With so much attention on COVID-19 treatment and vaccine developments, life science laboratories are getting more notice.

Alexandria Real Estate Equities (NYSE:ARE) is a real estate investment trust (REIT) based in Pasadena, California. It’s the largest landlord in the US for laboratories and related offices.

Its top companies by rent revenues include Amgen (NASDAQ:AMGN), Bristol-Myers Squibb (NYSE:BMY), Celgene, Eli Lilly (NYSE:LLY), Merck (NYSE:MRK)—which we own in Profitable Investing—Moderna (NASDAQ:MRNA), Novartis (NYSE:NVS), Pfizer (NYSE:PFE) and Sanofi (NASDAQ:SNY).

And those tenants pay. The most recent monthly rent collections were current for 99.4% of all leases. Moreover, Alexandria has 97% of its leases as triple-net.

This means nearly all of its life science tenants pay rent as well as taxes, general upkeep and insurance, which significantly reduces risks of unexpected costs and makes for a more dependable portfolio.

But it gets even better.

Over 95% of leases have locked-end annual agreed base rent escalation agreements. That means, at minimum, Alexandria has inflation and cost control protections for its longer-term leases. And these agreements don’t preclude additional rent increases as further negotiated.

Then, there is an added additional sweetener: 96% of tenant leases also come with clauses mandating additional capital expenditures (CAPEX) to the properties owned by Alexandria.

Alexandria Knows Where the Brains Are

The best and the brightest in the biotech and life sciences are not just scattered here and there. They tend to be clustered around educational and government facilities as well as around others in the “best and brightest” category. Alexandria knew this from day one in 1994, with its first major facility.

It has clustered properties for single and multiple tenants in Boston, San Francisco, New York, Seattle, San Diego and the Research Triangle in North Carolina, which ties together leading universities and science labs. It’s also in suburban Maryland, just outside of DC, thanks to the NIH and other government entities.

Now, in the current era of COVID-19, the idea of clustered properties might seem like a big problem as so many folks around the US are remote working and staying away from offices. But this is where biotech and life sciences are unique.

There isn’t really work-at-home here, as you can’t just set up a controlled environment complete with filtered air and water as well as other technologies that are mission-critical for lab work.

Even before COVID-19, the lab properties were already set up with stringent air and filter controls well above HEPA (High-Efficiency Particulate Air) and MERV-13 (Minimum Efficiency Reporting Value-13) standards. This means that the brainiacs working in Alexandria’s lab properties are likely safer at work than at home.

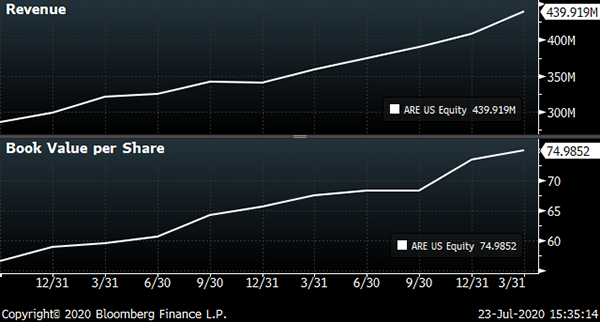

For the most recent data, Alexandria has seen revenue growth of 15.4% over the past year. This continues the trend of strong gains in sales, with the three-year average running at 18.9% on a compound annual growth rate (CAGR) basis.

Its property and other assets amounting to the company’s intrinsic (book) value continue to expand at a CAGR of nearly 12% over the past three years.

Alexandria Revenue & Book Value—Source: Bloomberg Finance, L.P.

The building of book value is quite impressive because it shows that shareholders are not just getting a higher share price, but a higher actual value in the underlying company. And with revenues gaining by an even greater pace, that means the company is able to make more from its assets at better margins.

But what shareholders really care about is the share price. And Alexandria continues to be recognized in the market.

The return over the trailing year is 24.3%, including its dividend income. That’s more than 33% better than the return of the S&P 500 and compares even better to the S&P Real Estate Index’s net loss of 0.6%.

Alexandria Real Estate Equities, S&P 500 & S&P Real Estate Indexes Total Returns—Source: Bloomberg Finance, L.P.

This outperformance is not just a recent fluke. Over the trailing five years, Alexandria has continued to out-gun the S&P 500 and S&P Real Estate Index by nearly similar margins.

Is it too pricey? Nope.

The shares are only valued now at 2.3 times book, which is lower than the shares have been valued over the past years. And it’s at a discount to the average book value of the Bloomberg US REITs Index members, even more so compared to the average book value of the S&P Real Estate Index, despite Alexandria’s continued outperformance.

The return on funds from operation (FFO), which measures just the actual return from the rental of its properties, is ample at 11.5%. That’s also better than most of its peers.

Debt is controlled at only 40.9% of overall capital of the company, and creditors are eager to buy its bonds. The company has been lowering debt costs with refinancing.

Moreover, Alexandria has been able to expand its capital for property acquisition and development with equity sales. The company has placed three share sales since June 2019 at market favorable terms that have rewarded both existing shareholders as well as buyers of all of the new shares.

The dividend yields 2.4%, which is lower than the average for the bigger REITs, but it’s well above the general market average and has been increasing in distribution by an average of 7.5% over the past three years.

To get my buy-under price and further guidance on Alexandria Real Estate Equities (NYSE:ARE), sign up to become a Profitable Investing subscriber today.

Neil George was once an all-star bond trader, but now he works morning and night to steer readers away from traps — and into safe, top-performing income investments. Neil’s new income program is a cash-generating machine…one that can help you collect $208 every day the market’s open. Neil does not have any holdings in the securities mentioned above.