Yes, they may be entrusted with the safety and stability of the U.S. financial system, but when it comes to putting dollars into investors’ pockets, the “Big Four” bank stocks — in particular, Bank of America Corp (BAC) and Citigroup Inc (C) — have been found lacking.

On a year-to-date basis, they’re the worst of the bunch, and despite the recent comeback from February’s bottom, both bank stocks show very mixed signals. Is there any relief in the much-troubled financial sector?

On a year-to-date basis, they’re the worst of the bunch, and despite the recent comeback from February’s bottom, both bank stocks show very mixed signals. Is there any relief in the much-troubled financial sector?

At cursory glance, it doesn’t look too promising. The benchmark exchange-traded fund Financial Select Sector SPDR Fund (XLF) is the worst laggard, down more than 5%. The next worst is the heavily embattled Health Care SPDR (ETF) (XLV).

But the most sobering point is that so far this year, the majority of industries are into positive territory. The fact that the major bank stocks can’t get some of that market love is disappointing to say the least.

However, it’s not all doom and gloom for the financials. With the exponential growth of the digitalization of everything, more people have access to financial services than at any other point. And the reality is that the “underbanked” population — or those that have limited access to traditional banking services — represent about a third of all Americans. While we are certainly more sophisticated financially than most other countries, it’s clear that even here in the world’s sole superpower, there’s a lot of room for opportunity.

That opportunity, though, best suits bank stocks that are unencumbered by aging assets and massive overhead costs. Without the prying eyes of all of Wall Street, mid-capitalized and regional banking firms have greater agility — and far less pressure — to adapt to new trends in finance. For investors, that means far greater returns for mid-cap bank stocks compared to their bigger brethren.

Here are three mid-cap bank stocks that will likely slip past the competition.

Mid-Cap Bank Stocks to Buy: Flagstar Bancorp Inc (FBC)

Click to Enlarge

Tired of putting money into major bank stocks, only to end up severely disappointed? Flagstar Bancorp Inc (FBC) might be the better bet. FBC is a near-$14 billion savings and loan holding company which is headquartered in Troy, Michigan. Under the FBC banner, Flagstar Bank is the largest bank from that state, and is one of America’s largest providers of mortgage loans.

While many outside of Michigan may not be familiar with FBC, it’s making a name for itself in the markets. Over the last five years, FBC stock is up 83%. Compare that to Bank of America, which is up a less impressive 28%. Citigroup has fared even worse, only mustering 12% over the same time frame.

In addition, FBC is one of the few names among bank stocks that are in positive territory. Sure, it’s a technicality. But it’s something that the Big Four bank stocks haven’t accomplished, down an average of 13% year to date.

Just as importantly, Flagstar is also making steady progress on its fundamentals. In recent quarters, FBC has produced very strong earnings results. After registering a slight miss against earnings expectations for the fourth quarter of fiscal year 2015, the company responded strongly in Q1. FBC

posted a profit of $39 million, resulting in a positive earnings surprise of 53%.

Don’t get me wrong — the financial sector is a tough pill to swallow. However, FBC is one of the shining gems that could continue to shame their bigger competitors.

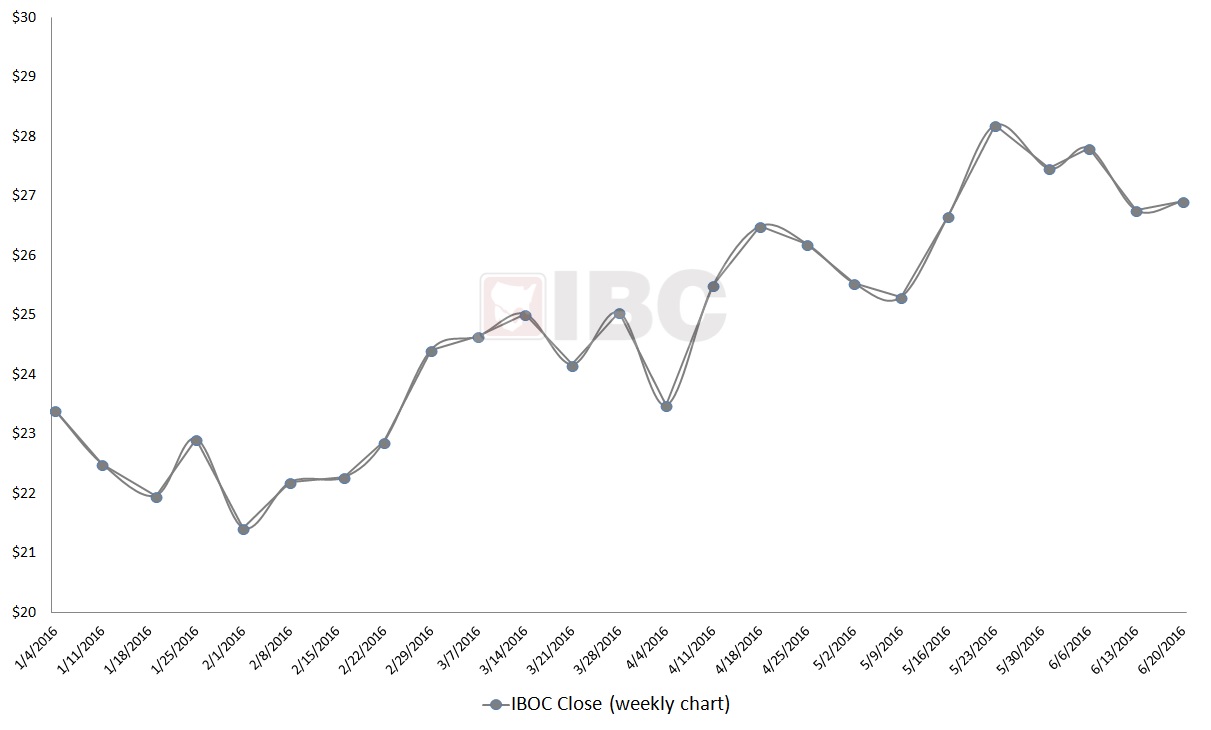

Mid-Cap Bank Stocks to Buy: International Bancshares Corp (IBOC)

Click to Enlarge

One of the compelling reasons to consider mid-cap bank stocks is that regional institutions have a strong understanding of their core markets.

Headquartered in Laredo, Texas, International Bancshares Corp (IBOC) serves 88 communities in the Lone Star State and neighboring Oklahoma. Catering towards small businesses, IBOC has nurtured and developed relationships with their clients since its founding in 1966. That extra step towards excellence has garnered it several industry awards, as well as earning praise from local Hispanic-owned businesses.

IBOC notes proudly on its website that it has never had a “down year,” a winning streak that continues to this day. Indeed, IBOC has an enviable net income growth rate of 2.4% over the last ten years without any loss of profitability. In contrast, some of the major bank stocks have negative earnings growth due to sharp losses incurred during the crash of 2008. Or, as is the case with BAC, their earnings growth looks great on paper simply because they set the bar low from prior misses.

Of course, market performance is where it really matters. Here again, IBOC separates itself from the rest of the pack. On a YTD basis, IBOC stock is up nearly 5% — almost unheard of in the financial sector graveyard. At present, shares appear to be rising in a “step-wise” pattern characterized by a rally following a consolidation period.

Given the historical track record of IBOC both in good times and in bad times, it’ll be hard to bet against the company.

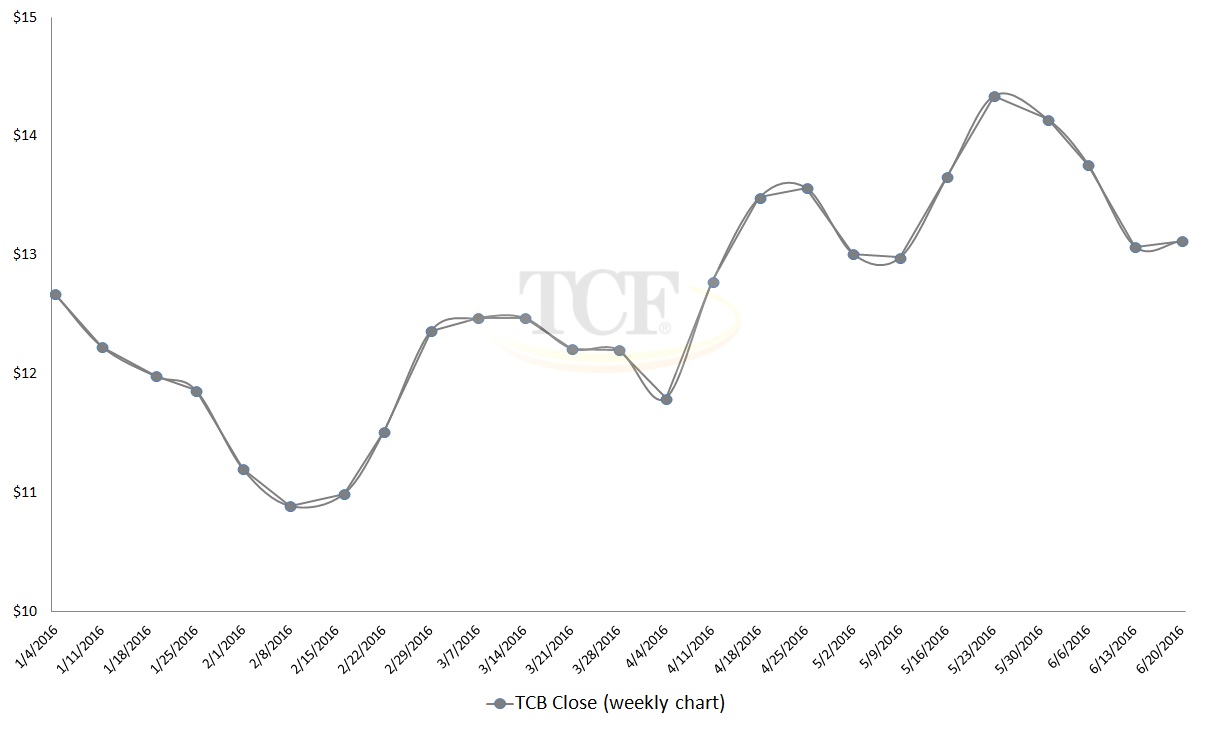

Mid-Cap Bank Stocks to Buy: TCF Financial Corporation (TCB)

Click to Enlarge

Within the money business, there’s always going to be some level of snobbery. In the case of TCF Financial Corporation (TCB), it’s banking on it. Famous for its free-to-open checking accounts, TCB is offering a new twist — services sans checking accounts.

Called “Zeo” accounts, TCB allows new clients to exercise services such as debit cards, cash withdrawal and direct deposit without having to open a traditional checking account. Best of all, the cost of entry is as low as $25. That’s something that JPMorgan Chase & Co. (JPM) would scoff at. But for TCB, it fits the bill quite nicely.

There’s a wide-open opportunity among America’s unbanked community — and TCB is hell bent on taking it.

Although terms like “unbanked” or “underbanked” have a negative connotation, there are a significant number of individuals that eschew traditional banking in favor of alternative financial services. For the parties involved, it’s a win-win. Clients get the services they want, and TCB can collect the money for investment into other areas of their business. Best of all, the major bank stocks aren’t interested, so competition from them is a nonissue.

What I like about the Zeo accounts is that it perfectly meshes with the fundamental needs of TCB. In terms of its top-line income stream, the one weakness that stands out is non-interest income, or income generated through activities not related to the balance sheet.

Over the last four years, no-interest income represents an average of 35% of total revenue. This figure is seeing no real improvement, while interest income is rising. The new Zeo accounts should bring a healthier balance, and potentially boost the trajectory of TCB stock.

As with other bank stocks, TCB is a calculated risk, but with that said, you have to love management’s decision to play into their strengths.

As of this writing, Josh Enomoto was long Flagstar Bancorp.