Tom Yeung here with your Sunday Digest.

There’s a saying on Wall Street that the best time to buy is when there’s blood in the streets.

Sounds easy, right?

After all, that’s how investors like Warren Buffett made their billions. For instance, he bought…

- Wells Fargo & Co. (WFC) during the 1989-’90 savings and loan crisis…

- Goldman Sachs Group Inc. (GS) and Bank of America Corp. (BAC) in the depths of the 2008 financial crisis…

- And Dominion Energy Inc. (D) during the COVID-19 pandemic.

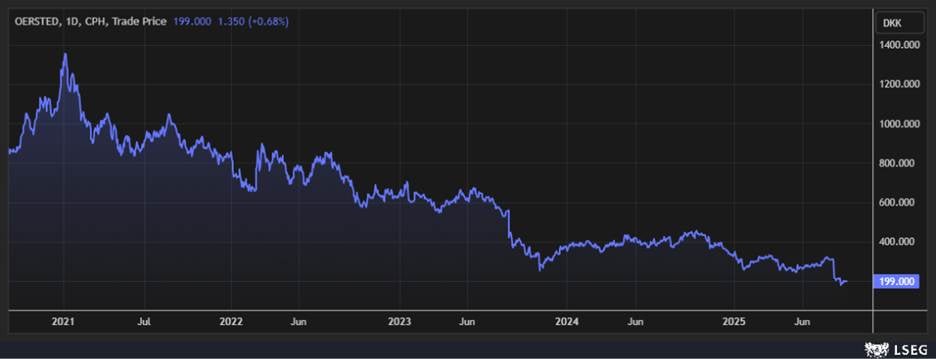

But then, what if you saw a stock graph that looks like this?

Because that’s what “blood in the streets” looks like at the bottom… an ugly combination of falling share prices, several dead cat bounces, and then even further drops.

In fact, the graph above shows shares of Oersted A/S (DNNGY), an offshore wind company that recently saw the Trump administration halt its $1.5 billion megaproject off Rhode Island. The Danish company’s stock has fallen almost 90% since its 2021 peak, and it could drop further as the U.S. president continues his war on wind power.

That’s the trouble with buying companies during panics. Bad news typically brings more bad news, so falling stocks tend to keep dropping. After all, a firm that’s lost 90% of its value is simply one that’s gone down 80%… and then fallen another 50%.

Yet, many of the top investment gurus seem to have a second sense of when markets and individual stocks are ready to rebound. They’re the ones standing on the sidelines, patiently waiting for the right moment to pounce.

In fact, that’s precisely what InvestorPlace Senior Analyst Eric Fry has been doing for the past three decades.

Since 1992, he’s been picking companies that have gone on to produce 10X gains, like:

And each of these followed a similar pattern. Shares would first plummet on factors beyond the company’s control. And right as things seemed most dire, Eric would jump in and invest for a 1,000% return.

Now, Eric has refined this “second sense” – his “mental” system – into a quantitative playbook. This new computerized system, Apogee, incorporates the factors behind his 41 investments that returned 1,000% or more. By doing so, he’s turning decades of intuition and knowledge into a repeatable process.

The system, of course, isn’t always flashing “Buy.” It’s not every day that a potential 1,000% winner walks through the door. Besides, it’s always better to wait for a fat pitch than swing wildly at whatever comes down the lane.

But now, Apogee is flagging not one… but three different stocks to buy. And Eric will reveal all three of those stocks – including their names and tickers – in during a free broadcast at 10 a.m. Eastern on Wednesday, September 10. In this presentation, he will go into detail about the Apogee system and reveal its first three “official” recommendations.

These are all firms he believes can rise 1,000% or more.

Click here for details and to get your name on the guest list for Eric’s full reveal on Wednesday.

Until then, I’d like to cover one of the key elements to his system – something he calls “down a lot, up a little.” When combined with other factors, this powerful signal can help investors buy when there’s blood in the streets while not getting hurt in the process.

And the best way to do this is with two illustrations…

Down a Lot… Up a Little

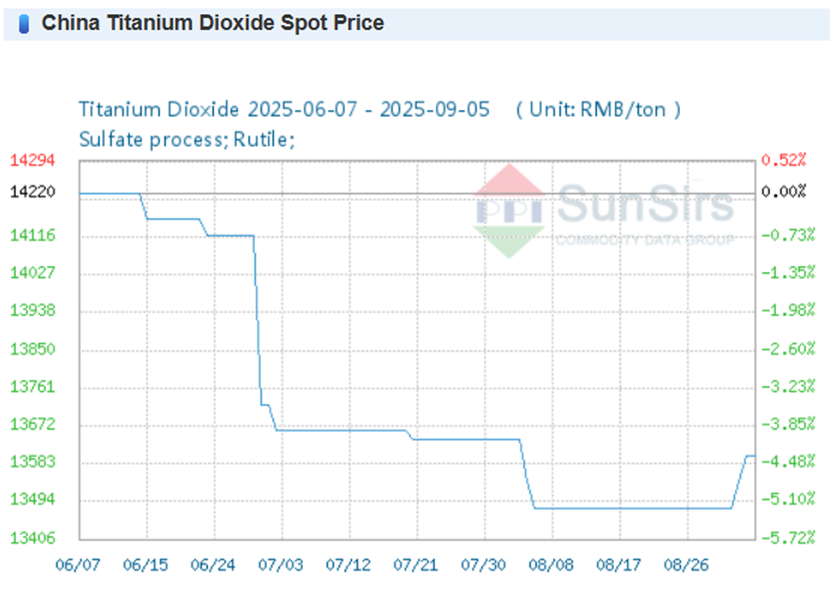

In August, I recommended Tronox Holdings PLC (TROX), one of America’s top makers of titanium dioxide (TiO2), the whitening compound found in paints, toothpastes, and more. Shares had fallen 86% since 2021 on weakening TiO2 prices, and the company was valued as if the market would never recover.

This is the “down a lot” part of Eric and Apogee’s 10 investment criteria. A company must have fallen far from its peak before its shares look attractive. After all, it’s easier for a cheap company to rise 1,000% than an expensive one to do the same.

Since then, Tronox has mounted a modest recovery. Shares have risen 16% since mid-August thanks to rising commodity prices, improving sentiment, and several bullish economic reports. Over the past weeks, prices of TiO2 in China have edged higher while those elsewhere have stopped falling.

[source]

This is the “up a little” sign that signals a turnaround could be underway… the green shoots that chase away short sellers and algorithmic traders.

There’s good reason to expect more upside from here.

First, American manufacturing is in better shape than most seem to realize. The S&P Manufacturing Purchasing Managers’ Index (PMI) rose to 53.0 in August, its strongest improvement since May 2022. (Any figure above 50.0 signals an expansion.) PMI in the European Union and China also sits above 50.0. These are highly bullish signs for Tronox, because TiO2 prices are determined by industrial demand.

Second, Tronox’s stock is cheap compared to its historical average. Shares trade for just 0.4X book value – below the 1.4X seen in more typical times. This gives TROX an unusual amount of upside from re-rating alone. (This is where multiples re-expand to meet their historic averages.)

Finally, Tronox remains the same well-run firm it was in 2021, when shares traded above $25. Selling costs have not budged, and the firm continues to reinvest in its highly productive mines worldwide.

And so, shares of this promising firm have 400% to 600% upside, even after a recent uptick. I’m reemphasizing TROX again this week as shares begin their “up a little” climb.

Stored Energy

Another company that’s been hammered by bad news is Fluence Energy Inc. (FLNC), a clean-energy firm that’s expecting to see revenues decline 3% this year. The firm specializes in building battery-powered energy storage for American utility companies, and uncertainty surrounding import tariffs has sent a chill through the industry. It’s hard to sell projects when it’s unclear whether imported batteries will have a 25% import tax or 114% one.

In addition, Fluence has suffered delays in ramping up its U.S. manufacturing facilities. By April 2025, shares had fallen under $4, from a previous high of $40.

Investors should sense an opportunity. Since the depths of the “Liberation Day” selloff, Fluence’s shares have rebounded 80% as growth comes back into the cards. Analysts expect fiscal 2026 revenue to surge 22%, and 19% in 2027. Meanwhile, net income is expected to flip back positive next year as Fluence’s American manufacturing facilities come online.

One key growth area comes from abroad. Fluence recently signed two contracts worth $700 million in Australia, which have helped bring its backlog to roughly $6 billion – enough to sustain 24 months of revenue. To international buyers, it matters little what American tariff rates are.

The other is from American utilities themselves. Many power companies are now returning to the market as the Trump administration clarifies import tariffs. As Fluence CEO Julian Nebreda noted it in recent earnings call remarks, all contracts that were halted due to tariffs have been reactivated. AI-focused data centers have high and variable energy needs, and lithium-ion batteries are often the only practical solution.

Here’s from Nebreda during his official third-quarter earnings call remarks:

These workloads are not only energy intensive. They are also highly variable. Training large AI models or processing inference tasks can lead to solid spikes in power consumption, placing immense strains on the grid and creating localized reliability challenges.

This is where battery energy storage can play a critical and unique role that cannot be filled by conventional sources of generation or renewables. [It] can act as a buffer, absorbing rapid surges in power and releasing it during high-demand intervals, effectively leveling out the fluctuations that come with AI-driven compute cycles.

In addition, battery prices have now fallen far enough that they are competitive with gas turbines. According to data from BloombergNEF, power costs from battery storage systems fell 40% to $165/kilowatt-hour in 2024. It’s now slightly below the roughly $169/kWh average cost of gas peaker plants.

That’s turning Fluence into a potential 500% to 600% winner. Battery power demands will only go up, not down, and Fluence has built out the production capacity and distribution network to ride these secular trends.

The Apogee Difference

Readers will quickly notice there’s far more to Tronox and Fluence than “down a lot, up a little.” These firms operate in must-have industries – sectors where demand isn’t going away just because of temporary disruptions.

Titanium dioxide will always be needed for paints, plastics, and coatings. Battery storage will always be critical as AI data centers expand and renewable energy reshapes the grid. These firms also have years of operating history and strong growth prospects.

That’s how Eric’s Apogee system sets itself apart. It doesn’t just find beaten-down companies… it looks for the ones with clear paths to recovery and identifies the right moment to buy in. It will likely know, for instance, when wind power firm Oersted flips to a “buy.”

In his upcoming special broadcast on September 10 (reserve your spot here), Eric will reveal the details of his Apogee system and reveal, for free, its first five official recommendations. All of them have the potential for 1,000%+ gains.

I’ll have more to share next Sunday — including another sneak peek into Eric’s strategy and several more companies demonstrating Apogee’s “buy” signal.

Until then, be sure to sign up for Eric’s special presentation… and be ready to act when opportunity knocks.

And I’ll see you here next week.

Regards,

Thomas Yeung, CFA

Market Analyst, InvestorPlace