General Electric (NYSE:GE) just can’t seem to catch a break.

In Dec. 2018, shares flushed down to the $6 range, as investors worried about the company’s solvency.

Fast forward 15 months and GE stock is right back down to those lows.

Of course, the context of the overall market doesn’t help. In December 2018, the stock market hit its lows as investors panicked about rising interest rates. This time around, the stock market is panicking over the coronavirus and trying to weigh the coming recession.

In both cases, General Electric has suffered because investors know it doesn’t have strong financials. GE has been improving over the last 15 months but that doesn’t mean it’s a high-quality stock.

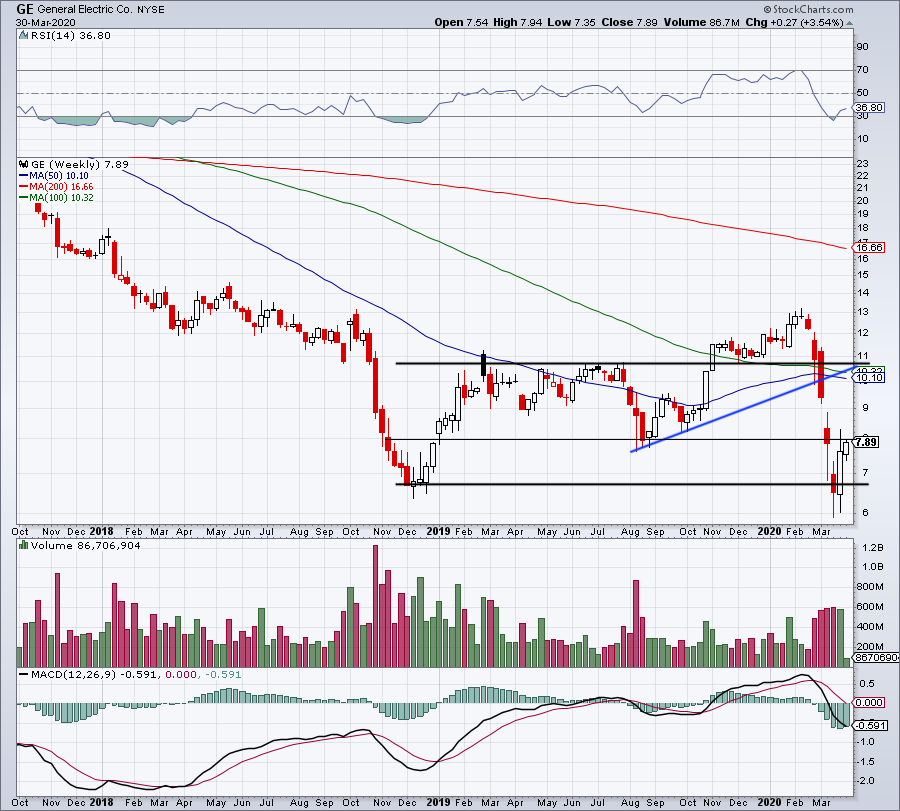

Avoiding GE Stock

Click to Enlarge

When the stock market goes through volatile panics like this, almost every stock gets hit. There are a few exceptions as a handful winning stocks show relative strength to the overall market. By and large though, it creates large discounts relative to stocks’ recent highs.

So far, the S&P 500 has fallen about 36% from peak to trough. High-quality companies may have fallen a bit less than the index — for instance, Johnson & Johnson (NYSE:JNJ) — while a number of growth stocks have fallen even further than the broader market.

However, true “junk” stocks take the brunt of it. That’s as investors dump their holdings with weak financials, knowing that they’ll struggle the most during a prolonged downturn. Carnival Cruise (NYSE:CCL), Spirit Airlines (NYSE:SAVE), General Electric and others fit that bill.

From peak to trough, GE stock fell 55.5% in just over a month. For whatever reason, these selloffs typically attract investors. They’re looking to bottom-fish, buying CCL for a big discount and hoping it posts a strong rebound. Remember, “hope” isn’t a sound investing strategy. Some investors are good at buying distressed companies. Most are not.

Instead of picking over the scraps of companies well past their glory days, why not look for companies that are still in their prime, and down 30% to 40%-plus amid the selloff?

Sizing Up General Electric

Can General Electric rebound back to $10-plus from here? Of course, but that doesn’t make it a buy.

We could look at Alphabet

(NASDAQ:GOOGL, NASDAQ:GOOG) and say that the stock is heading back to $1,500. Or Shopify (NASDAQ:SHOP) is going back to almost $600, Roku (NASDAQ:ROKU) back to $150-plus. You get the idea.

Instead of sporting strong growth and a solid balance sheet though, General Electric is struggling for flexibility. The COVID-19 outbreak isn’t helping. The company has been leaning on its aviation unit to drive its financials. For years, this was the place to be, because growth was solid and business was steady. With the coronavirus putting the squeeze on airlines right now, that’s bad news for GE.

Suddenly, prior orders are in jeopardy as airlines try to figure out the finances. It doesn’t help that Boeing (NYSE:BA) has already had so many issues relating to the 737 MAX. Slowing orders and production could crimp GE’s financials, as management was previously expecting flat-to-positive 2020 free cash flow from its aviation segment.

On March 4, management stuck to its guns, saying that it still expects $2 billion to $4 billion in industrial free cash flow for the year. That’s despite a first-quarter hit of $300 million to $500 million.

These forecasts seem aggressive. A lot has changed since March 4, and the aviation industry is not in a good spot right now. And a recession won’t help matters. That’s going to hurt business and thus, the financials for GE stock.

Bottom Line

Click to Enlarge

Like we said, it’s possible for GE stock to rebound up toward $10. But with the issues this company has faced in the past two years, along with current concerns, I find more comfort in buying high-quality companies at a discount.

Analysts currently expect General Electric’s revenue to fall 6.5% this year to $89 billion. Estimates call for an even worse decline in earnings, down 20% to 52 cents per share. Because the situation has so many unknowns though, it’s hard to trust these estimates. Even if they’re accurate, they don’t reflect a good situation.

As for the charts, look to see if GE stock can reclaim $8. Above it puts a gap-fill up toward $9.25 on the table, followed by a possible rally to $10. There it will run into several key moving averages. On the downside, watch for a break of $6.50. Below puts the recent 52-week low in play.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.