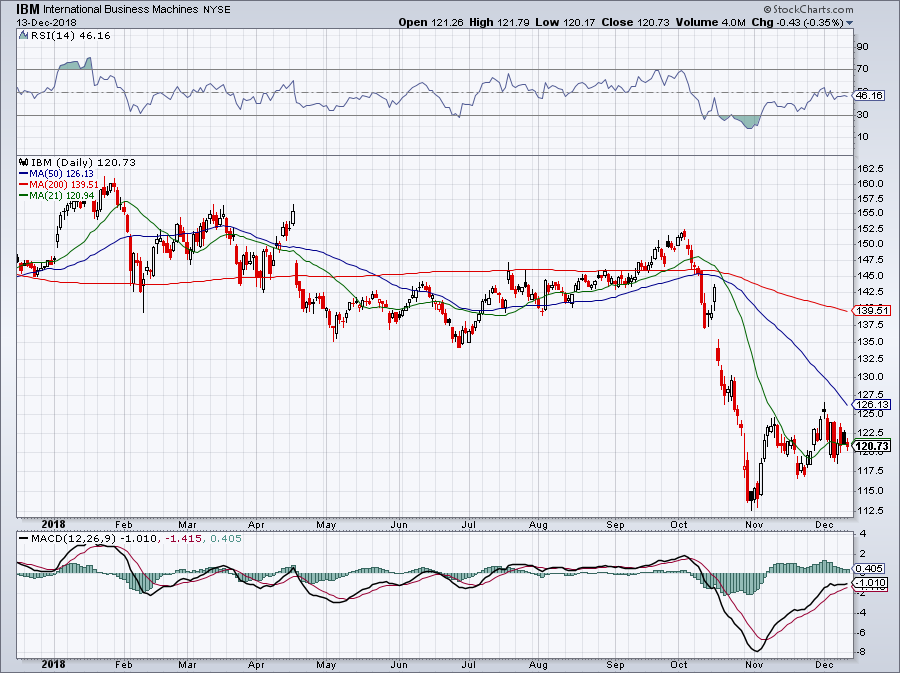

Shares of IBM (NYSE:IBM) are cheap, have a big yield and are rebounding off the lows. So why then are we opting to look at other names over IBM stock?

The fact of the matter is, IBM isn’t a great company. It’s not the one that I want to invest my money in, certainly at a time where the market’s have been increasingly more volatile. I would rather plow my funds into high-quality stocks with strong growth, free cash flow and balance sheets. In fact, we recently took a look at seven stocks with the strongest balance sheets — perfect during a time like this.

Click to Enlarge

For a quick look at its numbers, analysts expect just 1% earnings growth this year and 1% earnings growth next year. For revenue, expectations call for 0.7% growth and -0.4% growth in 2018 and 2019, respectively. These are some pitiful numbers, even if the stock does trade at just 9 times earnings.

Even after IBM’s massive purchase of Red Hat (NYSE:RHT), there are still names I like more. If we were talking IBM stock down near these levels but without a major market correction, perhaps it would be a different story. But there are simply too many attractive choices to allocate funds to rather than IBM stock.

So what are they?

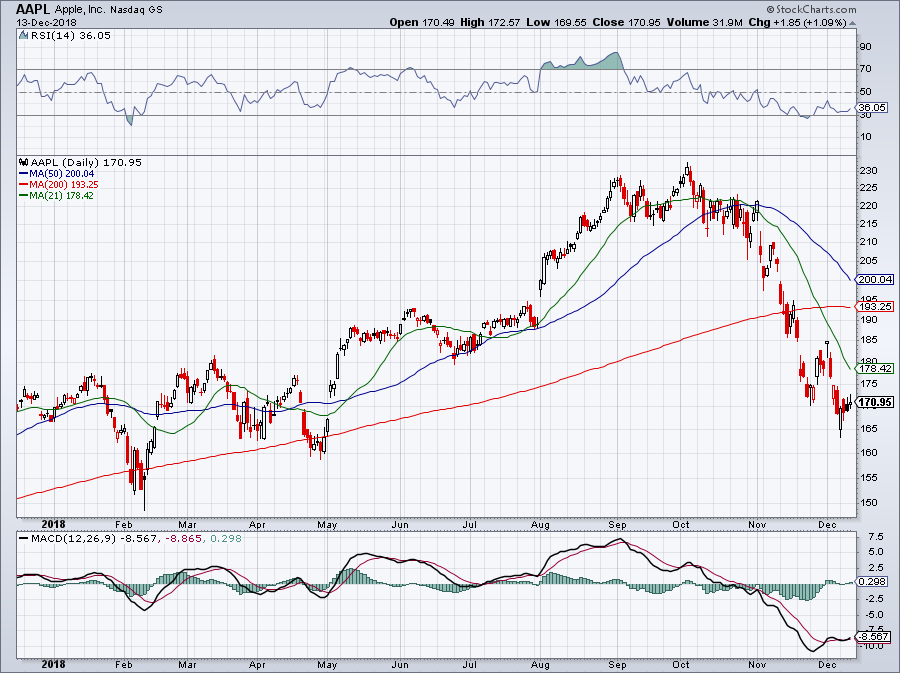

Apple vs. IBM Stock

Click to Enlarge

How is this one even a comparison? The Oracle of Omaha Warren Buffett dumped his IBM stake and has poured billions into Apple (NASDAQ:AAPL) instead. Buffett’s no dummy, right? Right.

Apple has a massive balance sheet, is repurchasing billions of dollars of its stock and has impressive growth. Last year, it generated more than $64 billion in free cash flow. Do investors even realize what a sum like that does to your business?

So there’s been some short-term noise around iPhone supply chains and demand for the new devices. If only we had seen these kinds of headlines before! Whether Apple is having some issues or not, we won’t know until it reports its quarterly results in January.

But we know plenty of other things. For starters, we know Apple makes billions per year from iPhone sales. If that number shifts around a bit, it doesn’t make Apple a sell. Its massive cash flows will keep being plowed into buybacks and elevate its earnings per share. But on top of that, its Services unit is now churning out $10 billion worth of high-margin revenue per quarter.

Shares are roughly $60 off the highs and I wouldn’t hesitate for even a second to buy this over IBM.

Alphabet vs. IBM Stock

Click to Enlarge

Another name to buy on a discount is Alphabet (NASDAQ:

GOOG, NASDAQ:GOOGL). Many investors focus on the company’s wide moats and excellent assets. Segments like YouTube.com, Google.com, Waymo, Android and the cloud are major drivers for the company.

As a result, investors can count on near-20% sales growth over at least the next two years. Earnings growth remains impressive too, with expectations calling for roughly 30% growth this year and 13% growth in 2019. Given its growth profile, many feel that 25 times this year’s earnings is a reasonable valuation to pay for such a blue-chip technology company.

Adding to that, how many investors realize the balance sheet power of GOOGL? It is in fact, one of the strongest companies in that regard.

With $106 billion in cash and less than $4 billion in debt, GOOGL has enough “dry powder” to do just about anything it wants. That type of cash also protects the company amid an economic downturn.

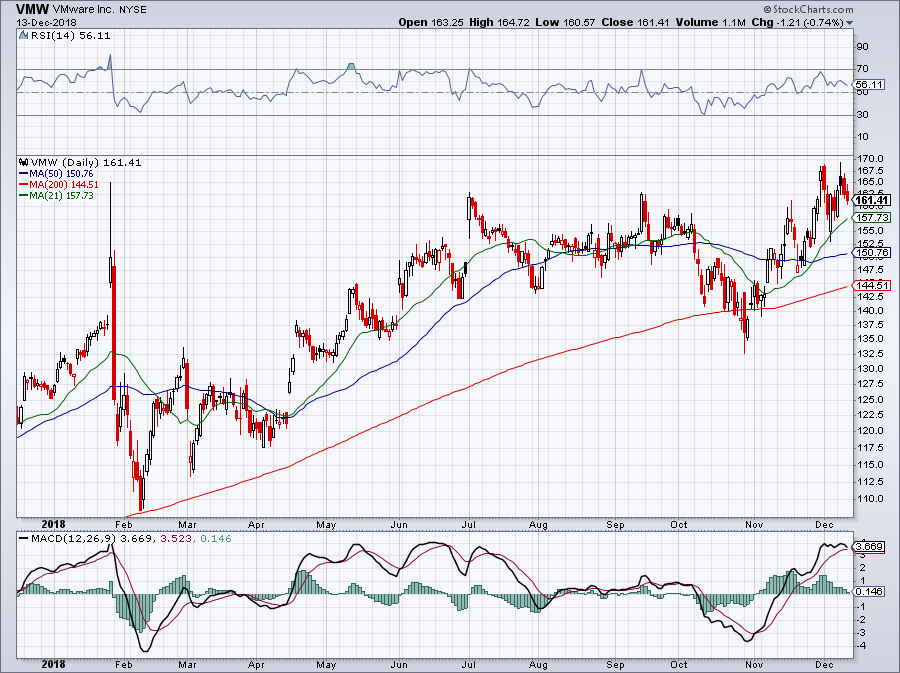

VMware vs. IBM Stock

Click to Enlarge

Last but not least is VMware (NYSE:VMW). Investors who want exposure to the cloud but don’t feel comfortable paying the premiums demanded by stocks like Salesforce (NYSE:CRM), Splunk (NASDAQ:SPLK) and Work Day (NASDAQ:WDAY), VMW is a perfect alternative.

The stock trades at 25 times earnings, which isn’t cheap necessarily, but it’s among the cheapest in the group. It doesn’t pay a dividend, but did just approve a one-time $11 billion special dividend. Considering its size — trading with a $66 billion market cap — this is a massive payout. The payout comes as part of the Dell (NYSE:DVMT) tracking stock buyout.

Beyond that though, growth remains quite solid at VMW. Analysts expect revenue to grow 12% this year and 11.5% in 2019. On the earnings front, estimates call for 20% growth this year and 7.5% growth next year.

Sure beats the numbers out of IBM, right? Even though IBM is cheap, it’s cheap for a reason. If I want a high yield and low valuation, I’ll stick with high-quality REITs or telecom stocks. When I look to tech, I want growth and investors don’t get it with IBM.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AAPL and GOOGL.