Reality has finally started kicking down the doors of the grocery industry. Pressured in recent years by record levels of food price deflation, grocery stores face an uphill battle in the markets. Unfortunately, things may get worse before they get better. Deciding to bite the bullet, Sprouts Farmers Market, Inc (NASDAQ:SFM) slashed its quarterly and full-year guidance on Wednesday. While the announcement isn’t exactly surprising, Wall Street punished SFM severely, making it one of the worst performing stocks for the day.

Click to Enlarge

But the real uppercut to the jaw is Sprouts’ admission that the food price deflation would likely be an overhang for months. Since grocery stores typically operate on razor-thin margins, the only feasible solution is to promote discounts aggressively.

However, the volume for margin game is not an exclusive one. Competitors will certainly take note, even those companies that don’t have a majority of their business levered towards food sales. It all makes for a dog-eat-dog scenario, thus leading to sharp volatility across multiple grocery stores.

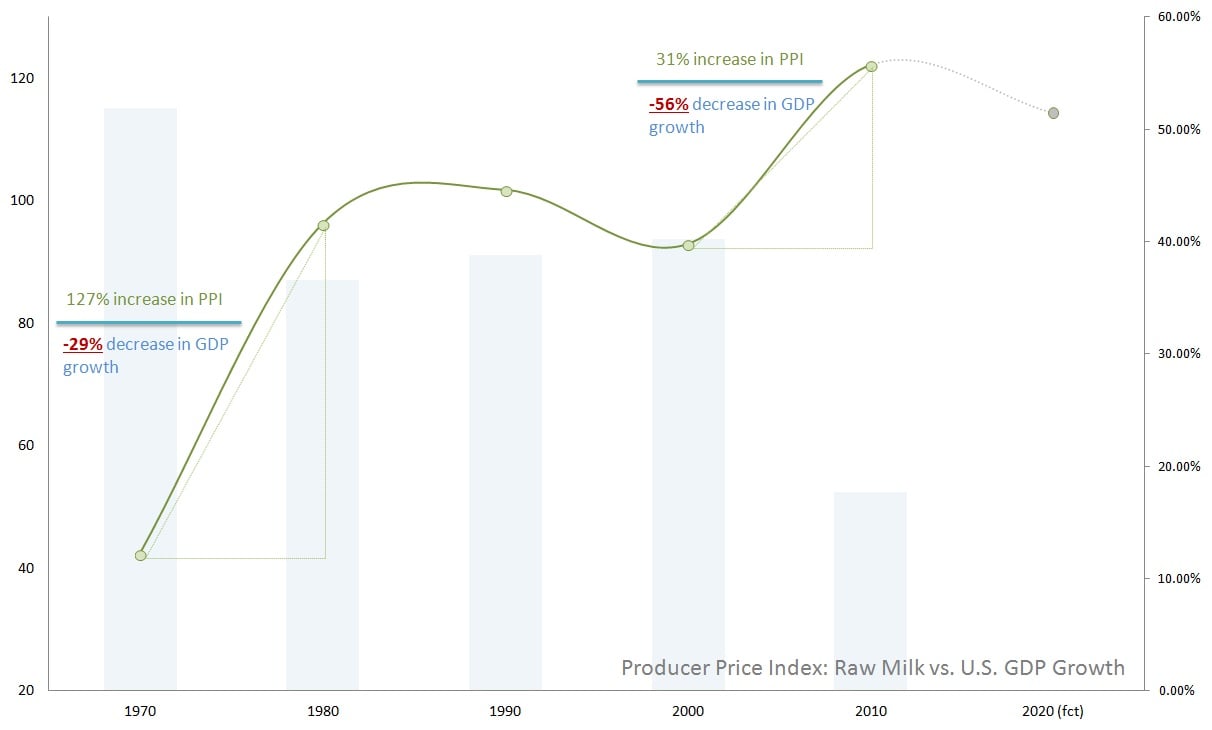

Contrarians tempted to buy into the panic should take some time to think over their strategy. The agricultural industry has taken quite a hit on commodity prices, where the impact will likely reverberate. Over the past six-and-a-half years, the producer price index for raw milk has declined by 6%. Over the trailing-30 months, the PPI has eroded by an average of 10%. At that rate, the index could possibly fall by double-digits by the end of the decade.

Macroeconomic headwinds — particularly the strong U.S. dollar — will also pose serious headaches. Massive consumers of American goods, such as China, have been forced to cut back due to the unfavorable currency exchange rate. In addition, the global economy isn’t exactly running on all cylinders, leading to a top-line drain for food producers. That constriction leads to further problems for grocery stores.

No matter which way you turn, the food distribution industry is in quite a pickle. Here are three grocery stores that you’ll definitely want to leave on the shelf.

Grocery Stores You Should Leave on the Shelf: Kroger Co (KR)

Click to Enlarge

As one of the direct competitors to Sprouts Farmers Market, Kroger Co (NYSE:KR) should be viewed as at least being a nearer-term investment risk. Wall Street evidently thought the same. KR stock took a pretty good beating, gapping down to a 4% loss on Wednesday. Adding to the pressure is the fact that Kroger is set to release its second quarter of fiscal year 2017 results this Friday.

Can KR pull off a miracle?

We Americans have a never say never attitude. However, KR stock might be an exception. The consensus earnings per share target of 45 cents is definitely near the lower range of estimates. Compounding matters is the fact that profitability margins for KR are middling compared to the industry. That’s offset somewhat by better-than-average revenue growth over the last three years. But with the kind of red flags being raised in the sector, it’ll take a remarkable performance to impress the markets.

As a secular company, KR has benefited from consistent demand driving up its share price. This year, though, has been a downer for just about every industry participant. Since the beginning of January, KR is trailing by more than 25%. Even with an unlikely earnings beat, it would take considerable effort to convert gun-shy investors.

There’s no doubt that KR has performed admirably under the circumstances. Sadly, there’s simply too much crossfire that will prevent any company from getting away cleanly.

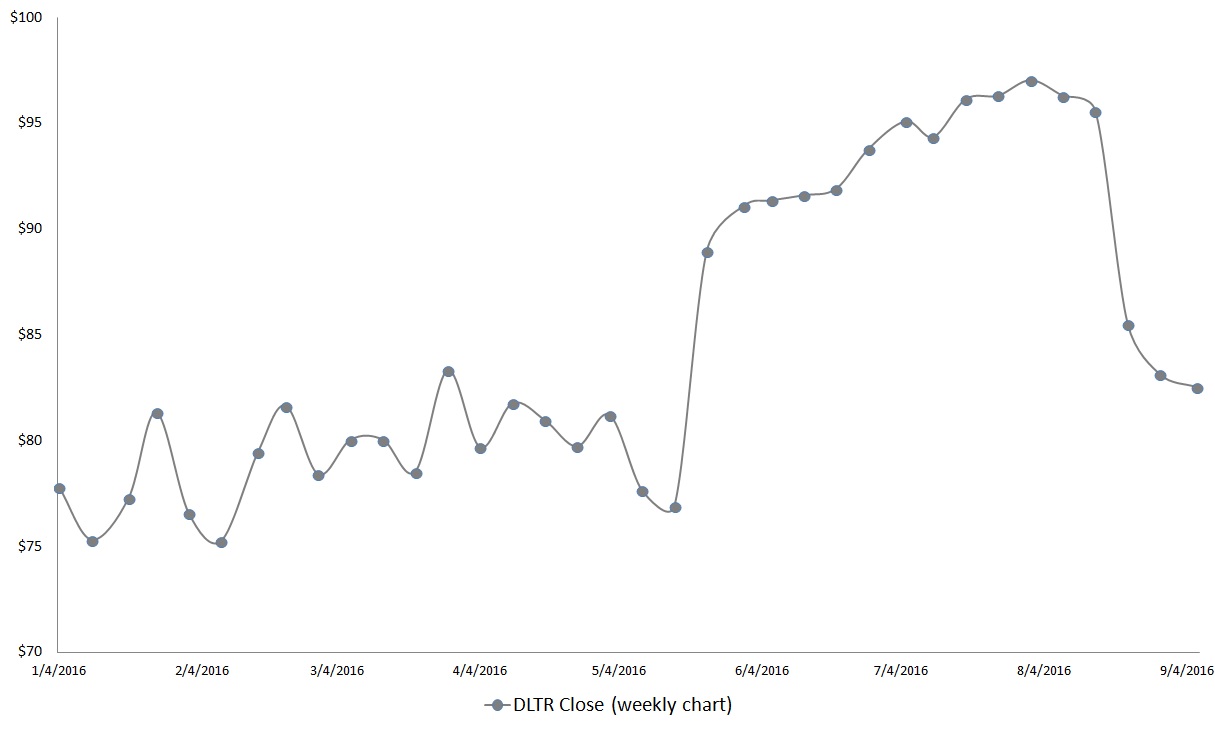

Grocery Stores You Should Leave on the Shelf: Dollar Tree, Inc. (DLTR)

Click to Enlarge

For Dollar Tree, Inc

. (NASDAQ:DLTR), the tough road ahead is just a matter of inevitability. Last month, chief rival Dollar General Corp. (NYSE:DG) cited food price deflation as a major threat to their bottom line. In a matter of weeks, DG has dropped 22%. Although DLTR stock has yet to see that kind of damage, it’s not too far off. Additionally, DLTR faces unique challenges different from traditional grocery stores.

As a discount dollar store, one may assume that Dollar Tree is mostly inoculated against macroeconomic headwinds. This was basically true during much of the Great Recession.

However, the price deflation creates an income effect — consumers are able to buy more goods at the same price. This also means that shoppers can buy higher quality goods that they normally couldn’t afford. With complaints rising about the health repercussions of products sold at places like DLTR, dollar stores are at higher risk for competitive losses.

The one advantage that DLTR has over many other grocery stores is long-term momentum. Shares are remarkably in positive territory, up 6% year-to-date. This is right in line with the benchmark exchange-traded fund SPDR S&P 500 ETF Trust (NYSEARCA:SPY). However, the immediate upside potential has surely been stunted as everyone in the sector is reeling from the Sprouts’ disclosure.

Usually, you can count on DLTR to deliver the goods, rain or shine. But even the best of us need a breather.

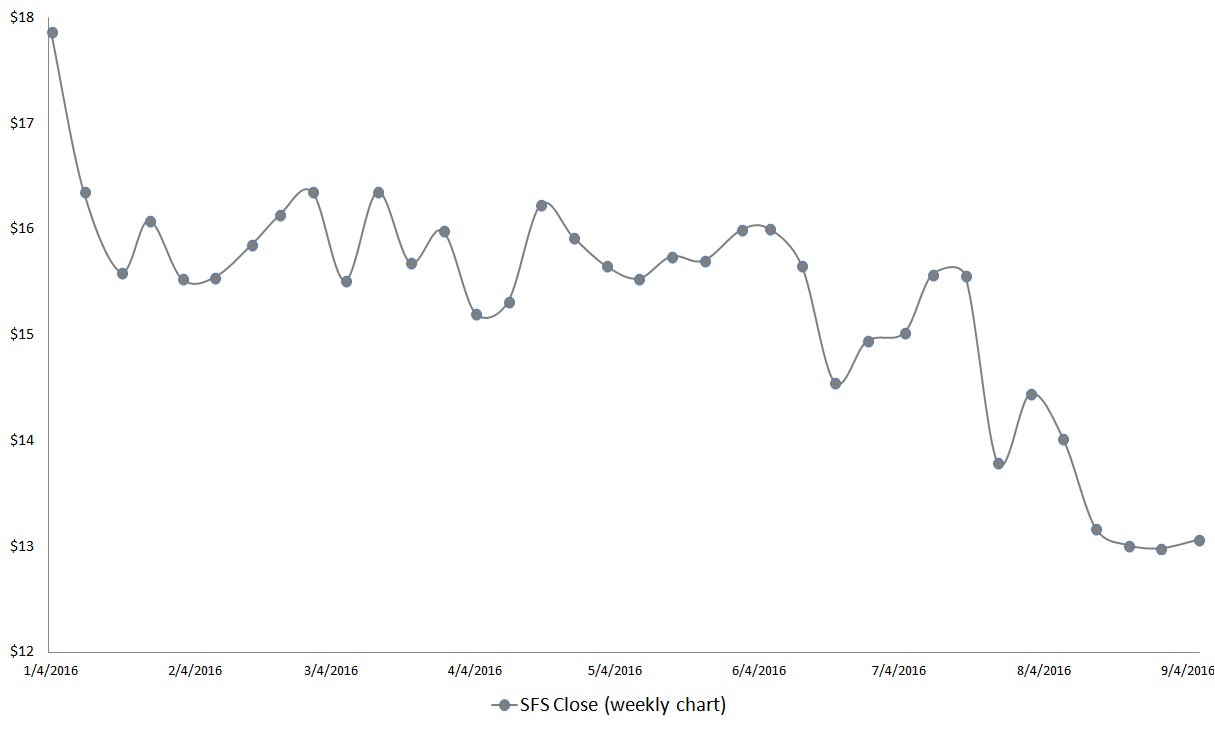

Grocery Stores You Should Leave on the Shelf: Smart & Final Stores Inc (SFS)

Click to Enlarge

Although it was the least affected by the Sprouts fallout, Smart & Final Stores Inc (NYSE:SFS) may actually be the most at risk among grocery stores. First off, their retail stores are exclusively located in the western states, with most operating in California.

Not only does that expose SFS to regional vulnerabilities, major grocery stores operate nationwide, thus creating volume challenges. More importantly, as a bulk retailer, SFS is highly sensitive to margin impacts.

That’s going to be a significant dilemma. SFS isn’t blessed with the greatest financials, and the industry headwind only amplifies this shortcoming. Most worrisome are the operating and net margins, which are well behind the median for grocery stores.

As a result, earnings performances have been disappointing this year, causing SFS to appear overvalued despite suffering severe losses in the markets. Revenue growth, while trending in the right direction, may not be enough of a driving force.

Assessing both the company and the industry, Morgan Stanley made the decision to downgrade SFS stock. It’s hard to argue against their revision. Shares are down more than 30% YTD, which is actually worse than Sprouts. Since its initial public offering in late-September of 2014, SFS has been a choppy mess. Only the brave — or the crazy — will pile into this company.

For those that don’t have money to burn, SFS is a case of too few resources, and too many problems.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.