Alibaba (NYSE:BABA) is a stock I have loved, and the recent price action has been rewarding for those who are long. Alibaba stock burst higher on July 8, rallying 9% to new all-time highs.

The action comes after several strong days of gains, with BABA stock up 15% so far this week and almost 20% for the month of July. In short, this stock has been a monster and Ant Financial’s potential IPO only makes it more attractive.

Alibaba holds a 33% stake in Ant Financial, which is seeking an IPO in Hong Kong. The company is looking at a valuation of more than $200 billion, with plans to sell 5% to 10% of its shares.

It’s not clear how much of its stake Alibaba may pare down in the offering. Whether it does or not though doesn’t matter, as investors will want to see how Ant performs in the future.

That is, if the stock appreciates, so too will Alibaba’s stake. Sad as it may seem, many investors in Alibaba may have very well not even realized it has a stake in Ant Financial. That may help explain why shares rallied 9% on the day and gained momentum through the trading session, as they made this realization.

Obviously the potential IPO won’t happen overnight, but it should be viewed as a positive catalyst for Alibaba. For me, Alibaba’s stake in Ant has been one of the reasons I’m bullish on BABA. Thankfully though, there are other reasons to consider a long position too.

Valuing Alibaba Stock

One of my favorite things above Alibaba is its underappreciated business. Not that Alibaba is really flying under the radar so to speak — with its $668 billion market capitalization and huge rally over the past few weeks — but it’s not the size of Amazon (NASDAQ:AMZN), Apple (NASDAQ:AAPL) and others.

I have argued in the past that companies still churning out growth amid the novel coronavirus deserve a higher valuation. That’s even more true for companies with robust growth.

Consensus expectations call for more than $94 billion in sales this year. If hit, it will represent more than 30% revenue growth from fiscal 2020 (last year). Revenue growth of 20%-plus is expected to continue for the next few years, too.

Alibaba has beat on earnings estimates for seven consecutive quarters. As it stands now, forecasts call for earnings of almost $9 per share this year. That leaves the stock trading at less than 29 times earnings. While not cheap by traditional measures, let’s remember a few things.

First, it holds the

most dominant e-commerce position in China, a country that has a booming middle class and a population four times the size of the U.S. Second, it’s diversifying into other revenue segments, like cloud computing and digital entertainment.

Finally, it has better revenue growth and a lower price-earnings ratio than Apple, Amazon, Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL).

These other companies have great attributes too, but I feel that Alibaba stock doesn’t get the same type of respect these other names do. It has solid, secular growth and a reasonable valuation. That’s oftentimes a tough combination to find.

Trading BABA Stock

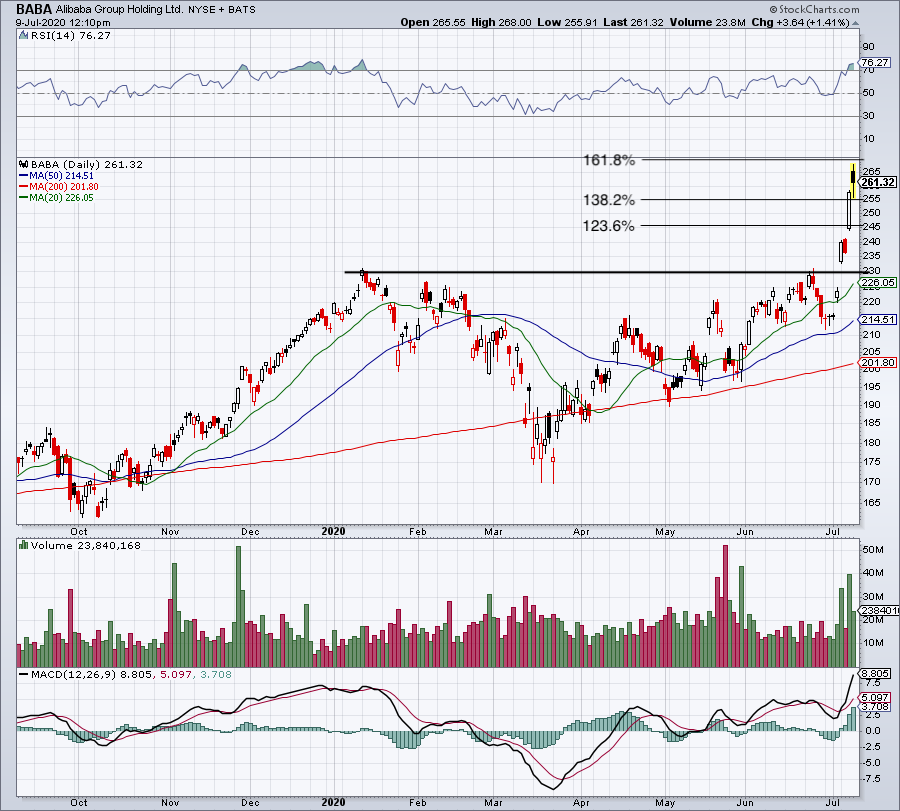

Click to Enlarge

The fundamentals and future catalysts check out, but what about the technicals?

The biggest critique investors could have regarding the chart is that Alibaba stock has gone too far, too fast. On the week of July 5, the first full week of the month, shares burst through $230 resistance. This mark twice held shares in check, but finally gave way.

After the Ant Financial news hit the wires, shares were able to push through the 123.6% and 138.2% extensions. With a close above the latter, it technically puts the 161.8% extension in play, up at $268.96.

While the stock is starting to get extended, its overbought/oversold readings are not in extreme territory just yet. If Alibaba stock pulls back and moves below the 123.6% extension, it could fill the gap from July 8 and potentially retest $230. For long-term investors who missed the boat, this level could provide an excellent buying opportunity.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now. As of this writing, Matt did not hold a position in any of the aforementioned securities.