Retail has been the second-worst sector in the S&P 500 this year. However, Target (NYSE:TGT) has outperformed in 2020, with Target stock down 23.3% vs. a 32.6% decline for the retail sector.

This outperformance doesn’t make Target a buy on its own. However, there are clear reasons that the stock has been outperforming in this mess and it’s something to take note of. We’ve seen that unfold plenty since February, so let’s explore why Target is still one of the best names in retail.

Why I Like Target Stock

There are a handful of retail players that are transforming or already fit the mold for retail’s future. Those names include Target, Walmart (NYSE:WMT), Costco (NASDAQ:COST) and Amazon (NASDAQ:AMZN). You could include a few brand-specific names too, like Apple (NASDAQ:

AAPL) and Nike (NYSE:NKE), but these are companies that make their own products and happen to be great at retail. For this purpose, we are talking about the big-box retailers.

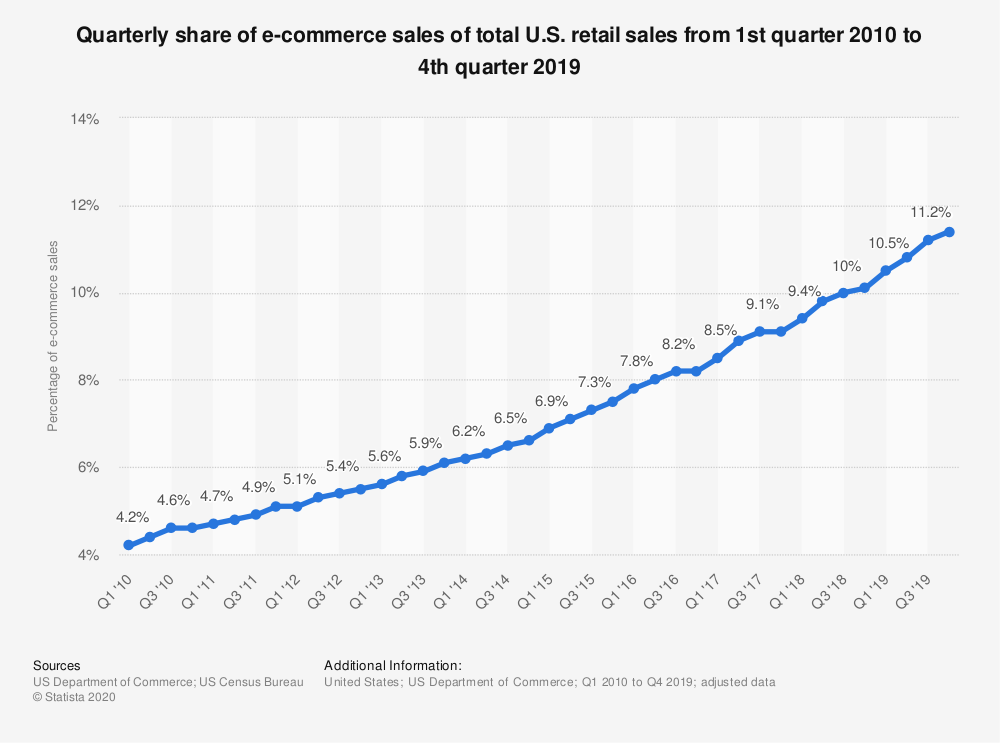

Click to Enlarge

Walmart, Costco and Target rely on a bulk of their profit to come from in-store shoppers, but they are focused on growing sales via e-commerce. Physical retail locations will always have a role to play for consumers, but they are increasingly looking for online solutions. Those that can do both, like these three, will be long-term winners.

But let’s not forget the other positives for Target stock. The company pays out a 2.7% dividend yield and trades at a reasonable 14.7 times earnings. Despite the recent novel coronavirus impact, analysts still expect positive revenue and earnings growth this year and next year. That’s even with the “recession” word — and in some circles, the “depression” word — being tossed around.

Let’s put it another way. Investors who are interested in Target stock can begin accumulating this retailer with a 2.8% dividend yield and below-market valuation, while still trading at a near-25% discount from its Q4 high. That’s even as Target is forecast to have positive sales and profit growth this year and next year, and remains a long-term winner in the space.

Target and the Coronavirus

Obviously the coronavirus has thrown a wrench into the system. It’s got investors worried about financial markets, the labor market, the health system and a whole host of other concerns. It’s just not a good situation.

However, the silver lining is that things will get better. It’s just a question of when, not if.

Over the last several quarters, Target stock has had plenty of bullish momentum. The company would report blowout numbers, the stock would rip higher, consolidate sideways and repeat the pattern on another strong quarter. That is, until this quarter.

Target reported earnings on March 3. The company missed on revenue estimates and reported comp-store sales growth of just 1.5% vs. expectations of 2.1%. Keep in mind, the quarter ended before the impact of the coronavirus. So it had lost some momentum before the chaos hit. One quarter doesn’t tell the whole story, but it’s worth pointing out.

With investors talking about a recession, retail should be flattened. That’s not the case for Target, though.

Management said store traffic has been robust, as have sales. Near the end of the month, comp-store sales for March were up 20% year-over-year. While units like apparel were suffering, essentials, food and beverages were up strong. A few weeks ago, I noted that in-store alcohol sales were also strong for retail across the board.

Bottom Line

Target has been seeing a boost, not a shortfall in traffic in sales. That said, the company suspended its buyback and pulled its prior guidance due to the wide-ranging outcomes that are possible. Further, the company is now set to limit the number of customers in stores to help promote social distancing.

Perhaps that creates some short-term weakness in the stock over the next few quarters. Maybe the results will still be better than expected. It’s hard to say with so much uncertainty in the world right now.

However, what’s not uncertain is Target’s long-term trajectory at this point in time. This retailer is a winner and has a lot of positive attributes. With such a discount from the highs, long-term bulls should consider accumulating a position.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.