Nothing is guaranteed in the market, but I have good personal conviction in several “Surefire” stocks to buy regularly. This is mostly due to how sticky their revenue and profits are, alongside their stable and consistent performance in the stock market up until now. Not only that, these stocks have also delivered solid growth and will likely keep compounding in the long run.

I think boosting your holdings in some of these seven surefire stocks is a good idea each time you get a paycheck. These businesses will likely compound your money faster than the broader market if they keep executing as they have. Let’s explore the stocks to buy regularly:

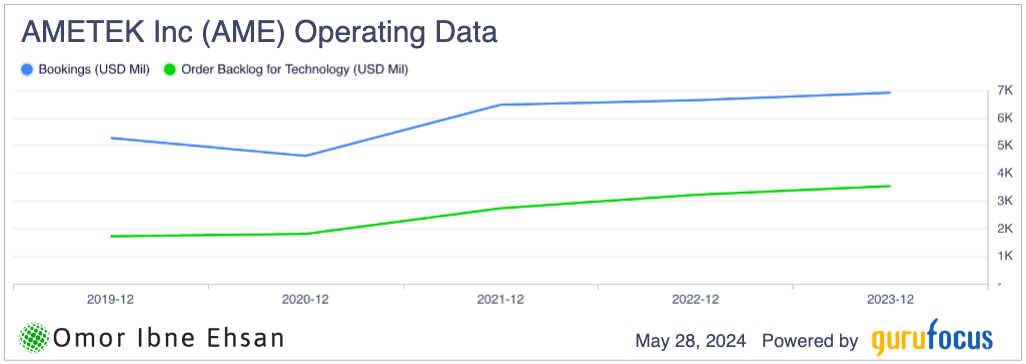

Ametek (AME)

AMETEK (NYSE:AME) is a company that makes electronic devices and electromechanical tools. Even with economic challenges, it posted decent results this earnings season. Their sales grew 9% YOY, reaching $1.74 billion. However, this actually missed estimates by 2.4%. So why am I putting this in a list of surefire stocks? It’s because Ametek still expects revenue to grow in the low double-digit percentage range for all of 2024. Besides, the company has slightly raised its earnings per share (EPS) guidance. The previous EPS guidance range was $6.70 to $6.85, and the new updated guidance range is $6.74 to $6.86. Bookings and backlog are swelling, too.

Click to Enlarge

AMETEK had a record operating income of $446 million, up 10%, with operating margins at 25.7%.

The Electronic Instruments segment did very well, with operating margins at 30.5%. This company is a cash cow with healthy growth. This positions them well to keep expanding by buying other companies, and the revenue growth in Q1 was actually driven mostly by their new acquisitions. The stock also had a correction of around 9% recently, so I think it’s a great buying opportunity right now. It also has a small 0.64% dividend yield, which makes me think it is one of the best surefire stocks to buy regularly.

Palo Alto Networks (PANW)

Palo Alto Networks (NASDAQ:PANW) is a leading cybersecurity company. The company reported strong results for the third quarter of 2024, with revenue growing 15.3% YOY to almost $2 billion, surpassing estimates by $17.86 million. EPS of $1.32 also exceeded expectations by 7 cents. The growth so far has been outstanding here.

Click to Enlarge

I believe Palo Alto Networks is well-positioned to benefit from the growing need for robust security solutions. Cyber-attacks will forever be a problem, especially with nation-state actors taking advantage of weaknesses at a large scale. These attacks are also being paired up with AI, which Palo Alto Networks specializes in through its suite of AI-focused security products. The stock has been one of the most consistent names in the AI and software field, up 382% over the past five years. The stock has dipped a little recently, but I think it presents a good entry point for the long run, as PANW has already started to bottom out.

Heico (HEI)

HEICO Corporation (NYSE:HEI) operates in the aerospace and defense industries. HEI stock has been one of the most stable and consistent stocks over the past few years. Moreover, the trend has only been better, with the stock up almost 37% in the past year.

This company has delivered very good results this earnings season. Total revenue jumped an amazing 44% YOY to $896 million, while operating income soared 39% to a new high.

They posted 12% organic growth in their Flight Support Group, driven by strong demand for replacement parts and repair services after planes land. The booming aerospace industry is nothing to scoff at. Look at how companies like FTAI Aviation (NASDAQ:FTAI) have been performing recently.

Management has done an exceptional job here–smoothly integrating recent acquisitions like Wencor–which are already paying off. With air travel picking up and steady defense spending, I believe HEICO is set up for sustained growth going forward. The stock should continue delivering consistent gains.

IDEXX Laboratories (IDXX)

IDEXX Laboratories (NASDAQ:IDXX) provides diagnostic testing and services for pets and livestock at veterinary clinics. The company reported subpar results for the first quarter due to some broader economic headwinds, with 7% growth in revenue slightly missing, though an impressive 9% EPS growth surpassed estimates. The most concerning thing was the FY24 guidance being lowered, though I do not think you should worry too much about near-term trends. The company is having ongoing success in placing premium diagnostic instruments, an 11% rise in recurring software and imaging revenue, and the ability to expand profit margins.

Click to Enlarge

While severe January weather and softer demand for veterinary appointments presented difficulties, IDEXX saw 6.5% growth in recurring U.S. diagnostic testing revenue, significantly outpacing the 2.3% drop in overall clinic visits.

I believe IDEXX remains well-positioned as a high-quality long-term investment that can produce sustainable growth and returns for shareholders, even in a more challenging overall business environment. Analysts expect both revenue and EPS growth to accelerate in 2025. Indeed, I think this is one of the most surefire stocks to buy regularly.

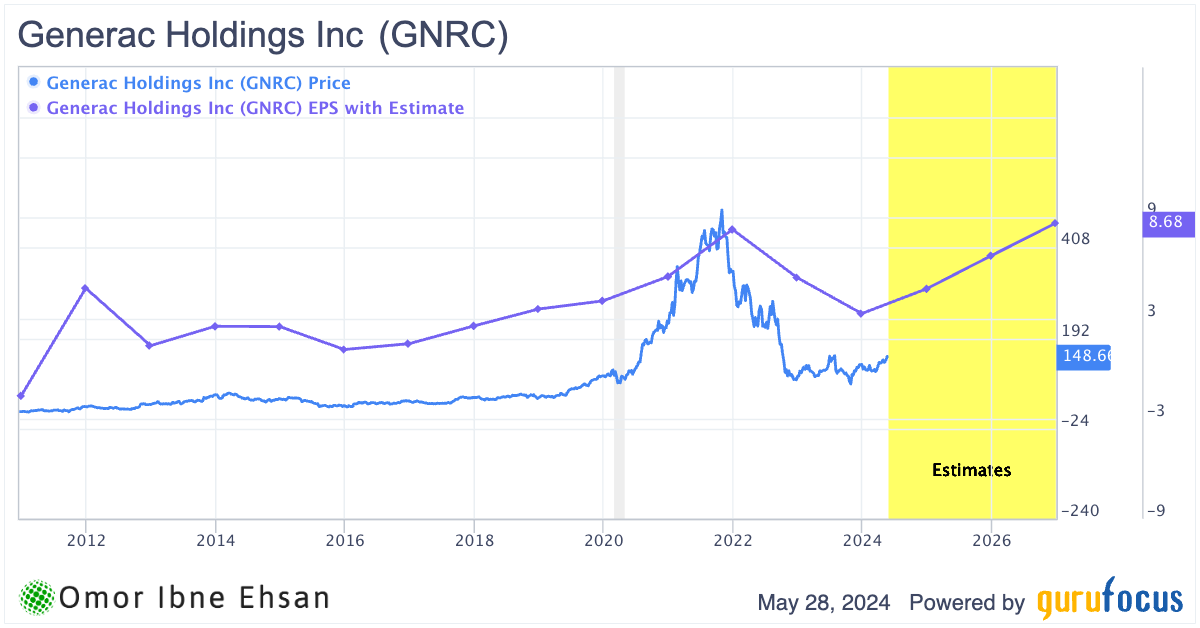

Generac Holdings (GNRC)

Generac Holdings (NYSE:GNRC) is a leading global innovator of energy technology and power product solutions. This stock has not had the best historical performance. The past few years have been very volatile, and the stock delivered explosive gains in the early post-COVID era, which were then wiped out in 2022. That said, I still think this is a surefire stock, as GNRC has been performing well since.

Q1 earnings exceeded expectations thanks to higher commercial and industrial shipments, combined with favorable input cost management. Revenue increased slightly YOY to $889 million, with residential product revenue growing 2%. However, the top line still missed estimates by $3.4 million.

While global commercial and industrial product sales dipped slightly, a robust increase in shipments to industrial distributors helped offset softness in some rental and telecom markets. Generac’s has been significantly strengthening margins and improving free cash flow. Analysts expect this trend to continue, with EPS expected to more than double in the next four years.

Click to Enlarge

Although home consultations declined from a solid prior year, they still remain well above pre-pandemic levels. With Generac making ongoing investments to engage new customer segments and expand their installer partnerships, I believe they are well-positioned to capitalize on the long-term home standby power opportunity ahead.

Monolithic Power Systems (MPWR)

Monolithic Power Systems (NASDAQ:MPWR) has built a strong business designing high-performance power solutions for its customers. I’m consistently impressed by how MPWR delivers solid results each quarter, even when the broader economy is facing uncertainty. In Q1, their revenue reached $457.9 million, which was nearly $13 million above what analysts had predicted. Their earnings per share of $2.81 also beat the forecasts by 17 cents. To me, this looks like one of the top surefire stocks to buy regularly.

While management is keeping a close eye on the potential challenges of the second half, given limited visibility, I’m encouraged by the strong engagement they continue to have across all the markets they serve. Their expanding list of design wins with new customers. MPWR is diversifying its supply chain on a global scale, which will serve it well as economic conditions eventually improve.

One area they are gaining share in is enterprise data centers, which now make up about a third of total sales. With that in mind, I believe MPWR remains a solid pick for the long run. The stock is up over 46% over the past year, which is impressive given the environment. It also comes with a 0.66% dividend yield.

Parker-Hannifin (PH)

Parker-Hannifin (NYSE:PH) is a global leader in motion and control technologies.

The company posted $5.1 billion in total sales in Q3 2024 and 1.2% organic growth. I’m especially pleased by the record adjusted operating margin of 24.7% across all segments, a full 1.5 percentage points higher than last year.

The strong demand from their aerospace business has clearly provided a significant boost, and I expect that positive momentum to carry forward. Now that management has opted to raise full-year projections, I believe Parker-Hannifin is well-equipped to deliver sustainable growth and returns for shareholders in the long run, especially due to the cash flow here.

Click to Enlarge

The dividend yield here is 1.23%. This stock is up over 60% in the past year, but you should steer clear as a near-term correction could happen after the recent rally. Regardless, it is still one of the best stocks to buy regularly for the long run.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.