Like most of tech, Amazon (NASDAQ:AMZN) hasn’t been an exception to the beating in the stock market. While it was one of the top-performing large cap stocks in 2018, the last few months have been anything but encouraging for Amazon stock.

Long-term investors are still enjoying 2018’s 34% gain in AMZN, but that’s roughly a 50% decline from just a few months ago. During the onslaught, there have been very few places to hide in the market.

In tech stocks specifically, almost every stock has come under pressure. Even names like Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) and Apple (NASDAQ:AAPL), which have strong balance sheets and cash flow, have felt the pinch.

For a number of stocks (including the three above) it becomes a question of when to buy, not if long-term investors should buy. Just because the stock market is under pressure, let’s not forget that these are blue-chip names in the sector.

To help answer that question, we look to the charts. With Amazon stock, there is a bit of hope. While “hope” itself is not a sound investing strategy, bulls can base their decisions around a measured risk/reward setup.

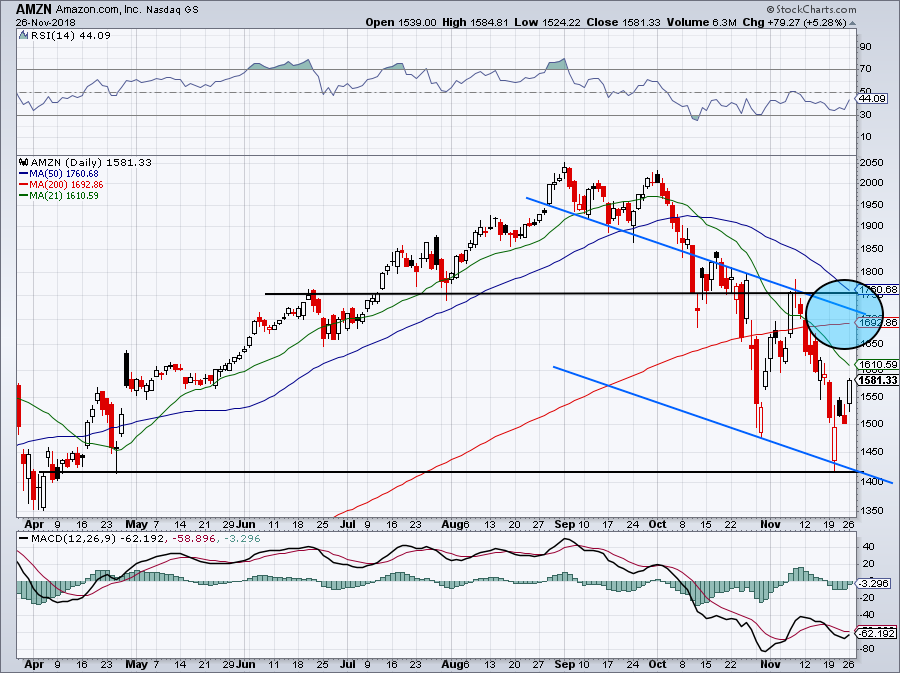

Trading Amazon Stock

Click to Enlarge

It’s too early to tell if Amazon stock has put in a “Black Friday” bottom, but after last week’s action, it’s possible. I say “Black Friday bottom” because even though the action came to life earlier in the week, Tuesday to be exact, the action leading into what is Amazon’s strongest stretch for e-commerce sales has been downright brutal.

After a post-earnings flop in late-October, shares put in a low near $1,475, climbed north of the 200-day moving average and topped out near $1,750. November gave no reprieve though, with AMZN stock declining hard and taking out that October low.

Shares put in a low near $1,425 this month before reversing and closing near $1,500. But enough of the history lessons. Where to from here?

Amazon stock is now roughly in the middle of this downtrend channel (blue lines). From here, we need to see if the 21-day moving average keeps pressure on Amazon stock and pushes it back down to its sub-$1,500 lows.

If it doesn’t, look for a rally up toward the 200-day moving average and the top of the channel (blue circle). A rally to the $1,700 to $1,750 range is possible without bulls being out of the woods yet.

If shares were to pull back, but not take out the November low, that would be constructive action for the bulls. At this point though, we’re basically observing AMZN to see which path will develop. If it can put in some constructive action for the bulls, this month’s low may prove to be the bottom.

Sizing up Amazon Stock

So why should investors be bullish on Amazon stock in the first place? It has a higher valuation than both Apple and Google, and even though its cloud business trumps that of Microsoft (NASDAQ:MSFT), the latter has a stronger balance sheet and a lower valuation.

All of that may be true, but Amazon has growth that all of the above companies surely are envious of.

For starters, Amazon has its ecommerce arm. The Black Friday through Cyber Monday sales numbers are monstrous. Adobe (NASDAQ:ADBE) Analytics had forecast a robust season, with $7.8 billion in sales expected for Cyber Monday. The total came in even higher, at $7.9 billion. That came following record online sales over the four prior days as well.

While companies like Walmart (NYSE:WMT) and Target (NYSE:TGT) are upping their ecommerce game, Amazon is the undisputed leader of the pack. As more retail sales shift online and to mobile, Amazon is a clear winner.

Beyond that, its Amazon Web Services (AWS) division remains red hot, helping to bolster the company’s overall financials. AWS is a market-share leader, holding Microsoft and Google to No. 2 and No. 3, respectively.

Its advertising business is robust as well, while its Prime membership has more than 100 million members. While not all pay $150 apiece, we’re talking about a company collecting somewhere in the $11 billion to $13 billion range in subscription fees. That equates to some serious cash flow.

Its valuation isn’t cheap, but then again, it never has been.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AMZN, GOOGL and AAPL.