As of July, over 2,600 stocks on major U.S. indices have a share price of $10 or less. While many of these are risky penny stocks, there are some real diamonds in the rough waiting to be discovered. Low-priced stocks are often ignored, especially those in the $5 to $10 range, as they don’t count as a penny stock and get skipped by screeners, but they can still deliver huge returns.

Of course, the low-priced landscape is littered with land mines. Stocks often trade under $10 because the underlying businesses are struggling. Separating the wheat from the chaff requires diligent research.

The key is to zero in on fundamentally sound, undervalued companies relative to their long-term prospects. Here are seven that I think fit that bill:

Bumble (BMBL)

Bumble (NASDAQ:BMBL) operates a popular online dating platform that empowers women to make the first move. The company’s stock has taken a beating in the past year, plummeting over 50% to trade around $9.30 as investors fret about the competitive landscape and path to profitability.

However, I believe the market is being too pessimistic about Bumble and overlooking the company’s strong fundamentals. Despite the stock price decline, Bumble continues to post impressive revenue growth, with analysts projecting high-single-digit increases. The app is also rapidly expanding its user base by double digits and gaining market share from rivals.

While not yet solidly profitable, analysts expect Bumble to return to the black for the full year of 2024 and nearly double earnings per share over the next four years. Valued with a forward price-to-earnings ratio of just 11x, the stock looks quite cheap, given the future growth.

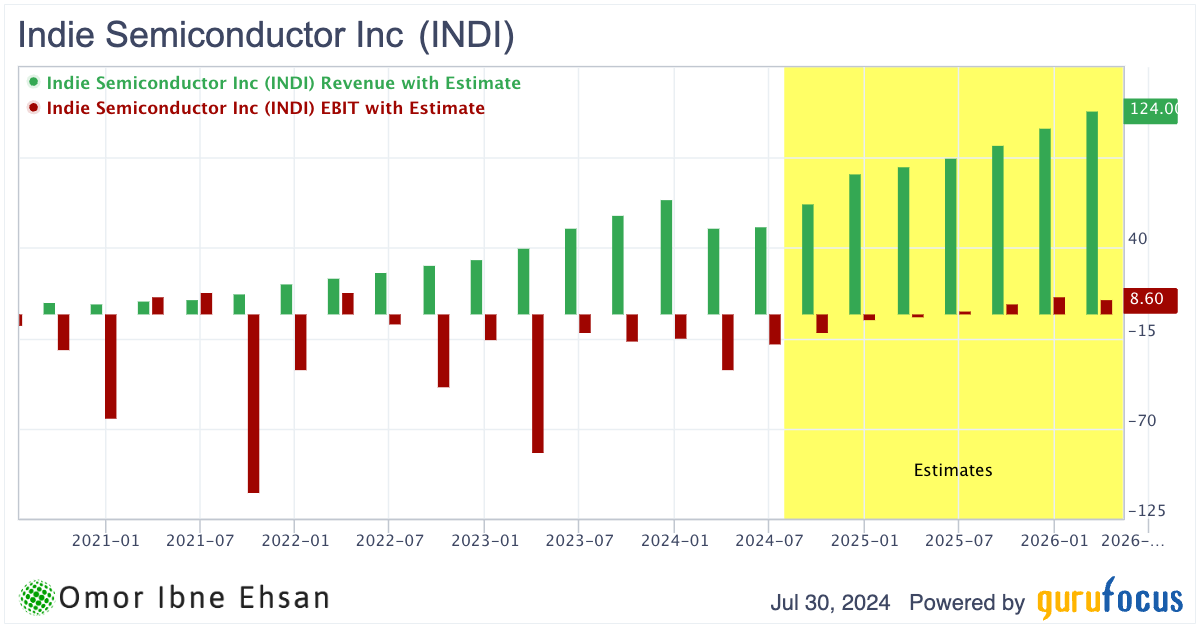

Indie Semiconductor (INDI)

Indie Semiconductor (NASDAQ:INDI) is a pure-play automotive semiconductor company focused on developing cutting-edge solutions for advanced driver assistance systems, connected cars, user experience, and electrification applications. Despite the recent struggles of many EV-related startups, Indie weathered the storm relatively well, with its stock down only 35% over the past year and a mere 4% in the last six months.

I believe Indie Semiconductor is poised for significant growth and profitability. Analysts are bullish, with a consensus “strong buy” rating and an average price target of $10.80, representing a 76% upside from current levels. Deutsche Bank analyst Ross Seymore reiterated a “buy” rating in May with a $9 target (lowered from $10).

In Q1 2024, Indie reported 29% year-over-year revenue growth to $52.4 million, albeit slightly below guidance. With profitability expected in 2025 and revenue projected to nearly double over the next two years, I think Indie is positioned to capitalize on the automotive recovery once rates start getting cut. The transition to profitability should also cause the stock to rise.

Click to Enlarge

Of course, risks remain in this challenging macro environment for the auto industry. Indie will need to execute flawlessly to achieve its ambitious targets. But trading at $6 with such robust growth prospects, I believe the stock is undervalued and has the potential to double. Keep this one on your radar.

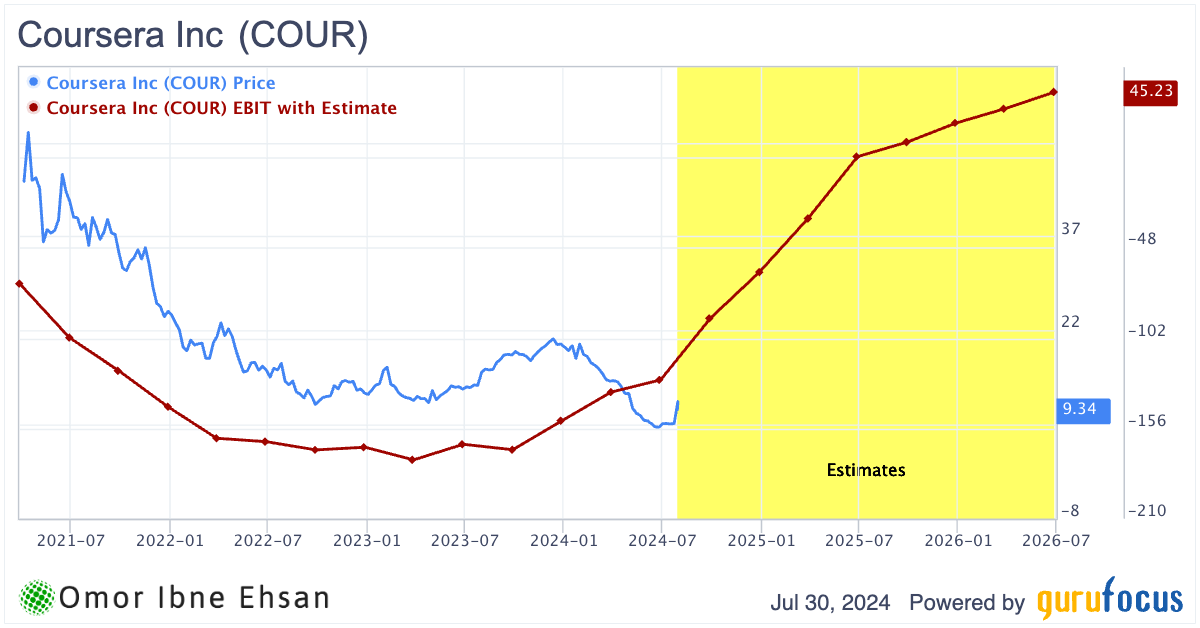

Coursera (COUR)

Coursera (NYSE:COUR) provides online courses and degrees from top universities and companies. The ed-tech company has been on a wild ride in the stock market lately, with shares soaring after a strong Q2 earnings report before diving nearly 13% the next trading day on profit-taking and a bearish analyst note.

Despite the volatility, I think Coursera is worth a closer look at under $10 per share. The rise of online learning plays right into their hands as people rush to learn new skills. Revenue rose 11% year-over-year to $170.3 million, beating estimates. And the company is finally profitable, with analysts expecting earnings to skyrocket over 2,000% this year.

However, not everyone on Wall Street is bullish. Goldman Sachs analyst Eric Sheridan just cut his price target on Coursera to $9, reiterating his “sell” rating. On the other hand, most analysts still have “strong buy” ratings on the stock, with an average price target of $17.

It’s a bit over $9 right now. At around $9 per share, you’re paying just 23x expected 2026 earnings for this beaten-down growth stock.

I don’t care about the near-term volatility. I see this as a long-term turnaround as the company turns profitable.

Click to Enlarge

If Coursera can maintain its momentum and prove the bears wrong, shares could easily double in the coming years.

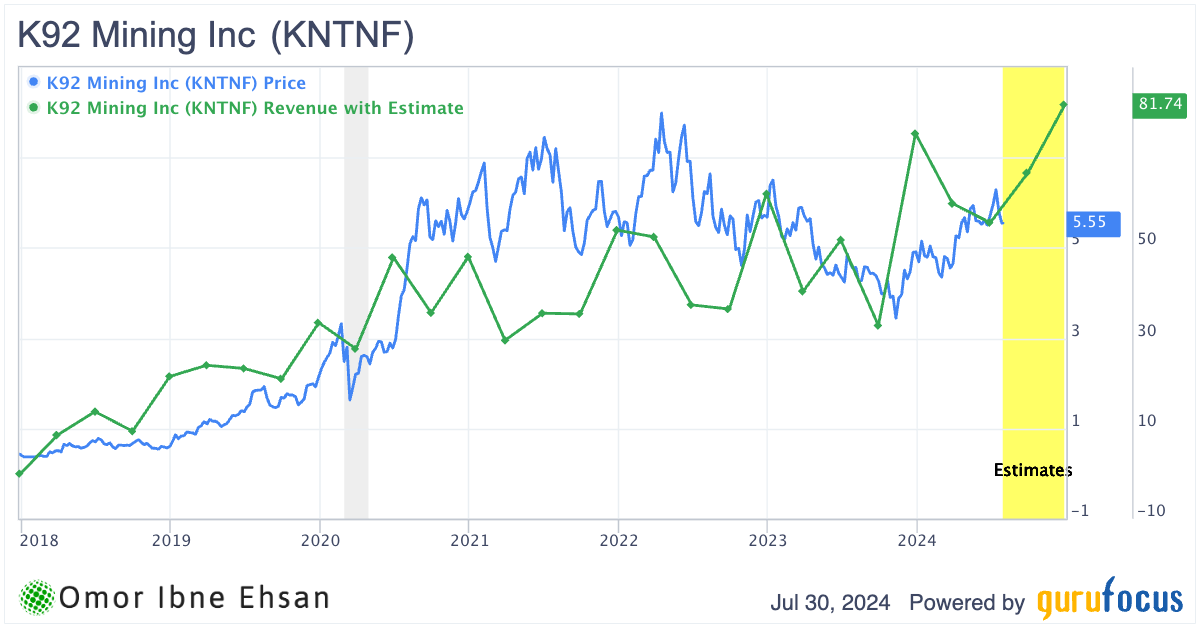

K92 Mining (KNTNF)

K92 Mining (OTCMKTS:KNTNF) produces gold, copper, and silver at the Kainantu Gold Mine in Papua New Guinea. The company delivered strong operational results, with record quarterly production of 39,101 gold equivalent ounces in Q4 2023 and exceeding its annual production guidance.

I’m pretty bullish on K92 Mining as gold prices continue to soar. Analysts expect the company’s sales to surge from $250 million this year to around $880 million in 2027. That impressive growth could easily cause the stock to double, especially if gold prices remain stable or keep climbing. The stock has historically followed sales metrics, and I expect the same going forward.

Click to Enlarge

Analysts currently have a “strong buy” rating on K92 Mining with a consensus upside potential of nearly 50%.

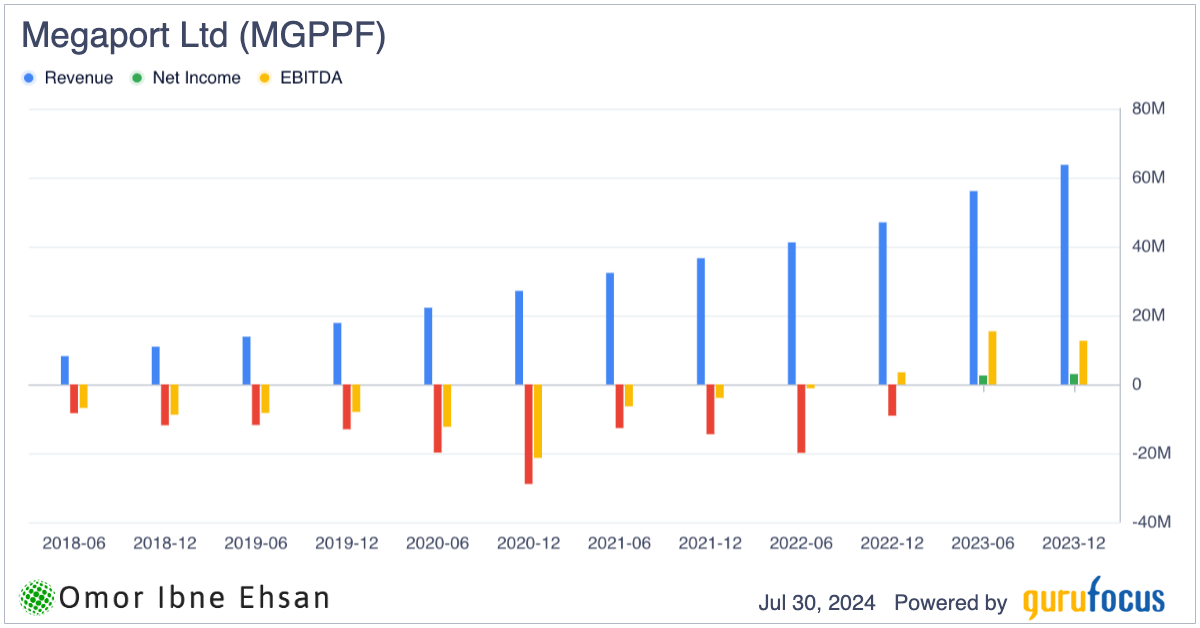

Megaport (MGPPF)

Megaport (OTCMKTS:MGPPF) provides software-defined networking solutions that enable fast, flexible, and secure connectivity to cloud service providers. The company has been riding the wave of the cloud boom, delivering strong financial results and attracting positive analyst sentiment.

In its latest quarterly update, Megaport reported a 30% year-over-year increase in revenue to 49.5 million AUD and an impressive 92% surge in EBITDA to 14 million AUD. Annual recurring revenue also grew to 199 million AUD. It’s a profitable growth stock now.

Click to Enlarge

However, the stock took a hit recently despite the company upgrading its full-year EBITDA guidance, as the market seemed to have priced in a stronger performance. Nevertheless, Megaport is positioned to benefit from the ongoing cloud adoption trend and deliver solid returns for investors. The stock is still up by nearly 40% over the past year.

SmartRent (SMRT)

SmartRent (NYSE:SMRT) provides smart home automation solutions for rental properties. The company has been expanding its offerings and customer base but is still operating at a loss.

I believe SmartRent could turn things around if the real estate market stays robust. Demand for rentals should remain high, especially with smaller households and immigration trends. SmartRent’s products could become must-haves for landlords looking to attract tenants and streamline operations.

Analysts seem cautiously optimistic, with a consensus price target of $3.80, implying almost 60% upside potential. Analysts at BTIG recently maintained a “buy” rating with a $4 target (cut by 30 cents). However, profitability remains elusive, as SmartRent posted a $35 million loss last year. The path to breakeven is narrow.

Still, there are bright spots. Zero debt means less risk for investors. And revenue could double within four years. If management executes well and demand stays strong, the stock has a decent shot at doubling.

Eventbrite (EB)

Eventbrite (NYSE:EB) operates a global self-service ticketing platform for live events. The company’s stock has struggled over the past year, down nearly 54% and hovering just above $5 since March 2024. However, I believe Eventbrite could turn things around if it grows well and achieves solid profitability. It’s more “recovery” than “growth” right now.

Analysts think Eventbrite could become profitable next year and grow its EPS rapidly in the coming years. If those projections prove accurate, the stock will trade at just 5x 2028 estimated earnings. Of course, long-term estimates are prone to significant error.

Eventbrite recently began charging event organizers a new fee to boost its lackluster profitability. This risky move may drive away some customers, evidenced by a shrinking paid organizer count. While this strategy could pressure the stock soon, I’m optimistic about the company’s long-term prospects.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.