Listen to the audio version of this article (generated by AI).

Tom Yeung here with your Sunday Digest.

Last week here, we talked about how master trader Jonathan Rose and Wall Street veteran Marc Chaikin had combined their smart money indicators into a “Convergence Trigger” signal.

They revealed their system’s top five picks in their Convergence Summit on Thursday night. I hope you tuned in. The pick I featured here in the Sunday Digest from that list – Ameresco Inc. (AMRC) – has already risen 10% since then, bringing its one-month return to 18%. In fact, the five companies Jonathan and Marc selected have now risen 38% since the start of May.

Now, it’s tempting to think it’s too late to jump in. Jonathan and Marc’s five stocks are all a part of the AI Revolution, and many investors are rightly wondering how high things can keep going. After all, all “Big 3” dynamic RAM memory chip makers – Micron, Samsung, and SK Hynix – are now worth $1 trillion each.

Could they possibly be worth $2 trillion? $5 trillion? Or more?

Fortunately, I’m quite certain that at least one of their “Convergence Trigger” companies still has further upside. I’ll tell you why in this update.

In the meantime, be sure to tune into a replay of Jonathan and Marc’s Convergence Summit if you haven’t seen it yet. In it, they explain how their system works, and how you can use it to make sure the next investment boom doesn’t pass you by. (And don’t wait long… our publisher will be removing the video later this week.)

Now, here’s more on that “Convergence Trigger” stock that I believe still has some juice in it…

The Sunny Outlier

First Solar Inc. (FSLR) is a rather fantastic company. This Tempe, Arizona-based solar company doesn’t have just one moat around its business… but rather it has four. Let’s go through each.

1. Product. First Solar is the only company in the world that can produce cadmium telluride (CdTe) photovoltaic cells at scale. Unlike crystalline silicon (c-Si) panels, CdTe versions are straightforward to build and highly resistant to heat and long-term degradation. That makes them superior in hot and humid environments like the U.S. South, India, and the Middle East.

This moat is protected by numerous patents, $2 billion in cumulative research and development spending, and a proprietary manufacturing process that even General Electric (GE) couldn’t figure out. GE exited the CdTe business in 2013.

2. Supply Chain. First Solar is also protected by a quirk of its technology. CdTe panels require no polysilicon, no silver paste, and no wafers. Instead, their panels are essentially glass, steel, and a thin layer of proprietary cadmium telluride compound.

That’s particularly important because China controls roughly 80% of the global supply of c-Si panel components. Rivals like Canadian Solar Inc. (CSIQ) are low-margin businesses because they rely on Chinese suppliers that can dictate terms and prices. First Solar faces none of those challenges.

In addition, First Solar is vertically integrated. It controls its own tellurium sourcing, module assembly, and even end-of-life-recycling to handle and reuse the cadmium in its panels. Each step is relatively difficult — for instance, telluride is geologically as rare as gold, and cadmium can be as dangerous as mercury. Assembling the whole chain under one roof makes this moat especially wide.

3. Government Subsidies. The U.S. solar industry is currently protected by two pieces of legislation that the 2025 One Big Beautiful Bill confirmed:

- Section 45X. This series of production-based tax credits overwhelmingly benefits First Solar because credits for cell production and assembly are stacked. In fact, the company generated so many of these credits that it sold $1.3 billion worth of them in 2025, making up a quarter of total revenues.

- FEOC Restrictions. This consumer-based tax credit requires buyers avoid Foreign Entity of Concern (FEOC) panel makers to claim their own credits. First Solar clears this hurdle easily given its domestic CdTe supply chain. These rules last through 2027 for project-level credits and until 2032 for manufacturing credits.

I expect both to get extended in some fashion. In April 2026, a group of Republican congressmen from Pennsylvania, New York, and Ohio proposed legislation to preserve commercial solar tax credits to protect firms like First Solar, which has a large presence in the region. Meanwhile, FEOC rules were strengthened under the current administration, and any trade war with China will likely trigger an expansion. Even though the White House has publicly criticized the solar industry, its actions have moved in the other direction.

4. Financial Strength. I ordinarily don’t award a “moat” for financial strength, since anyone with a large enough pocketbook can step in. But I’ll make an exception for the solar industry because everyone else is in such terrible shape. Canadian Solar, JinkoSolar Holding Co. (JKS), and Sunrun Inc. (RUN) all have debt-to-equity ratios of over 250% and struggle to afford payments on interest. China’s LONGi Green Energy Technology Co. Ltd. has lost money since 2024 and will likely keep doing so until at least 2027. The c-Si panel industry is a cutthroat business.

Meanwhile, First Solar has maintained a fortress balance sheet, thanks to its 30% profit margins from its differentiated product. The company has $2 billion of net cash on its books, almost no debt, and is expected to generate $1.8 billion of free cash flows next fiscal year, up from $1.2 billion in 2025.

This financial strength has allowed First Solar to continue investing in research and development ($270 million this year) and spending on production capacity ($884 million). It outspends its rivals by almost 3-to-1 on R&D and could be the company to bring next-generation technologies like perovskites to market. (These calcium/titanium/oxygen crystals would be a major step forward if they can get scaled up.)

Dawning Demand

These moats suggest that First Solar still has room to run. Shares have risen just 11% this year, even as electricity demand from AI data centers has continued to rise.

Consider the math. The latest Blackwell chips from Nvidia Corp. (NVDA) draw roughly four times the power of what the prior generation needed and produce far more heat. Multiply that across thousands of racks, and you start to understand why data center operators are scrambling for power-generation capacity for chips and cooling.

So, where will that juice come from?

Increasingly, data center operators are turning to the sun. The solar production curve roughly matches demand for data center cooling, solar farms are quick to build, and solar power pairs well with electricity from natural gas and batteries. The U.S. Energy Information Administration estimates that 51% of planned grid capacity additions in 2026 will be solar.

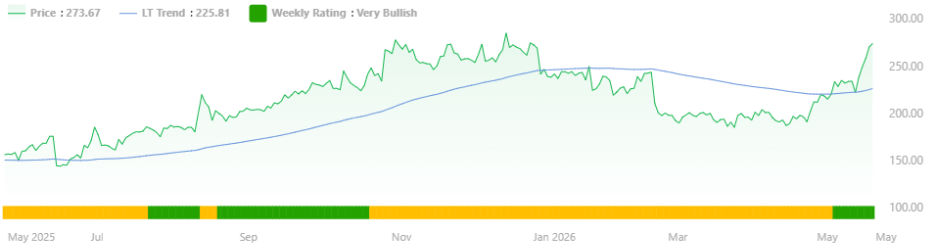

First Solar also easily passes Jonathan and Marc’s smart money screens. Shares have recently flipped to “Very Bullish” in Marc’s system on strong smart money buying. As you can see from the graph below, his system has consistently found the best times to buy.

Marc Chaikin’s First Solar Inc. (FSLR) Rating

I also believe there’s more room for First Solar to grow. Only 17% of installed panels in the U.S. are currently CdTe, and barely 2% of global capacity uses the technology. That gives the company a long runway for growth. In the most recent quarter, First Solar announced record sales in India, and said that its backlog now sits at 47.9 gigawatts, or more than 2.5 years of revenues.

Rays of Caution

Obviously, there are longer-term risks for a company like First Solar:

- Regulatory. First Solar faces an earnings cliff in 2027 when subsidies start to expire. Without any changes, one of its widest moats could dry up by 2032, taking as much as a third of revenues along with it.

- Tariffs. Import taxes on Southeast Asian c-Si imports could be reduced, eroding the company’s pricing power

- Future Products. First Solar’s success in perovskites is not guaranteed. Though these crystals have shown efficiency ratings as high as 34% (compared to 26% for c-Si), this has only been proven at tiny scales. Lossmaking LONGi Green Energy is also pursuing this technology

Nevertheless, markets have more than priced these fears in. First Solar’s shares trade at just 11X forward earnings, or roughly a third of comparable companies in the AI power buildout. If regulations move the way I expect, shares have at least a 50% upside from here.

The Swiss Cheese Model Part 2

As I wrote here last week, markets have a lot of pressure building up beneath the surface. Many retail investors are now chasing returns of the hottest stocks, and analysts at Morningstar (and many others) are warning that companies like Micron Technology Inc. (MU) should “expect the wave to crash longer-term.” Morningstar analysts give Micron a fair value of $455, a 50% downside.

Fortunately, Jonathan and Marc’s “Convergence Trigger” system helps investors avoid these pitfalls by forcing investment ideas through multiple screens. Even if smart money is giving bullish signals for Micron’s stock, options traders might have an entirely different outlook.

And so, be sure to watch their Convergence Summit, where Jonathan and Marc will explain where they see the next pockets of opportunity, and how they’re navigating this “new normal” of markets that rise quickly and fall just as fast.

Until next week,

Thomas Yeung, CFA

Market Analyst, InvestorPlace