Oil has been doing poorly lately, which has most energy stocks falling as well. OPEC recently agreed to continue its current production cap, but investors still aren’t having it. They were either looking for a larger cut in production (cutting down supply while maintaining demand to drive oil prices higher), or they believe the U.S. shale producers will continue to up their output. This would theoretically neutralize OPEC’s intention and drive oil prices lower.

However, it’s not in U.S. producers’ best interest do this. Instead, they need to steadily see demand increase. That, or take advantage of volatility in the market, agreeing to sell oil on big swings higher and curb production on declines.

Whatever the reasoning may be, the truth really comes down to price. WTI crude is down about 10.5% over the past two weeks and almost 20% from this year’s highs. That’s hurt energy stocks too, with the Energy Select Sector SPDR (ETF) (NYSEARCA:XLE) falling o.5% and more than 12% in the same time period, respectively.

So what about now? If oil prices stabilize and begin to move higher, it will boost a great number of energy equities. The bad news is, if oil continues lower, inevitably, oil stocks will go down too. But the good news is we’ve found seven solid risk-reward setups.

That is to say, we’ve found a handful of stocks that give investors a beefy reward should oil prices hold and rally. And if that doesn’t happen, these stocks are just above critical support zones and traders can cut-and-run with minimal damage. Many of these names are long-term investment worthy too, should oil prices fail to totally collapse. This gives long-term investors a way to play as well.

That’s a win-win for traders and investors alike. Let’s have a look at our seven energy stock buys.

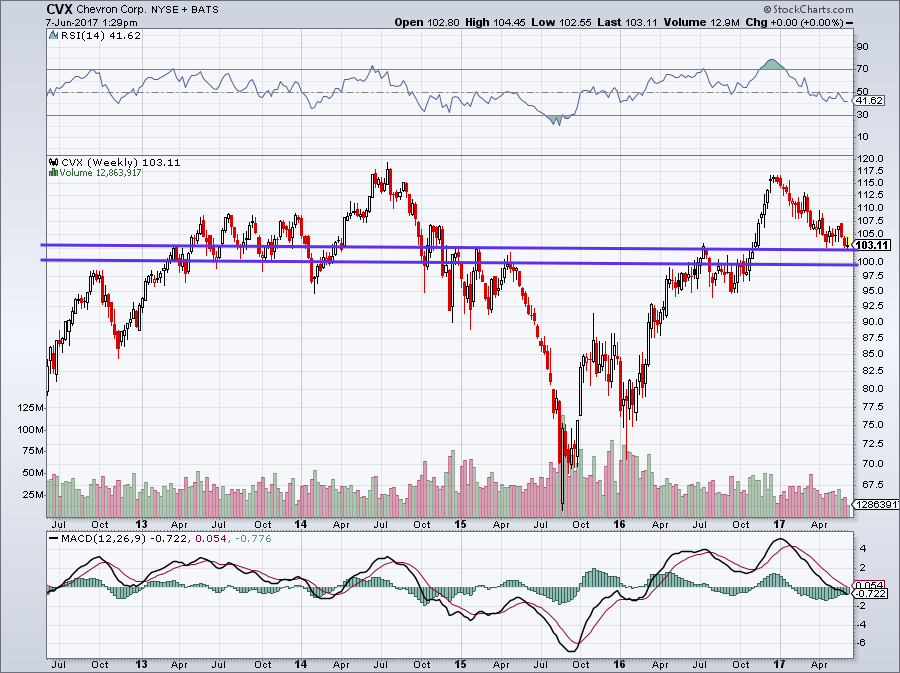

Energy Stocks to Buy: Chevron (CVX)

Click to Enlarge

Here’s an ideal candidate for a number of investors. Chevron Corporation (NYSE:CVX) is down about 10% on the year, but could certainly have some upside should oil drill down and find its mojo.

CVX stock pays out an attractive 4.1% dividend yield and has what many consider a reasonable valuation. Trading at 19x forward earnings estimates, Chevron isn’t a steal, but certainly isn’t vastly overvalued. Analysts expect sales to climb 20% this year to $137.8 billion and grow an additional 4% in 2018.

When it comes to earnings, analysts are looking for $4.33 per share this year, vastly higher than the 94 cents per share CVX had in 2016. Perhaps more encouraging is analysts’ call for $5.67 in EPS in 2018, representing growth of 32%.

As for the dividend, we touched on CVX’s attractive 4.1% yield. While Chevron’s balance sheet has been stressed in recent years, it’s one of the largest energy companies around. This gives us a bit more confidence when it comes to CVX maintaining that payout.

Regarding the stock, it may be my favorite part. The $100 to $103 level is quite significant, acting as both support and resistance in the past. This gives us a clear-cut line in the sand. Traders and investors alike can focus on this, because in either regard it gives an attractive risk/reward. Trading at $103, a move below $100 and investors can cut ties with the position. However, should oil and CVX stock trade higher, a rebound to the recent highs could be in the cards.

Just because one may be an investor doesn’t mean they can’t use proper risk/reward measurements.

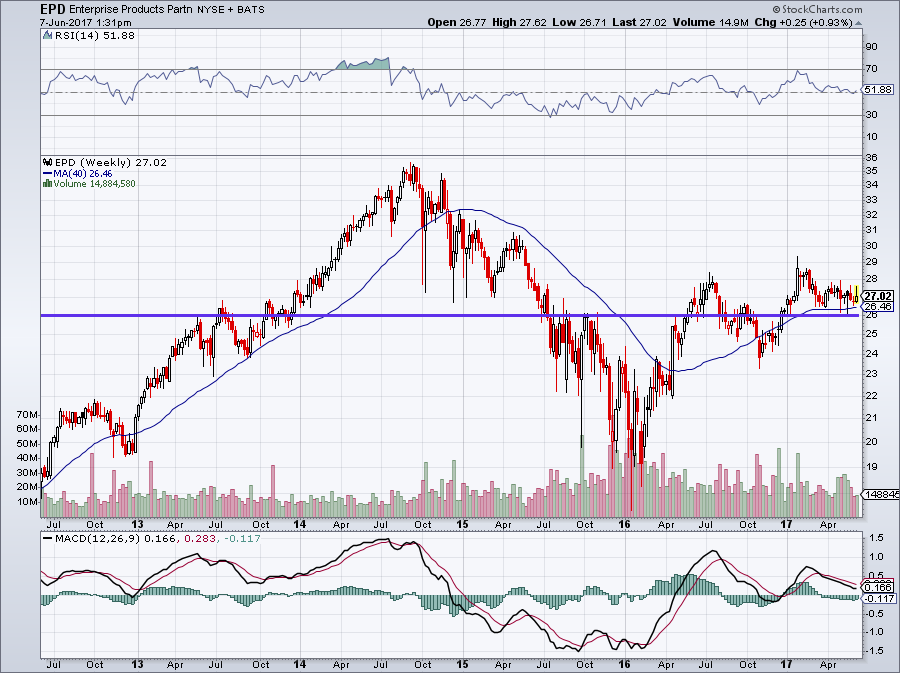

Energy Stocks to Buy: Enterprise Products Partners (EPD)

Click to Enlarge

Enterprise Products Partners L.P. (NYSE:EPD) is known as one of the more dependable, safer MLPs out there. Shares are flat on the year and down 5% over the past three months, but still boast a near-10% gain since the election.

The added kicker here is the 6.1% dividend yield, which is especially lucrative for income investors. Even if the stock turns out a flat performance for the year, the return is still pretty good by most standards.

So why go with EPD? First, its dividend is consistent. EPD has raised its dividend every quarter but one over the past 10 years. Keep in mind, this includes the Great Recession in 2007-08 and the oil crash of 2015. Despite these events though, EPD kept upping the payout.

Analysts expect 18.5% sales growth this year to go along with 18.3% earnings growth. 12% EPS growth and 7.6% EPS growth in 2018 are also attractive.

Furthermore, EPD operates in an environment going through deregulation. This will allow the company to push through lucrative deals with less hassle and hurdles. Expanding its business is key to keeping investors happy and will allow EPD to grow its dividend.

On the charts, EPD looks okay too, with solid support near $26. The 40-day moving average is also around $26.40 — a level that EPD stock has bounced from twice in the past month. If oil can stabilize, so too will EPD.

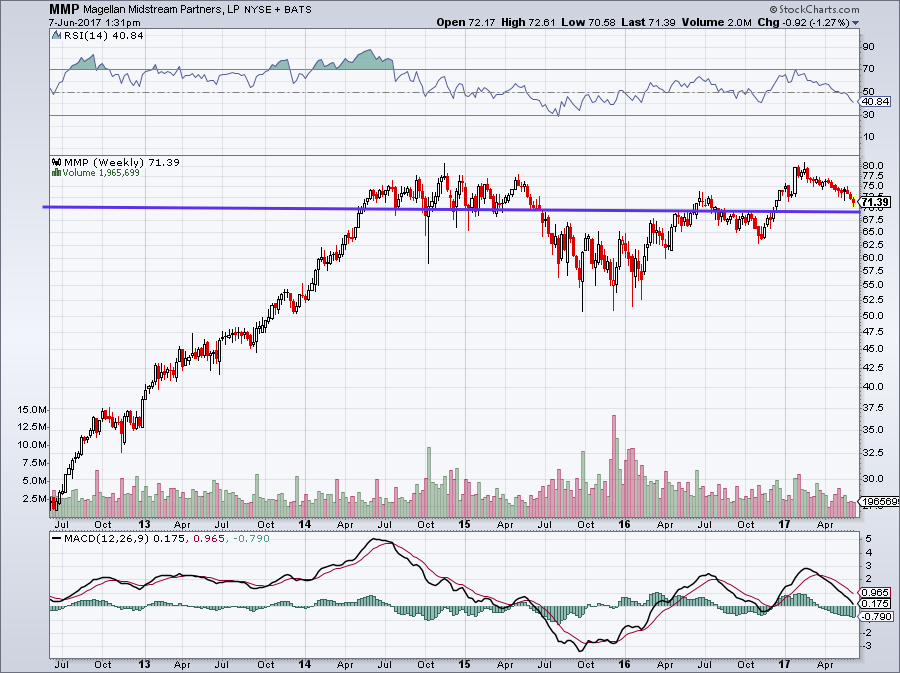

Energy Stocks to Buy: Magellan Midstream (MMP)

Click to Enlarge

Another stud when it comes to MLPs? How about Magellan Midstream Partners, L.P. (NYSE:MMP). MMP stock hasn’t wowed investors this year, down about 5% in 2017. It also pays of a dividend yield of “just” 4.9%. So what is there to like?

Let’s consider that this is one of the safer names in the MLP space. Combined with its near-5% dividend yield, it’s an attractive asset for income investors. Dependability also goes far with these investors, who should look no further than MMP. The company has raised its dividend in 35 of the previous 40 quarters.

Additionally, MMP has increased its payout by more than 70% since the first payout of 2013. That’s a notable increase in just a few years — imagine getting that kind of raise at your day job!

After rallying from $65 to $82 between the election and late January, MMP stock has cooled off. Currently trading in the low $70s, most longer-term investors would agree that current levels are good for accumulation.

Further, our pro-pipeline president surely bodes well for companies like MMP and EPD moving forward. Geopolitical tension in the Middle East could also help spark energy stocks higher. If supply takes a dip as a result and oil prices move higher in response, U.S. producers will jump at the chance to increase production. That bodes well for pipeline companies, which will get paid to move more of the commodity.

For short-term investors and traders, MMP stock offers positives as well. Roughly $70 has been a big level of support. If this level refuses to hold as support, they can cut and run, booking only small losses.

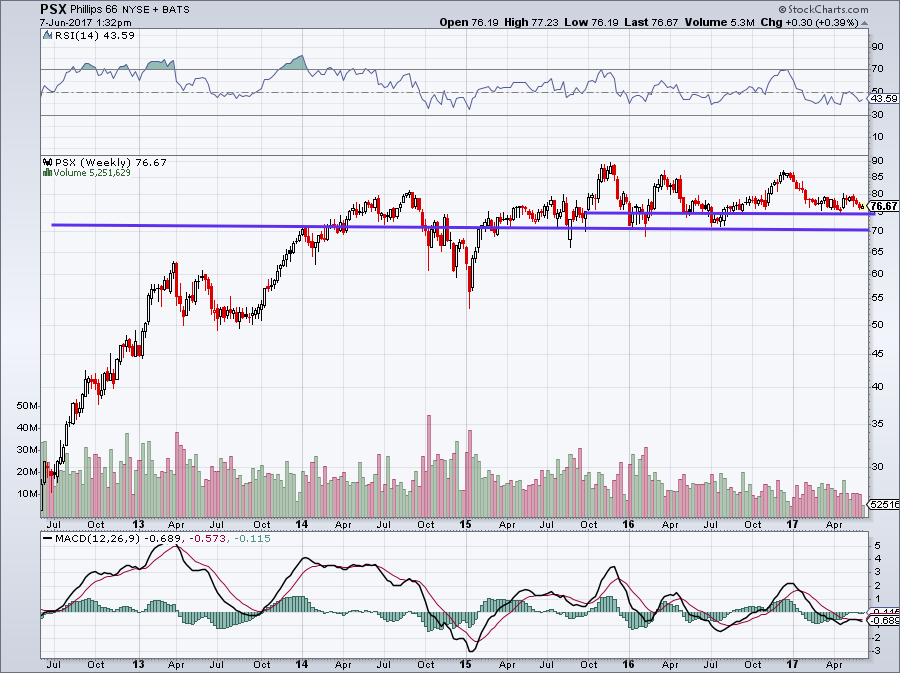

Energy Stocks to Buy: Phillips 66 (PSX)

Click to Enlarge

Is Phillips 66 (NYSE:PSX) the best energy stock to buy right now? It very well might be — and Buffett is in that camp too. With shares down 8% this year and 2% over the past 12 months, investors can get in at a bargain.

This year’s slide is sort of an anomaly. Although the energy sector has been widely volatile over the past few years, PSX has been the complete opposite. Even with the epic oil collapse of 2015, shares are actually up about 9% since the start of 2015. That in itself — the lack of volatility — is a reason to consider buying.

Phillips 66 also pays a 3.5% dividend yield, which has increased 40% since the first quarter of 2015.

Perhaps even better is the valuation. PSX stock trades at just 12.8x forward earnings, which analysts think will be $4.35 per share in 2017. This is up 54% from last year’s earnings per share of $2.82. Even better, earnings are forecast to grow another 43% in 2018. For sales, they expect nearly 30% growth this year and about flat growth in 2018.

In short, the valuation is attractive, growth is great and the dividend is big.

For traders in PSX, it would be constructive to see the $76 level hold as support. If it does, and PSX stock can clear the 200-day moving average around $80, its highs on the year could be the next target.

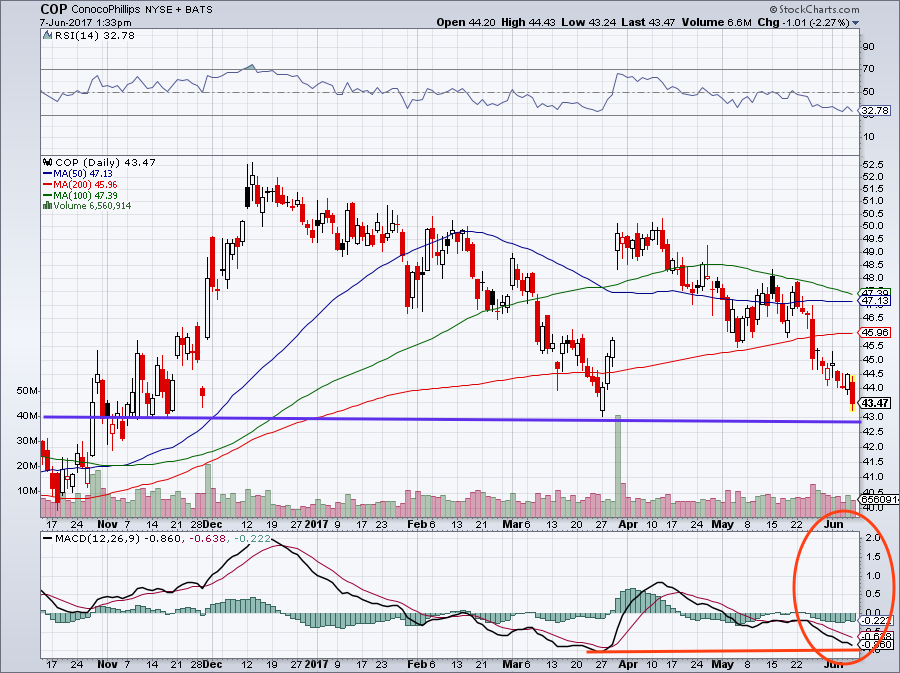

Energy Stocks to Buy: ConocoPhillips (COP)

Click to Enlarge

ConocoPhillips (NYSE:COP) didn’t have the best earnings results last quarter. A loss of two cents per share came in below expectations as traders have been waiting for a turn in the business. With just a 2.4% yield and total debt of more than $26 billion, why should investors think about COP?

This $55 billion oil company has been around for ages and it will remain that way for decades to come. Although Conoco is having trouble making the turn, it won’t be that way forever. It costs COP about $36 to produce a barrel of oil. With oil prices in the mid-$40s, Conoco has an advantage and should quickly return to profitability. After losing $2.66 per share last year, analysts expect COP to earn 53 cents per share in 2017 and $1.96 in 2018.

Are these estimates too high? That would be one legitimate concern. After 19% revenue growth in 2017 and flat growth in 2018, some may be wondering if ConocoPhillips has what it takes to deliver. For income investors, COP’s focus on its buyback more than its dividend may also be a turnoff.

However, for investors who can look past these obstacles and focus on COP’s longevity, there could be value — especially as the company returns to profitability and puts more focus in lucrative areas like the Permian Basin.

The charts have some positives too. Momentum (orange circle) looks like it could be bottoming. Second, there’s support near $43. For conservative traders, buying on a pullback at this level seems most prudent. For more aggressive traders, they could buy near current levels. Both traders can use a stop loss below $43.

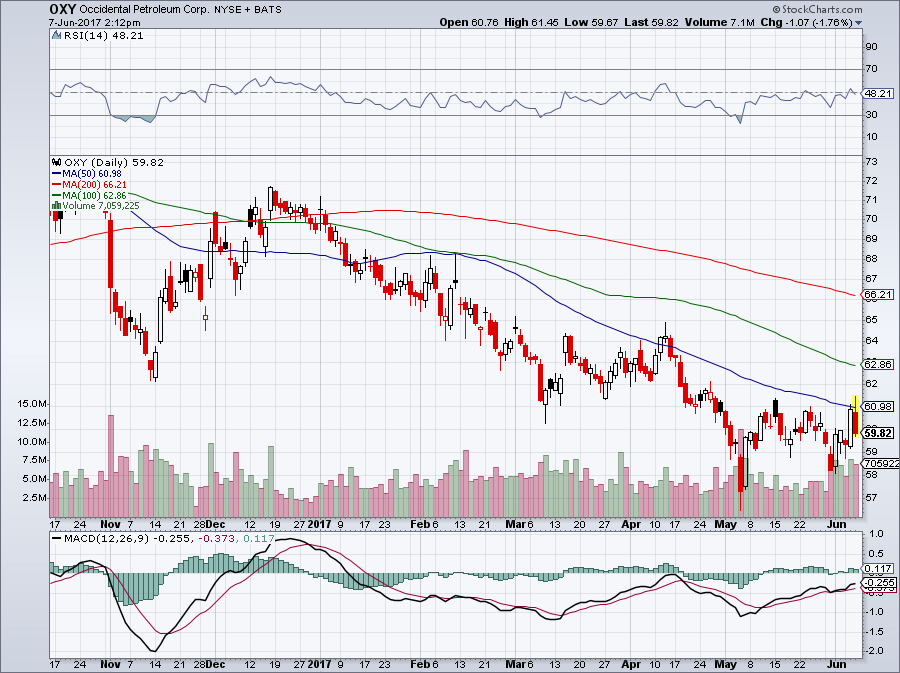

Energy Stocks to Buy: Occidental Petroleum (OXY)

Click to Enlarge

Occidental Petroleum Corporation (NYSE:OXY) popped 2.6% Tuesday, but has been a total dud in 2017, down 14.4%. However, before we dig into the fundamentals a little bit, let’s start with the chart.

On the five-year weekly, we can see that OXY has significant support around the $60 level. Additionally, MACD momentum (orange circle) is now positive. This is an important development, as it took more than five months to get to this point. Additionally, positive momentum coming as the stock is at key support is quite constructive.

On the short-term chart though, we can see that OXY has had trouble clearing the 50-day moving average. Should it do so, it could spark a rally, perhaps up to its 200-day average near $67.

Click to Enlarge

Now for the fundamentals. Occidental trades with a high earnings valuation, trading at 36x forward estimates. If the company were wildly profitable, that would help. Instead, it’s only moderately so. Analysts expect earnings per share of $1.01 in 2017 and $1.69 in 2018. That’s quite good, just not great.

While the valuation isn’t overwhelmingly bullish, there are certainly other positives. First, OXY has a lot of production in the Permian Basin, which has low production costs and plenty of oil. OXY should have plenty of room to increase production.

Finally, Occidental pays out a sweet 5% dividend yield. Conservative investors can buy the stock near current levels and use a 5% stop-loss as a cushion. Hopefully OXY will hold support and rally. Otherwise, it fall and break below the stop-loss, triggering a minimal loss.

Energy Stocks to Buy: Schlumberger (SLB)

Click to Enlarge

Schlumberger Limited. (NYSE:SLB) management has been persistently non-bullish on oil prices. It’s good that management is seemingly looking at the situation with a glass half empty approach. When oil has been decimated like it has, sometimes it’s better to have management that’s not overly bullish and going to put the company in harm’s way.

This can backfire, though, if management isn’t positive enough when things start to improve. In any regard, oil prices have been disappointing lately and that gives us more faith in SLB’s management.

For the stock, SLB is one of the few energy companies that had decent profit in 2016. Earning $1.14 per share was good, but analysts expect earnings to grow a robust 30% this year to $1.48. From there, forecasts call for 100% growth to nearly $3 in EPS in 2018.

Five-year outlooks seem foolish in the energy sector, but for SLB, analysts call for 54% annual earnings growth. On the sales front, expectations call for 8.4% growth this year and 19.4% in 2018.

All of this for 23.4x forward earnings isn’t cheap, but it makes a whole lot of its peers look expensive. Additionally, SLB pays a 2.9% dividend yield. When it comes to support, the $67 to $69 level is an important one. Should it a hold, a rebound could eventually send SLB back to this year’s highs of $87. In either regard, a slight bounce in combination with the dividend gives investors potential for a solid reward. With a stop-loss just below support, investors have a low risk/high reward setup on their hands.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a long position in MMP and SLB.