Stocks under $20 usually provide a very good balance of upside potential and safety. I believe it is worth looking into many stocks in this range, as many have been battered and are about to make a turnaround. That’s compared to many similar stocks in lower price ranges which may be up-and-coming startups that are just beginning to get big.

I believe once interest rate cuts start and the economy enters a new cycle in the coming quarters, investors could start taking a deeper look into the market. The best stocks under $20 would be among the first to rise. That’s I think especially true for the following three, if they can maintain their current trajectory.

Paysign (PAYS)

Paysign (NASDAQ:PAYS) is a leading fintech company that provides payment solutions for the healthcare and pharmaceutical industries. The stock has been on a tear lately, surging 66% over the past year despite the general malaise in the fintech sector. I believe this momentum can be sustained given Paysign’s growth metrics, particularly in its patient affordability business.

In Q1 2024, Paysign’s revenue rose 30% year-over-year to $13.2 million, while adjusted EBITDA skyrocketed 135% to $1.7 million. The patient affordability segment was the star of the show, with revenue exploding 305% to $2.4 million from just $590,000 a year ago. This division accounted for a whopping 59% of Paysign’s total revenue growth.

Management noted that they added a net 10 new patient affordability programs in Q1, ending with 53 active programs. They’ve also expanded into retail drug programs, which typically have higher claim volumes. With the sales pipeline remaining robust and productive meetings at the recent Asembia Summit, I expect the pharma segment’s growth to accelerate further.

QuickLogic (QUIK)

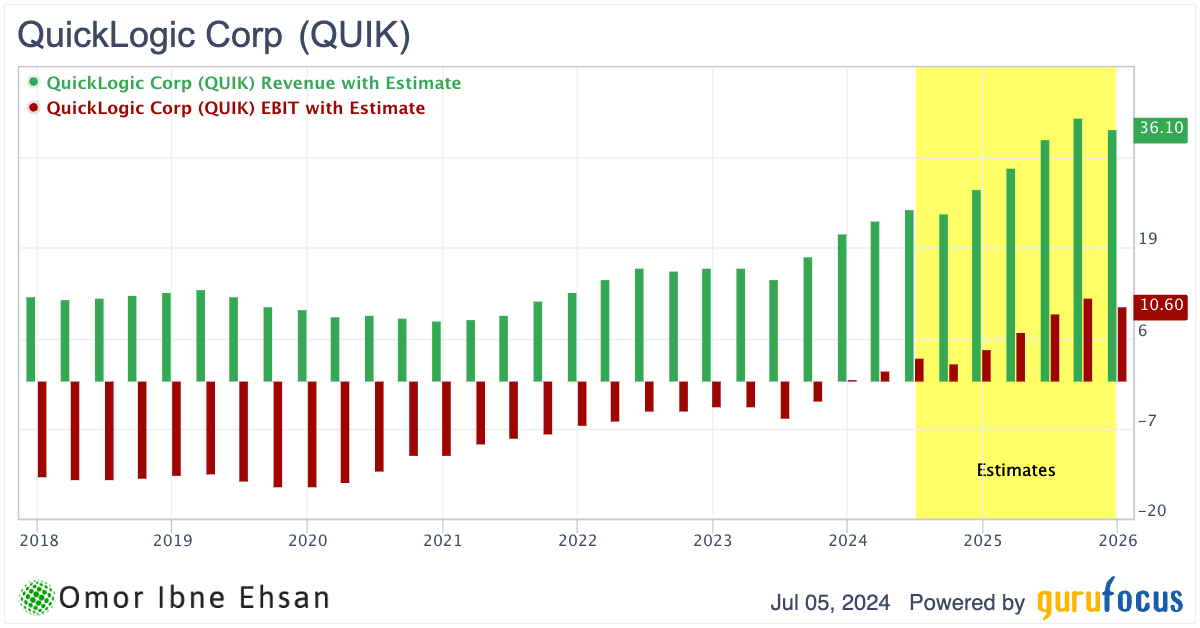

QuickLogic (NASDAQ:QUIK) develops low-power customizable semiconductor and software solutions. Notably, QUICK stock has retreated 45% from this year’s peak. However, I believe QuickLogic has significant upside potential. The company operates in many of today’s hottest sectors.

In Q1, revenue grew an impressive 45% year-over-year to $6.01 million. These strong results were driven by a nearly 60% surge in new product sales, primarily from eFPGA IP contracts. However, the company is projecting a sequential decrease in Q2 revenue to around $4.5 million. This lower guidance is due to changes in how IP contract revenue is recognized. That said, this shift should push more revenue into the second half of 2024. The company is expected to see operating profits rise higher over time as well.

Click to Enlarge

Despite the stock’s recent dip, there’s a lot to look forward to. QuickLogic’s record $179 million sales funnel and pending significant eFPGA contract proposals give me confidence in the company’s ability to deliver 30% annual revenue growth going forward. The company has also signed a $72 million radiation-hardened FPGA government contract. And impressively, this contract includes the likes of Honeywell Aerospace and SkyWater Technologies as partners. Plus, QuickLogic’s subsidiary SensiML makes AI/ML software that could be in high demand. Add it all up, and this is a cheap stock worth buying right now.

EZCORP (EZPW)

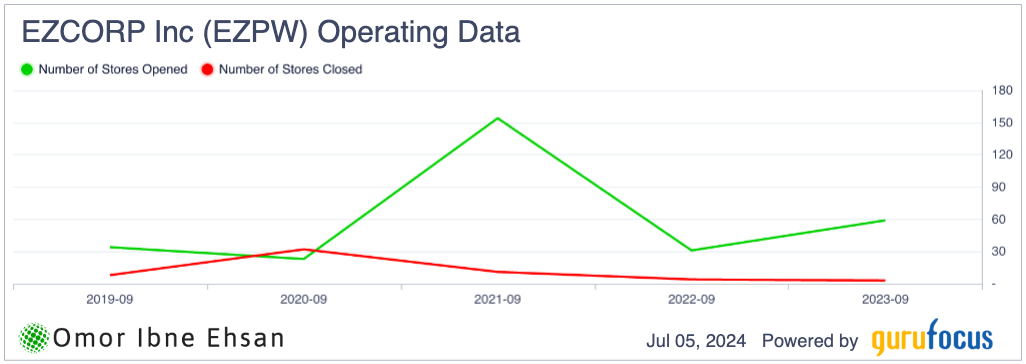

EZCORP (NASDAQ:EZPW) operates pawn shops in the U.S. and Latin America. I believe the stock is a compelling buy right now. Currently, EZPW stock trades at just $10 per share, with tremendous upside potential.

In Q2, EZCORP delivered record-setting results, with revenue up 10.5% to $285.6 million and outstanding pawn loans surging 13% to $232 million. The challenging macroeconomic backdrop is actually benefiting the business, as cash-strapped consumers increasingly turn to pawn loans for short-term financing needs.

Moreover, EZCORP opened nine new stores in Latin America, while acquiring six locations in the U.S. With $229 million of cash on its balance sheet, EZCORP has ample dry powder to open even more stores.

Click to Enlarge

While EZCORP has historically been a volatile name, I’m encouraged by the consistent improvement in key metrics like merchandise sales (+6%), gross profit (+10%), and adjusted EBITDA (+7%).

Plus, investments in adjacent fintech platforms like Rich Data Corporation could lead to more growth. Canaccord Genuity recently assigned an $18 price target on EZPW stock, so the risk/reward setup looks attractive at current levels. EZCORP is proving pawn shops are still relevant. As such, I think EZPW stock is one of the best stocks under $20 to buy right now.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.