Even with the stock market’s impressive gains, there’s no shortage of undervalued stocks if you know where to look. The recent correction has just scratched the surface of the tech sector. Those high-flyers have further to fall before being considered undervalued.

However, if you’re willing to dig deeper, you’ll find plenty of overlooked names that have languished at undervalued levels for months or even years. I think it’s worth scooping up some of these hidden gems before the economic tide turns. Many of these companies have the resilience and cash flow potential to outperform once interest rates are cut and their financials outpace their stock prices.

Granted, it might take longer than a year for the stars to align perfectly for these undervalued plays. But I’m convinced they can beat the broader market over the next couple of years as they recover.

Norwegian Cruise Line (NCLH)

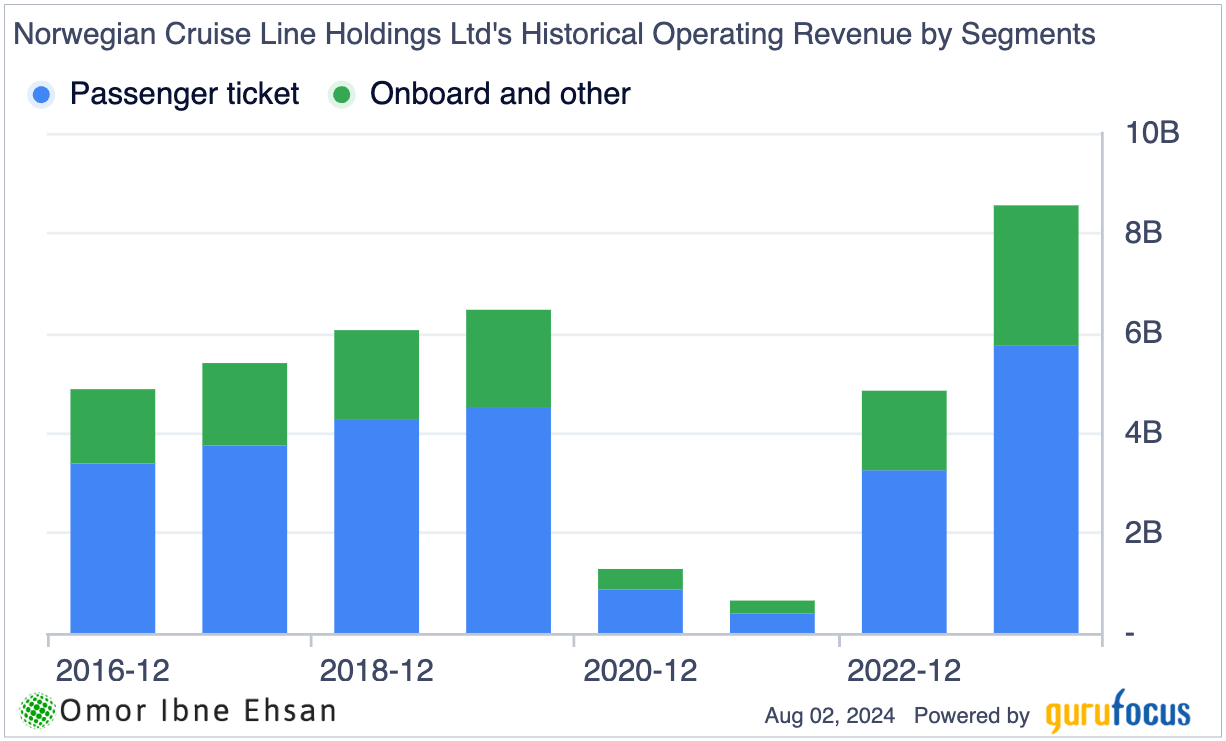

Norwegian Cruise Line (NYSE:NCLH) operates a fleet of cruise ships that sail to destinations around the world. The company has been navigating choppy waters lately, as it had to take on significant debt during the pandemic to stay afloat and was then hit with spiking interest rates that crushed profitability and forced cutbacks in growth investments like marketing spend.

Despite these challenges, I believe Norwegian Cruise Line stock is undervalued and poised for a major rebound in the next 12 months. The company just reported strong Q2 2024 results, with revenue up 8% to $2.4 billion and adjusted earnings per share of 40 cents, beating estimates by 23%. Both its segments have recovered in terms of revenue, and profitability should follow suit once debt servicing costs decline.

Click to Enlarge

Analysts are getting more bullish, too, with Macquarie recently raising their price target to $24. The consensus rating is still a “Hold,” but I think that will change as interest rates come down and profitability improves.

Norwegian’s debt load has doubled since 2019 to $13.7 billion, but even a small interest rate cut would provide a big boost to the bottom line. With the stock still 69% below pre-pandemic levels, I see huge upside potential as the cruise industry recovers. If you’re willing to ride out some near-term volatility, Norwegian Cruise Line looks like a very attractive risk reward at these depressed levels. The company is steadily improving operationally, and I expect the stock to start sailing much higher in the coming quarters.

StoneCo (STNE)

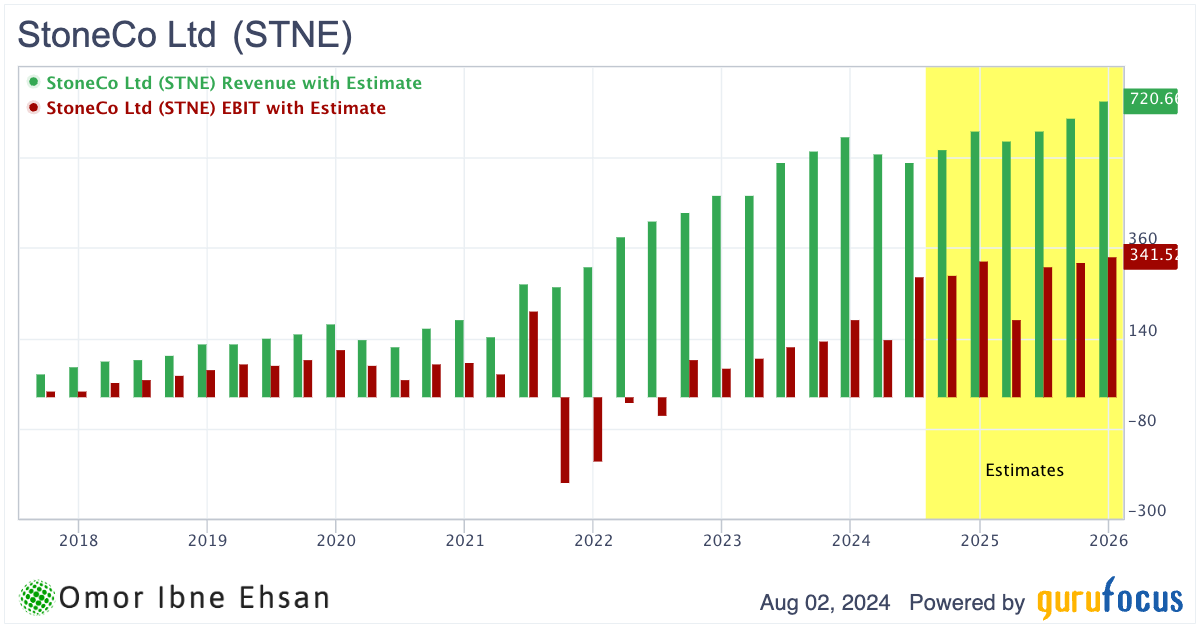

StoneCo (NASDAQ:STNE) provides financial technology solutions to merchants in Brazil. The company has been navigating a challenging environment, with its stock price trading sideways for the past two and a half years following an initial crash from the post-COVID boom in 2021. However, I believe StoneCo is well-positioned to capture a significant share of Brazil’s rapidly growing fintech market, in which it already holds 11.3%.

Brazil has been ahead of the curve in its inflation and rate cut cycle, having started raising rates earlier and subsequently cutting them substantially as inflation subsided. In my opinion, StoneCo stands to benefit greatly from this trend in the long run, even though STNE stock has yet to reflect the company’s improving fundamentals.

According to recent analyst estimates, StoneCo’s EPS is projected to grow from $1.20 in 2024 to $2.60 by 2027. Revenue and operating profits are both expected to recover and keep growing, and I think the stock should, too.

Click to Enlarge

As UBS recently upgraded the stock, I believe the time for a breakout is near, and the stock is poised to catch up with the company’s solid financial performance.

Teleperformance (TLPFY)

Teleperformance (OTCMKTS:TLPFY) provides customer experience management and business services solutions worldwide. The company has been facing challenges recently, with its stock price still down 72% from its 2021 peak following rising interest rates.

TLPFY used to be one of the most consistent stocks, often outperforming the broader market. However, higher rates have hit the company hard. I believe a turnaround may be underway, though, as global rates start to ease. With Teleperformance’s solid fundamentals, this could be an exceptional long-term buying opportunity, sweetened by a 3.24% dividend yield.

In H1 2024, Teleperformance reported accelerating growth and increased free cash flow (“H1 2024 revenue: €5,076 million, up +28.2% as reported and +1.7% pro forma | Q2 2024 revenue: €2,534 million, up +29.7% as reported and +2.4% pro forma”).

The company is also seeing the first effects of cost synergies from its Majorel acquisition. Some see Teleperformance as well-positioned with a resilient, diversified client base. Others are more cautious, given the uncertain macro environment. Regardless, I believe Teleperformance can weather this storm and is quite undervalued.

Block (SQ)

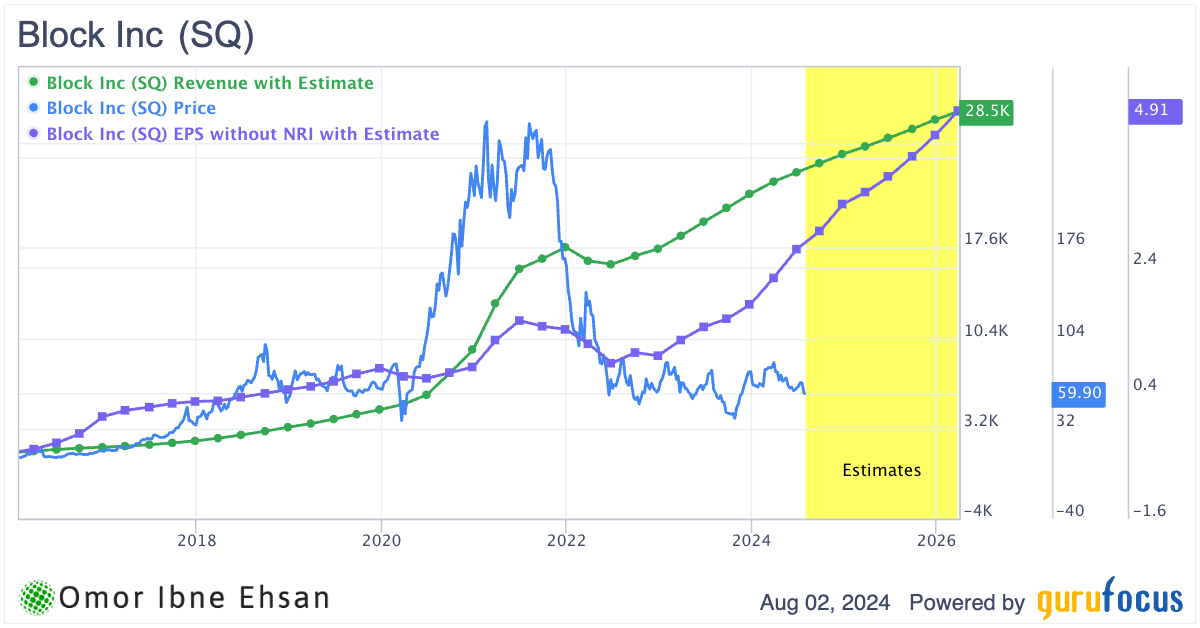

Block (NYSE:SQ) provides mobile payment and financial services through its Square and Cash App platforms. The company has faced challenges recently, with high interest rates causing banks and merchants to be more cautious and transaction volumes slowing down. SQ stock has been stuck in a rut along with many other fintech stocks, as the post-pandemic rush of users has subsided and account growth figures seem stagnant.

However, I believe most fintech stocks, including Block, are poised for a comeback as interest rates start to decline and we enter a new economic cycle. Block’s core financials have been impressive, with the company reporting $6.16 billion in revenue and EPS of 93 cents in Q2 2024, beating analysts’ estimates on the bottom line. The company has turned into a profitable growth stock and should be trading at a much higher valuation.

That said, Block is not without its challenges. The company is currently under federal investigation for potential breaches in know-your-customer and anti-money laundering rules.

Nevertheless, the majority of Wall Street analysts maintain a “Moderate Buy” rating on SQ stock, with an average price target of $88.9, representing a 48.4% upside. If Wall Street paid even half the pre-COVID earnings premium, the stock would trade at $150 today.

Click to Enlarge

As the gap between the stock’s price and the company’s strong financials continues to widen, I believe a breakout is inevitable. While it may take longer than 12 months for the stock to surge 500%, I think patient investors will be rewarded in the long run.

Snap Inc (SNAP)

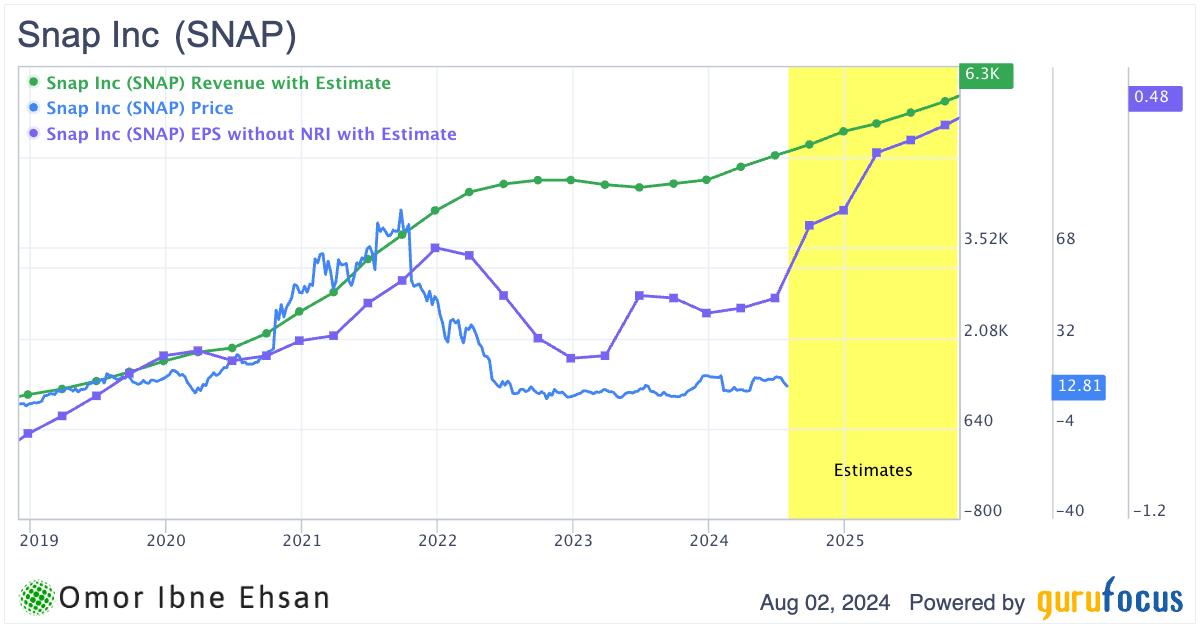

Snap (NASDAQ:SNAP) stock has been one of the weakest social media stocks over the past few years, and it has continued to disappoint investors like myself. Despite my frustrations, I still believe Snap could be a good long-term holding if they can turn things around.

After Snap’s weak Q2 guidance, the stock has slumped to around $10, which looks cheap considering the company is still delivering double-digit revenue growth. However, Snap urgently needs to improve its average revenue per user to stage a comeback like Meta (NASDAQ:META) did. It missed in the near term, but the long-term looks very promising. I can make the same argument about SNAP like I did with SQ. Growth hasn’t slowed by that much and it can still trade near pre-COVID multiples if management doesn’t make a fool of themselves going forward.

Click to Enlarge

The recent earnings show it will take longer than hoped, but potential catalysts like a TikTok ban in the U.S. could reignite interest in Snapchat. If Snap can find ways to better monetize its large, young user base, the stock has huge upside potential. But until they prove they can execute, you should still stay cautious.

Methode Electronics (MEI)

Methode Electronics (NYSE:MEI) has also been a big loser in the stock market for the past year and a half. It has lost nearly 77% of its value since the start of 2023, but I think it can turn things around once rates come down and the automotive industry makes a comeback. Analysts seem mixed about the stock. Jefferies recently initiated MEI with “Hold.” The decline has pulled the stock back down to more historical lows, and if things get better, it could rally back up like it did in 2012.

Recent news has been mixed. Methode reported a net loss in Q4 2024 on lower sales, but it did generate positive free cash flow and reduced its net debt. The company also won over $140 million in new program awards in the quarter, mainly in EV applications. If you’re willing to bet on an automotive rebound, MEI could be an undervalued opportunity. Analysts expect profits and positive sales growth next year.

Forward Air (FWRD)

Forward Air (NASDAQ:FWRD) provides expedited ground transportation services to the air freight and expedited LTL market in the United States and Canada. The company has hit some turbulence lately, with its stock losing nearly 80% of its value over the past year amid integration challenges with its acquisition of Omni Logistics and a sluggish demand environment.

It wasn’t always this rough for Forward Air, though. The company used to be one of the most consistent and stable performers in the transportation sector until the ripple effects of the pandemic sent shares plummeting. While the stock has bounced off the bottom a bit, it’s still struggling, down another 6% recently with the broader market selloff.

However, I believe Forward Air could be a solid long-term bet for patient investors willing to ride out the current storm. Activist investor Irenic Capital Management seems to agree, recently amassing a 5% stake and pushing the company to improve performance or consider a sale. The Wall Street Journal reported that Irenic believes several private equity firms would be interested in acquiring Forward Air at a substantial premium.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.