After a post-earnings pullback, shares of Alibaba (NYSE:BABA) are heating up again. Can Alibaba stock make a run for its prior highs?

With the Invesco QQQ ETF (NASDAQ:QQQ) hitting new all-time highs — yes, all-time highs — mega-cap tech is clearly in favor at the moment. To some degree that includes Alibaba, although it has not done quite as well as some of its other peers.

Given the strength in the company’s underlying business, combined with the (unfortunate) benefit it receives from the novel coronavirus, Alibaba stock should continue higher with its peers. Let’s explore three reasons why.

Growth, Growth, Growth

We were lucky with our investment analysis when it came to the impact from the coronavirus. In hindsight it seemed obvious, but at the time, not many investors were looking for such a massive run in the stock market. In any regard, we postulated that high-growth companies — which already command higher valuations — deserve an even higher premium amid the current pandemic.

This led to the inevitable question: Why pay a premium when we’re in a recession?

While understandable on paper, that mindset is flawed in reality. The reasoning is simple. Most companies will struggle to post break-even revenue and earnings growth this year. A small percentage of stocks will have growth this year and an even smaller percent will have robust growth.

These are the companies that deserve a premium — and Alibaba stock is among them.

Alibaba is forecast to grow revenue 30% this year, followed by 25.5% growth forecasts next year. There are not many companies with a $575 billion market cap that are growing sales at 25% to 30% a year.

Earnings are expected to take a bit of a hit this year due to extra coronavirus-related costs. However, they are still forecast to grow almost 14%, followed by 27% growth next year.

It’s Not Just Covid-19

Some investors may point to Covid-19 being the sole catalyst for Alibaba’s rising revenue figure. I would argue that that’s false.

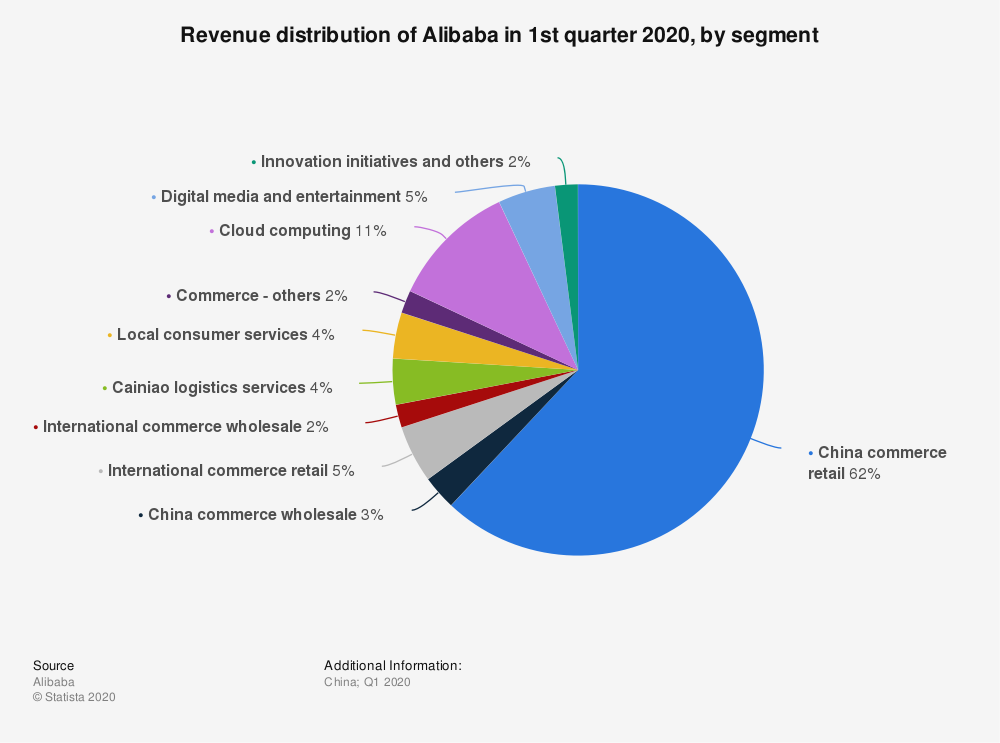

Four years ago, Alibaba was highly reliant upon its e-commerce segment. To be fair, it still is. If this unit vanished, it would be in a great deal of trouble. But like Amazon (NASDAQ:AMZN), the company is diversifying.

Alibaba now leans on cloud-computing for growth. It also leans on digital media, logistics, and investments in FinTech companies. Put simply, Alibaba relies heavily on e-commerce, but is tapping into different growth segments to diversify its revenue. While sales seem to benefit from Covid-19 — and more online ordering — profit is not.

Thankfully, it goes beyond growth.

Alibaba stock trades at about 28 times this year’s earnings estimates. That’s really not an egregious price to pay when considering its growth rate, market cap, and future growth potential. Plus, on a price-to-earnings ratio, that’s cheaper than Microsoft (NASDAQ:MSFT), Amazon, Netflix (NASDAQ:NFLX) and Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG).

Additionally, it has better revenue growth than all of these companies. That really says something.

Alibaba Stock Has Strong Technicals

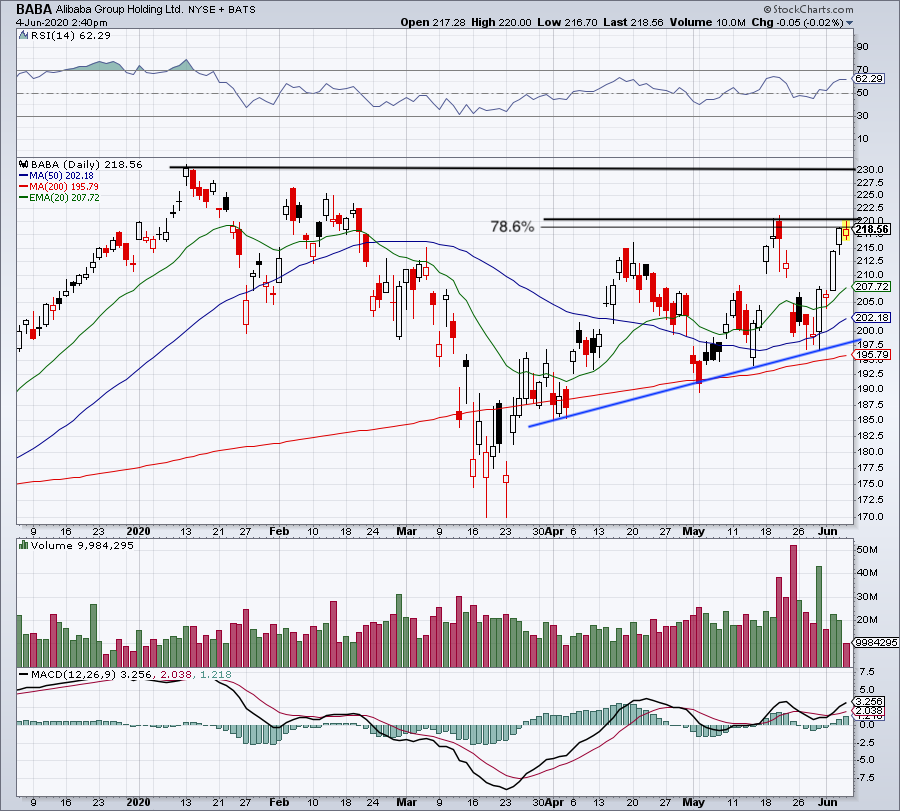

Click to Enlarge

Finally, let’s look at the charts.

Alibaba stock has been ripping back to life, bouncing hard off the 200-day moving average after a post-earnings shake-out late last month.

Shares held the 50-day moving average, then reclaimed the 20-day moving average and jumped higher. The rally sent Alibaba stock into $220 resistance and the 78.6% retracement near $218.

Now bulls have to be a bit careful. If shares pull back, let’s see if the 20-day and 50-day moving averages hold as support. Should we get a deeper correction, that’s okay. But uptrend support and the 200-day moving average must hold as support. That said, it would be more bullish if the 20-day and 50-day moving averages held strong for bulls.

On a breakout, let’s see if Alibaba can rally up to the prior highs near $230. Over this mark would obviously trigger a breakout.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.