Tom Yeung here with your Sunday Digest.

As we enter the final months of 2025, many traders will be waiting for a familiar market trend to take hold:

The Santa Claus Rally.

This phenomenon has been documented since 1972, and much of it is caused by the “window dressing” that companies use to boost their year-end numbers. After all, December is when performance gets judged and bonuses are paid. (Over the last 50 years, stocks have risen 80% of the time during this period.)

It’s also the period when families go holiday shopping and corporate department heads spend the remainder of the “use it or lose it” budgets. Retailers and software firms alike generate their highest revenues in the fourth quarter.

However, this year’s rally will come with the additional “gift” of volatility as AI-fueled speculation collides with a weakening labor market, an ongoing government shutdown, and record-low consumer sentiment. On Thursday, outplacement firm Challenger reported that last month’s layoffs affected more than 150,000 workers, the highest October figure in 20 years. Even Amazon.com Inc. (AMZN), a firm at the forefront of AI computing, is laying off 14,000 corporate employees (not just warehouse workers) as it embraces generative AI.

We’re already seeing these layoffs cause cracks in the bull market. This week, the tech-heavy Nasdaq Index fell 5% after investors reconsidered their bullish bets. Cost-cutting Amazons fell 6%.

Now, I know most traders consider volatility as something to avoid… much like driving 500 miles to your in-laws the day before Thanksgiving or getting coal in a Christmas stocking. The original concept of financial economics used volatility as its single measure of risk.

But personally, I’ve never heard anyone complain when volatility happens to the upside. AI company Palantir Technologies Inc. (PLTR) is four times more volatile than the broader S&P 500, as measured by implied volatility. Yet, investors seem pretty happy with Palantir’s 206% one-year return.

It’s the downside volatility that people dislike.

That’s why I’d like to reintroduce Jonathan Rose to you all.

Jonathan was a professional trader for 16 years on the Chicago Board Options Exchange, where he saw firsthand how trades are actually done. He’s since turned it into a system that has returned 233% in five days from Rigetti Computing Inc. (RGTI), 534% in three days from MP Materials Corp. (MP), and 959% in 31 days from Albemarle Corp. (ALB).

The wonderful thing about Jonathan’s system is that it performs even better when markets are volatile. It’s these moments when institutional activity reaches a frenzy, causing traders to essentially “tip their hand” of what they’re about to do. Those who recognize what Jonathan calls “unusual trading activity” stand to profit greatly.

To better explain this, Jonathan will be joining his InvestorPlace colleagues – Louis Navellier, Eric Fry, and Luke Lango – to bring you The Profit Surge Event tomorrow, Monday November 10, at 1 p.m. Eastern time. In it, he will explain why the rising volatility we’ve been seeing this week could produce one of the best trading windows of his career.

But be warned… this is your last chance to book a spot for the event before we go live with this free broadcast tomorrow. So, be sure to click here to sign up now.

Now, as we enter the start of a potential Santa Claus rally, I’d like to leave you with three stocks that should perform well heading into the end of the year. These firms have historically been resistant to downward volatility and have recently seen insiders “tip their hand” with some unusual purchases.

Buying the Dip (and Chips Too)

It’s been a terrible, horrible, no good, very bad year for consumer goods stocks.

Shares of Kraft Heinz Co. (KHC) have fallen 22% since January, while Garden Veggie Straws owner The Hain Celestial Group Inc. (HAIN) has plummeted 80%. Even The Procter & Gamble Co. (PG), a symbol of corporate boringness, is down 8% this year.

That’s left many of these ultra-stable companies trading at incredible discounts… right as markets are fretting about sky-high tech valuations.

That’s why Utz Brands Inc. (UTZ) now looks so attractive.

Utz is a Hanover, Pennsylvania-based snack food conglomerate with brands including On the Border salsa and tortilla chips, Golden Flake pork rinds, its flagship Utz potato chips, and more. Its products are available in all 50 states, and its market share has now increased for nine consecutive quarters.

Utz’s profit outlook has also remained steady this year, thanks to its focus on prices and cost efficiencies. Profits are expected to rise 5% this year and 15% the next.

Yet, over the past year, shares of this snack food giant have declined 34% in lockstep with other consumer goods stocks. The stock now trades for just 13 times forward earnings – roughly half of its long-term average.

That selloff has now triggered a flurry of insider buying:

- CEO. Bought 7,200 shares at $10.58

- Chief Financial Officer. Bought 477 shares at $10.47

- Chief Legal Officer. Bought 965 shares at $10.35

- Director. Bought 31,750 shares at $10.58

This type of “cluster buying” is one of my favorite bullish signals, as it indicates that the entire top management team believes their shares are undervalued. Third-quarter earnings met estimates, so there is no good reason for its 12% post-earnings selloff.

Utz is also well protected from potential downturns. Growth remained strong during the Covid-19 recession as consumers traded down, and recent earnings figures from Walmart Inc (WMT) and McDonald’s Corp. (MCD) are suggesting that Americans are doing so again. So, even though consumer goods stocks have faced a terrible, no-good year so far, there’s every reason to believe that Utz will see a special Christmas reprieve as the smart money pivots to lower-risk picks.

A Prescription for Gains

Biotech companies are also an excellent source of “smart money” tips. Executives are paid to closely monitor their clinical trials, and many use this knowledge to trade shares of their company before the results are officially tallied.

After all, if half of the patients in a double-blind clinical trial are suddenly getting cured, it’s a sign that the drug is working. (And if half are dropping dead, that suggests the opposite.)

For instance, insiders at biotech startup Longeveron Inc. (LGVN) began cluster buying shares in mid-October 2021. The stock surged 800% two weeks later after the company announced that its Lomecel-B treatment qualified for the Food and Drug Administration’s Rare Pediatric Disease designation. More recently, Nuvation Bio Inc. (NUVB) saw significant insider purchases in June 2025, three months prior to unveiling promising Phase 2 results. Its CEO is now sitting on 175% gains from that trade.

That’s what makes Greenwich LifeSciences Inc. (GLSI) a bet worth looking at.

The Houston area-based biotech is developing a cancer immunotherapy drug that aims to enhance the effectiveness of existing breast cancer treatments. Its flagship therapy is currently in Phase III trials and is expected to conclude by the end of 2026.

Over the past several months, the company’s shares have fallen 33% due to heavy short selling. Greenwich spent 25% more than expected in the third quarter, and markets punished this by increasing the percentage of shares sold short to 10%, up from 4% at the start of the year.

Now, the tide seems ready to turn in the other direction.

On November 4, the company’s CEO purchased 2,300 shares of the firm at $9.26, marking his first investment since April, when positive preliminary data from its Phase III clinical trial were announced. Recent 13F filings as of September 30 show that positions held by large funds are now rising again, rather than falling.

There’s a strong reason to believe more money will continue flowing into Greenwich’s beaten-down shares.

In September, GLSI received an FDA Fast Track designation, a process awarded to crucial drugs that have met certain efficacy criteria. The firm also received formal approval from European regulators to expand its Phase III trials. The following month, Greenwich announced it would extend its Phase III trials to Belgium and Austria.

It’s also worthwhile remembering that Greenwich’s Phase IIb and initial Phase III results triggered robust immune responses that reduced recurrence of metastatic breast cancer to 80%, compared to 20% to 50% by currently approved products.

This suggests that Greenwich’s $115 million market value is too low. Breast cancer is the second-most common form of that disease, and the type that Greenwich’s drug targets affects 15% to 20% of all breast cancer cases. (Recent Phase III data suggests it could be even more.)

It’s an enormous market, and large oncology players like Roche Holdings (RHHBY) and Pfizer Inc. (PFE) might be willing to roll the dice on acquiring this promising firm as regulators and insiders make positive bets on initial Phase III results.

Drilling for Value

Finally, this week brings us a company with an uncanny ability to buy its own stock at irresistible prices:

Matador Resources Co. (MTDR)

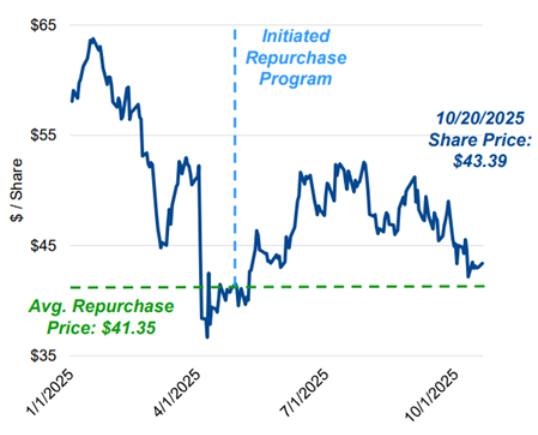

This midcap oil and gas company has seen 12 separate directors and managers buy shares in the wake of third-quarter earnings. CEO Joseph Foran alone bought almost 15,000 shares for under $39.

This is the kind of unusual money flow worth watching. In April 2025, Matador initiated its share repurchase program right before prices began recovering from America’s “Liberation Day” selloff. That period also coincided with a separate round of insider buying; some managers were sitting on 35% paper gains prior to the most recent selloff.

Taking advantage of market volatility

And now, management is doing it again.

There are three reasons to believe management is correct again in their purchases.

First, Matador has a relatively attractive cost structure thanks to its concentrated acreage in West Texas’s Delaware Basin. Its primary sites are linked by 650 miles of pipelines, and lease operating expenses are roughly $5.75 per barrel. That figure is within striking distance of America’s lowest-cost producer, Diamondback Energy Inc. (FANG).

In addition, Matador’s total operating expenses (which add depreciation, overheads, and taxes) are roughly $35 per barrel, not much higher than FANG’s $25 figure and in line with low-cost producer EOG Resources Inc. (EOG) before interest.

Second, shares are relatively inexpensive compared to their underlying assets and profitability. MTDR trades at an industry-low 0.81X book value and 6.3X forward earnings, a roughly 20% to 35% discount to its larger peers. That gives Matador double-digit upside from a potential re-rating.

Finally, Matador’s shares offer diversification from the high-priced tech market. The stock generates a healthy 4% dividend yield and saw prices rise 2% on Friday even as the tech-heavy Nasdaq Composite dropped 2%.

If institutional cash begins pivoting into safer assets, Matador offers a compelling place to store cash.

The Profit Surge Event

The three trades I highlighted above demonstrate how insider transactions can signal significant gains to come. “Smart money” buyers possess more knowledge than average investors, and studies have consistently shown that insider buying is one of the best bull signals.

Still, these sums are tiny compared to the millions (or billions) of dollars that institutional investors can pour into a firm. And when these dollars begin pouring in, that’s when you know that future gains are about to happen.

So, once again, I urge you to sign up for tomorrow’s Profit Surge Event. Jonathan Rose will be explaining how he’s starting to see some incredible sums get passed through the market, and why this volatile rally could be unlike any seen before.

Until next week,

Thomas Yeung, CFA

Market Analyst, InvestorPlace