Shares of Facebook (NASDAQ:FB) have been through a long 12 months. Facebook stock came surging into its July 2018 earnings report, only for management to drop the hammer on investors’ expectations. Spending would increase dramatically and fixing some of the platform’s issues were priority No. 1, not profits.

We’re approaching one year since that earnings call, with investors wondering if history is bound to repeat itself.

The quarter could be disappointing and cause a selloff. But I don’t expect management to come out with such a downbeat and negative tone like they did last year. Does that make it a buy? Not necessarily, although FB stock is certainly worth a deeper look.

Trading FB Stock

Click to Enlarge

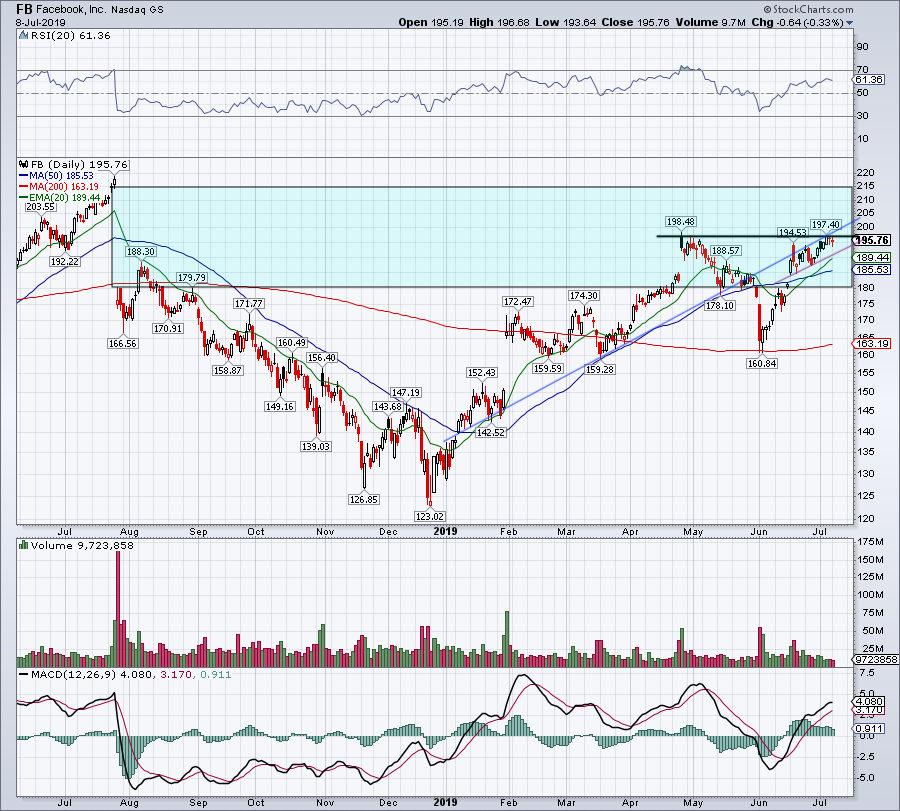

As you can see, almost a year ago Facebook stock gapped down from ~$215 to $180 in a single day. The 16% haircut dealt a crushing blow to investors, who had come to expect strong top- and bottom-line growth from the social media star.

Short of a dead-cat bounce in August 2018, FB stock stayed below this $180 gap-down level for months before re-entering this zone in April of this year. With shares consolidating just under $200, Facebook stock appears to be “filling the gap.” To complete the move, it requires a run up to $215.

Perhaps we will see that price action play out as bitcoin heats up and drives FB stock higher thanks to its Libra cryptocurrency. Maybe earnings optimism heats up and drives FB higher. The opposite action — poor bitcoin performance and pre-earnings worry — is possible too.

So where does that leave FB? For longs, they want to see a move over $197.50 resistance (black line). It would help if Facebook also hurdles prior uptrend support (blue line), meaning a rally north of $200. That could cause a squeeze to fill the gap.

On the downside, I want to see the uptrending 20-day moving average hold as support. That would keep the short-term trend intact and give bulls a bit more ammunition to take Facebook stock through resistance. Below that and the 50-day is in play. Both moving averages have played a strong role in the stock’s action over the past year.

Worth noting is that FB reports earnings on July 24th.

Valuing Facebook Stock

Facebook’s valuation is actually somewhat reasonable, with shares trading at roughly 27.5 times earnings. That’s not too bad for a company that connects a few billion people on earth, is one of the most popular websites in the world and has arguably the most efficient advertising platform of the digital era.

That said, because of some big-time spending, earnings are feeling the heat this year. Earnings estimates call for a 6.2% year-over-year decline to $7.10 per share for fiscal 2019. That’s a big haircut for investors that were used to strong double-digit earnings growth.

In 2020 though, estimates call for a 32% rebound to $9.36 per share. That leaves FB stock trading at less than 21 times forward earnings. On the revenue front, estimates call for 24.3% growth this year and 21.3% growth next year. Both figures represent strong growth, which is no surprise given the strength in digital advertising.

FB vs. FANG

Like Facebook, Alphabet (NASDAQ:GOOGL, NASDAQ:

GOOG) is going through a miniature earnings recession too, with estimates technically calling for just 4% growth this year. That doesn’t really tell the whole story (with the EU fine for instance) but we’re talking about FB, not GOOGL.

The point is, the two trade with similar valuations and both have very strong balance sheets. However, FB does have better growth forecasts in 2020. When compared to Amazon (NASDAQ:AMZN) and Netflix (NASDAQ:NFLX), Facebook has a far more attractive valuation. Further, it bests Amazon when it comes to revenue growth as well.

I’m not saying FB is better than any of its FANG counterparts necessarily, they all bring something unique to the table. I am saying Facebook stock is not drastically worse than the others, yet has been overlooked. The same goes for Alibaba (NYSE:BABA).

Simply put, FB is a profit machine.

The company sports trailing gross and operating margins of 82.6% and 38.6%, respectively. The latter has come down considerably over the past year, but is almost double the 23% that GOOGL sports. And it’s far more than the single-digit percentages that NFLX and AMZN have. That said, AMZN and GOOGL generate more cash flow than FB.

I wouldn’t bet my life savings on Facebook stock, but it’s at least worth a look here, especially if it can clear $200.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long GOOGL and AMZN.