This article is excerpted from Tom Yeung’s Profit & Protection newsletter dated July 19, 2022. To make sure you don’t miss any of Tom’s picks, subscribe to his mailing list here.

In 1881, the U.S. stock market suffered one of the most severe bear markets on record. By the end of the four-year pullback, shares of the US 100 index had declined by 34.6% — more than during the 2000 tech bubble (or my life expectancy when I was teaching my sister to drive).

The Panic of 1884 was a unique bear market. Railways and steelmaking dominated the U.S. economy; the market pullback directly resulted from overinvestment in capital goods in the post-Reconstruction era.

Yet Wall Street strategists consistently rely on historical data to guide their forecasts, no matter how irrelevant the figures become. Earlier this month, analysts at Deutsche Bank pointed out that historical data suggest that the market usually rallies during earnings season after a selloff.

In other words, they’re predicting a rally in August.

Meanwhile, analysts at Morgan Stanley have taken the same economic data and come to the opposite conclusion: that stocks have a further 20% to fall.

The problem is that market predictions tend to view the U.S. stock market as a single entity (often with human feelings!) — one that repeats past patterns like a commuter driving to work. S&P 500 target prices of 3,000… 5,000… 10,000… assume the stock market is a single vehicle where every passenger experiences the same ride.

The Complex Nature of Our Stock Market

We know, of course, that the S&P 500 is not a circus car with 500 clowns stuffed in it (Although I can’t say the same for the CEOs that run the firms).

Instead, markets are made up of stocks… sectors… sub-industries… that are all zigging and zagging across highway lanes like me and my sister’s driving (Apparently, it runs in the family.) In the past month alone, the energy sector has fallen by -19%, while healthcare and tech are up 4.5%.

These figures also change over time. In 1884, the rail and steel industries dominated the U.S. economic landscape. Today, they make up just 1.1% of our economy when measured by corporate revenues.

And noteworthy shifts can happen in relatively short periods. In 1993, financial companies were twice the size of tech in the S&P 500 index. By 1999, the tech bubble had made the opposite true.

Ignore these differences at your own risk. Deutsche Bank’s rosy conclusion of the economy came after a slew of bank earnings surprises — a far less significant figure today than in the pre-2008 years. And crypto’s recent turnaround comes at a time when cryptocurrencies make up a far larger share of investor wealth.

When Will Stocks Go Back Up?

Fortunately, segmenting the market can help us understand when stocks will go back up.

First, consider tech stocks — the high-growth companies driving in America’s fast lane. Today, the top 10 tech companies make up 25% of the S&P 500 index and 50% of the NASDAQ. Any market analyst would be remiss not to consider them separately.

Increasingly, these tech-focused multinationals are earning profits abroad. In 2021, Apple (AAPL) generated two-thirds of its revenues outside the U.S. Microsoft (MSFT) was close behind with one-half. A slowing domestic economy doesn’t necessarily mean bad times.

These companies are less capital-intensive than banks, industrials, rail or other market-dominating segments of the past. Rising rates only have second-order effects on the solvency of these large tech firms.

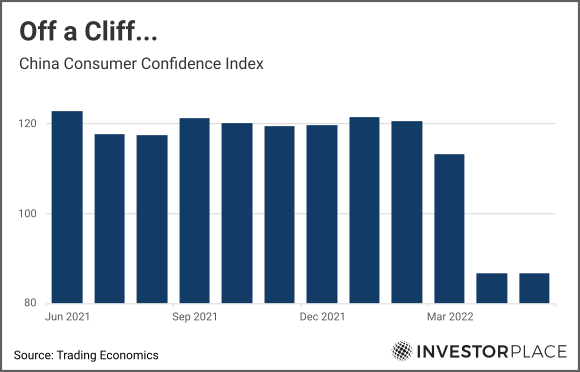

On the other hand, the 12.5% rise in the dollar index this year — combined with cratering Chinese consumer confidence — could cause a car wreck. In February, GLJ analyst Gordon Johnson noted, “Tesla’s China operations look to be much more profitable than the company’s U.S. operations.” Several city-wide lockdowns later, that may no longer be the case.

Bearish analysts at Morgan Stanley are probably right that mega-cap tech firms still have room to fall.

I’m not anticipating a full turnaround in these companies until 2023.

Then there are countercyclical, dividend, staple and other “safe-haven” stocks that make up much of the Dow Jones Index. These are the slow-and-steady firms that conservative investors tend to favor.

True to their word, many of these firms have barely registered a slowdown. Coca-Cola (KO), International Business Machines (IBM) and Merck & Co (MRK) are all up for the year.

Even Visa (V), the bellwether of consumer spending, has only dropped 3% since January. To investors in these conservative, dividend-paying companies, the question of “when will stocks go back up” has been a moot point.

It’s why the core Profit & Protection portfolio holds a healthy dose of countercyclical firms like AT&T (T), HanesBrands (HBI) and Charles Schwab (SCHW). For businesses with consistent cash flows, 2022 has been a relatively uneventful year.

To see more of these high-performing dividend picks, click here to download Tom’s latest report on 11 Dividend Stocks to Buy.

Are Tech Stocks Due For a Parabolic Breakout?

Growth stocks… Value stocks… Investors can use history to anticipate when prices of these traditional stocks will go back up.

Then there’s the third class of firms:

Moonshot companies.

These are the big bets, like Luke Lango’s OpenDoor (OPEN) and my pick Desktop Metal (DM) — game-changing startups with 5x… 10x… 50x upside. The firms don’t fit neatly into traditional categories of “growth” or “value,” but they hold incredible power to sway investor sentiment. Wherever the price of these stocks go, so too do market moods.

The issue, of course, is that early-stage firms have a limited history in the stock market. Before the 2010s, venture capital and private equity firms dominated the sector, keeping startups private for as long as they could. Only the bipartisan Jumpstart Our Business Startups (JOBS) Act of 2012 began bringing these startups to public markets.

Valuations of these companies also have little to do with their underlying performance. WeWork (WE) didn’t become a $47 billion firm on the quality of its cash flows or dividends. “Traditional” growth projections are no better; show me any venture capitalist who got rich by running DCF models or using technical analysis.

Instead, investor demand drives the market values of these risky assets.

When times are good and money is plentiful, shares of these zero-profit firms seem to levitate on their own. It should surprise no one that investors can predict 78% of Bitcoin’s changes by watching Tesla’s (TSLA) price action. And when liquidity dries up, these wagers can go to zero.

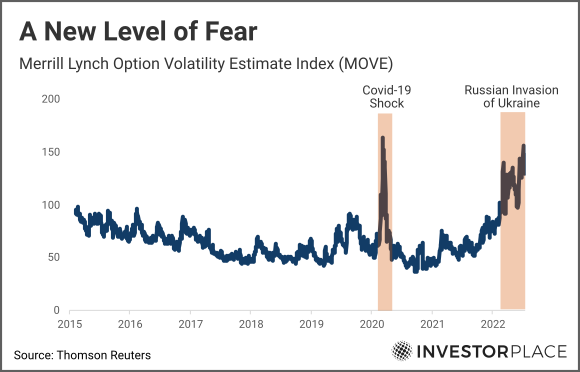

Today, markets are unfortunately showing little appetite for such bets. The Merrill Lynch Options Volatility Estimate (MOVE) — a well-regarded index of bond investor fear — has remained persistently high since Russia invaded Ukraine in February.

It’s an invaluable measure of investor sentiment — perhaps even more so than the commonly-used VIX Index (VIX) for stock volatility. Credit markets are a leading indicator for Moonshots, since zero-revenue startups depend on fundraising to stay in business. The iShares Biotechnology Index (IBB) peaked in September 2021, one full month before I said Fed Chair Jerome Powell was “ringing the bell at the top of the market.”

But the good news is that these firms will recover faster than mega-cap companies — once rate hikes start moderating. Research by Fidelity has come to similar conclusions: that interest-rate-sensitive firms are the first to recover in early-cycle turnarounds.

That means investors should anticipate a recovery in these high-risk stocks by the end of this year. The Atlanta Federal Reserve Bank estimates that rates will peak sometime between December 2022 and March 2023; demand for risky Moonshots should bottom out several months before that.

When Will Stocks Go Back Up?

The Panic of 1884 would eventually turn to a footnote of U.S. history. Less than a decade later, The Panic of 1893 would bankrupt a quarter of U.S. railroads, cause 35% unemployment in the state of New York, and even kickstart the Free Silver movement.

1907… 1929… 1945… the list of major recessions goes on.

Every dip, however, eventually returns to growth. According to the same Fidelity study, consumer discretionary and industrials are usually the first companies to benefit. These segments — which include automakers and airlines — were once the bellwether of investor sentiment.

Today, Moonshot companies have taken up that mantle. And investors looking to ride the wave back up should consider these faster-moving startups in the earliest stages of the rate-easing cycle.