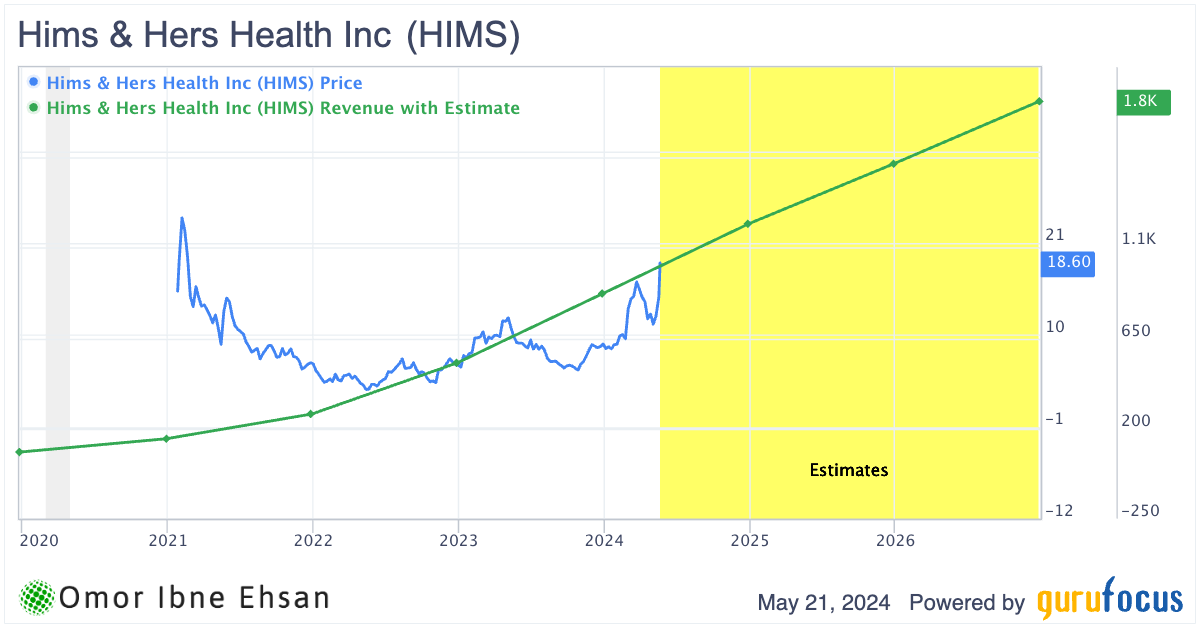

Importantly, Him & Hers reported very encouraging results in Q1. Revenue soared an impressive 46% to $278 million as the company’s personalized health offerings resonated strongly with consumers, attracting a record 172,000 new subscribers.

Click to Enlarge

More than 35% of their 1.7 million subscribers are now benefiting from a personalized treatment plan, which typically leads to higher customer retention. Additionally, Him & Hers reported 5 cents of earnings per share, which beat estimates by 4 cents!

If Hims & Hers continues effectively implementing their personalization approach, I believe the company is well-equipped for sustained growth in the coming years. Yes, HIMS stock has rallied a lot recently. But those weight loss drugs are real catalysts to consider. You’re paying just 2.6-times forward sales for a company with lots of room for margins to grow.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.