When you-know-what hits the fan, it’s best to go with quality. Luckily for bulls, Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) is among those high-quality picks. As a result, GOOG stock is up 39.7% from the recent lows and just 8% below its all-time high.

The novel coronavirus has wreaked havoc on small and large businesses — domestically and internationally. It’s rocked the healthcare world and seemingly every other industry with it. It’s forcing the globe into various states of lockdown, sending a rippling effect through governments and businesses alike.

The assumption was that as revenue dries up, so too would marketing budgets. When that happens, digital advertising spending falls, which hurts companies like Alphabet, Twitter (NYSE:TWTR), Amazon (NASDAQ:AMZN), Facebook (NASDAQ:FB

), Disney (NYSE:DIS) and a whole host of others.

Now that theory is being tested, though. When GOOG stock last reported earnings, management talked about a significant slowdown in March. However, they also said that ad spending seemed to bottom in April. Facebook’s management made similar comments.

Of course, there’s always the possibility that we see another dip in ad spending. If that’s the case, we should see a dip in GOOG stock too. But so far, the trends look promising.

Don’t Quit on Alphabet

I love Alphabet for several reasons, one of which is its balance sheet.

Total assets of $273.4 billion tower over total liabilities of $69.7 billion. Total current assets of $147 billion have a similar ratio against current liabilities, which stand at just $40.2 billion.

The real doozy is this stat though: GOOG stock has $117.2 billion in cash. Not only is that a monumental figure in and of itself, but it’s crossed against just $3.9 billion in long-term debt. Inclusive of current capital lease obligations, that figure climbs to almost $5.3 billion. But it’s a figure that Google could easily wipe away with its cash position.

Not only does that give the company incredible stability in these unprecedented times, it also gives Google flexibility. And for investors, it gives them confidence.

We’ll talk about growth forecasts in a moment, but let’s stay with the businesses right now. Alphabet has spent time (and plenty of money) diversifying its lineup. While its search and YouTube businesses remain busier than ever — and remember, these are the top-two most visited sites in the world — they do have falling ad revenue.

That is a short-term problem that looks to be rebounding as we speak. But the fact that they remain heavy traffic areas is what’s important to the long-term thesis of the business. That’s unlike many retail and other traditional businesses right now.

Further, the company’s building out its cloud unit. The segment generated revenue of $2.8 billion last quarter, up more than 50% from the same quarter a year ago. As for its self-driving car unit Waymo, the business has begun taking outside investment. While giving up a piece of its stake now, it should help shoulder the financial burden in this long-term business.

Should I Buy GOOG Stock?

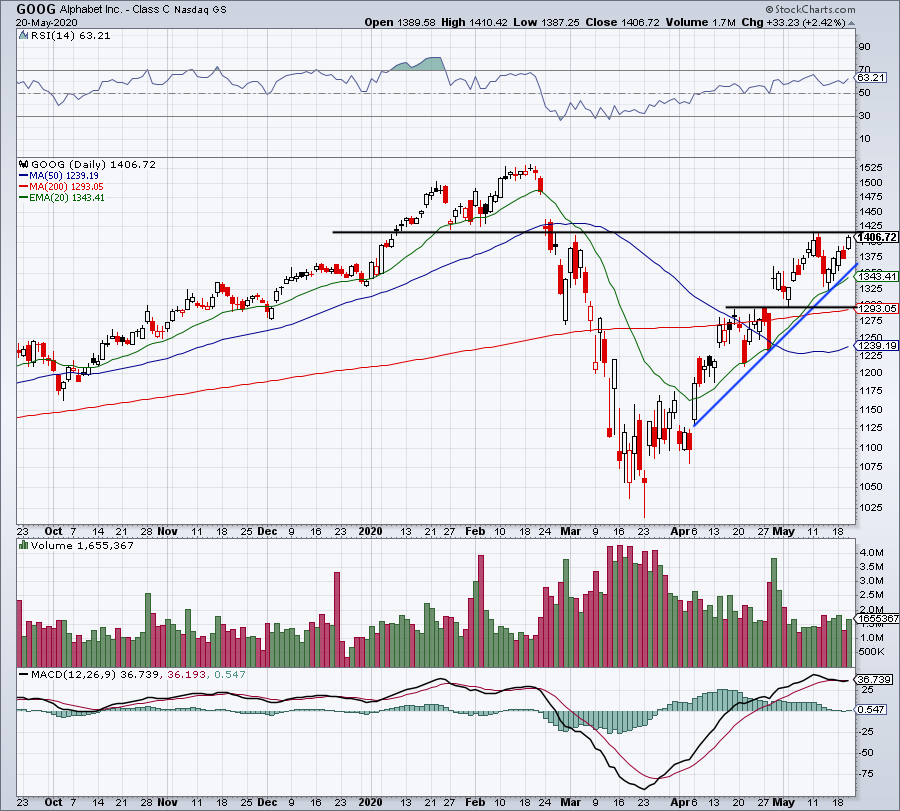

Click to Enlarge

This is where it gets a little tricky. On the one hand, Google is a very well-run company. It’s got strong financials, is diversifying its businesses and has secular growth. But right now, it doesn’t have short-term growth.

Analysts forecast revenue to grow just 4.2% this year to $168.7 billion. However, earnings are forecast to slip about 15% on the year. That’s mostly due to a 42% expected earnings drop in the current quarter.

It should come as little surprise that current estimates then call for a strong rebound in 2021. Don’t forget, the stock market is a forward-looking mechanism. While there are short-term growth issues, investors have been willing to scoop up GOOG stock provided digital ad spending really did hit a trough.

There is a small concern about overall ad spending, but long term, Alphabet will be fine.

Should we get a mild decline in the overall market, we may get a dip in GOOG stock. If that’s the case, it’s a dip to buy. Look to see if support comes into play at the 20-day moving average and uptrend support (blue line). Below that puts $1,295 in play.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.