If you’re already retired, you must play the investment game differently than others. Your main priority should be to protect the assets you already have while also making sure you have enough passive income coming in to make your retirement days as comfortable as possible.

First, this doesn’t mean you should put all your money into the stock market. Even the safest stocks can crash in a downturn. I think it’s wise to have a good chunk of your money in bonds. They have high yields right now; once interest rates come down, they’ll be worth even more.

Nevertheless, stocks are still essential as reinvesting dividends, and capital gains can make them compound more efficiently in the long run. Let’s examine three retirement stocks that strike the perfect balance.

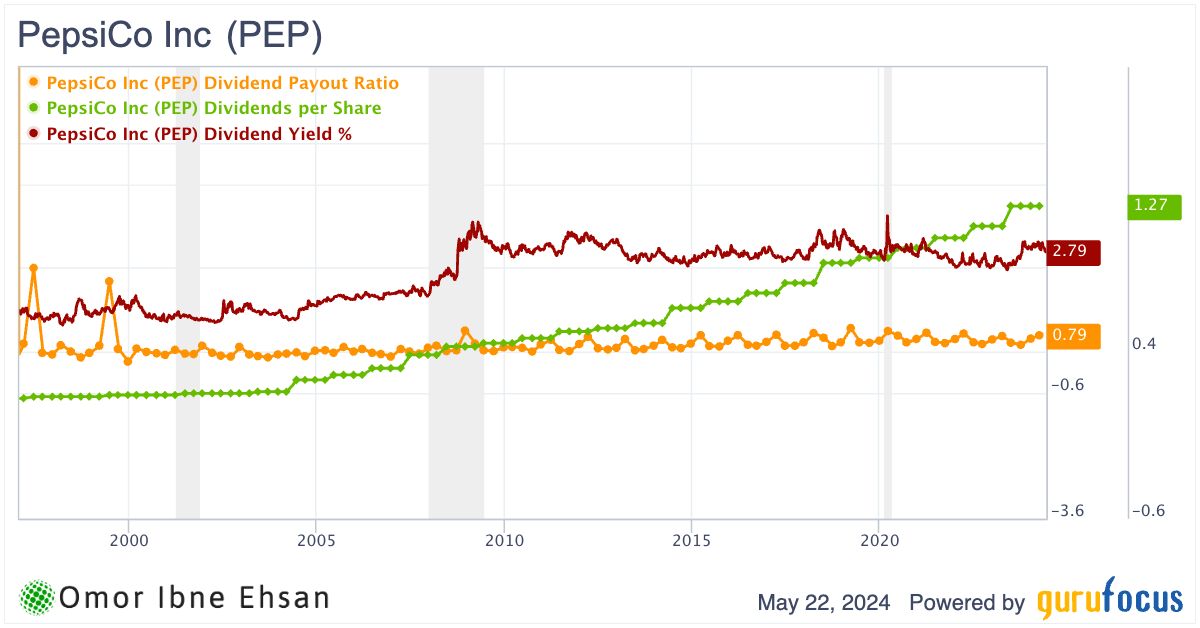

PepsiCo (PEP)

PepsiCo (NASDAQ:PEP) is by far my favorite pick when it comes to long-term dividend stocks. While it is going through some tough times right now, the stock has been very stable and consistent throughout its history. It is very hard not to be drawn into a PepsiCo product if you walk down any snack aisle.

The growth here is far from over. Its international segment continues to perform very well. The $36 billion international segment is expanding at a brisk pace while maintaining healthy profitability. I’m confident this momentum can be sustained given PepsiCo’s focus markets like China and India.

However, margins in the Frito-Lay North America business were a bit softer this reporting period. The company expects these headwinds to ease going forward. The question remains whether PepsiCo will reinvest any potential savings to drive faster top-line growth or allow it to boost margins. I believe Frito-Lay margins can return to the lower 30% range, but the timing is still uncertain.

Regardless, if you’re a retiree, the short-term trends should not matter much. This business will continue to compound in the decades ahead, and it has a solid 3% dividend yield to top it all off.

Click to Enlarge

Flowers Foods (FLO)

Flowers Foods (NYSE:FLO) is not as big as Pepsi, but the trends have been just as safe. Also, this stock is seeing some near-term weakness due to the broader economy not cooperating, but I only see this as an opportunity for the long run. The stock is already showing signs of a recovery.

There has been growth in demand for some of their branded products, especially Dave’s Killer Bread, which continues to attract more buyers each time.

Additionally, signs indicated that expenses were rising quicker than income. Higher costs for staffing and technology seem to be cutting into the bottom line more than hoped. Management aims to address this through changes and savings, but it’s an area I’ll be paying close attention to. The dividend yield is 3.8%.

On a brighter note, it looks like new prospects are being won over to Flowers Foods’ offerings faster than projected. This extra business should help maximize the use of their facilities. I also see potential in their plans to upgrade warehouses and transportation fleets. While costly at first, streamlining operations could serve them well in the long term.

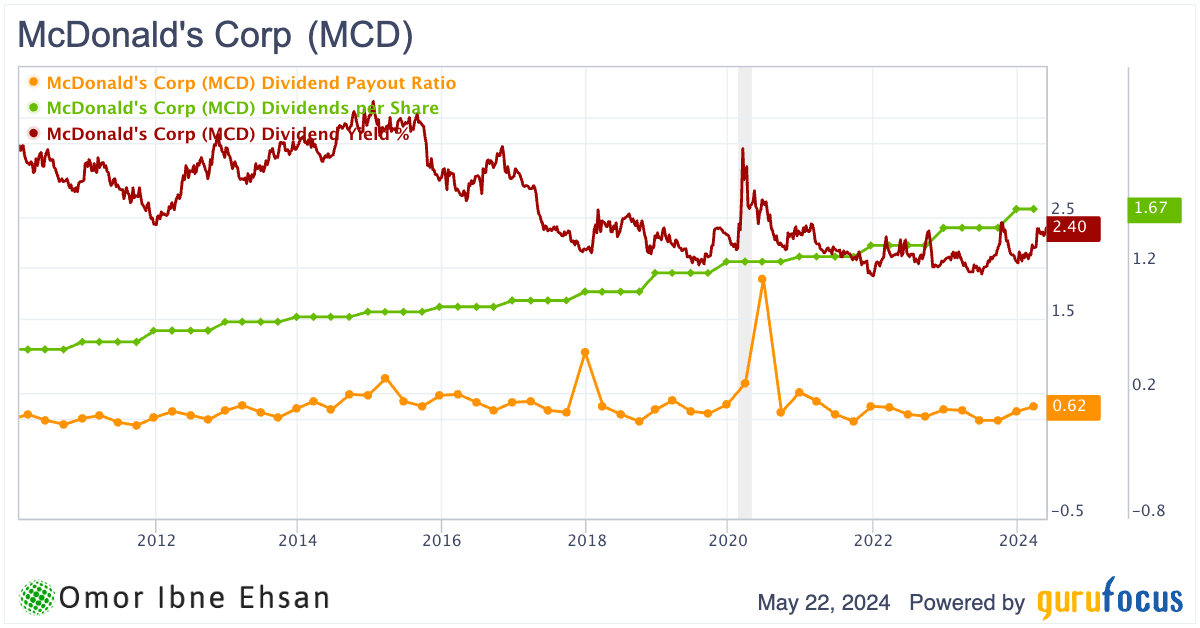

McDonalds (MCD)

You can’t go wrong with McDonald’s (NYSE:MCD). Historically, McDonald’s has weathered economic storms remarkably well. The stock gained 8.5% in 2008 as the S&P 500 plunged 37% during the Great Recession. And despite being a restaurant, McDonald’s only saw a 3% revenue dip in 2020 during the height of the pandemic. The Golden Arches have earned their reputation as an all-weather stock.

While the 4.6% revenue growth to $6.17 billion slightly beat estimates, the earnings miss with EPS of $2.70 coming in $0.03 below expectations is concerning. Comps growth is actually negative in the U.S. However, this is due to broad-based consumer pressures that are affecting every company. The dividend yields 2.51%. In the long run, MCD is unlikely to disappoint.

Click to Enlarge

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.