If you screen some of the top stocks on the market today, you’ll realize they were among some of the most deeply undervalued stocks at some point in the past decade. Most people looking at their charts now wish they were one of the contrarians who bought these stocks when they were trading at bargain-basement prices.

There are many deeply undervalued stocks on the market today, and most of them are actually profitable companies with a very long history and great staying power. Buying these stocks before the market cycle shifts is a good idea, and the recovery could boost your portfolio gains significantly. Here are seven such deeply undervalued stocks to look into.

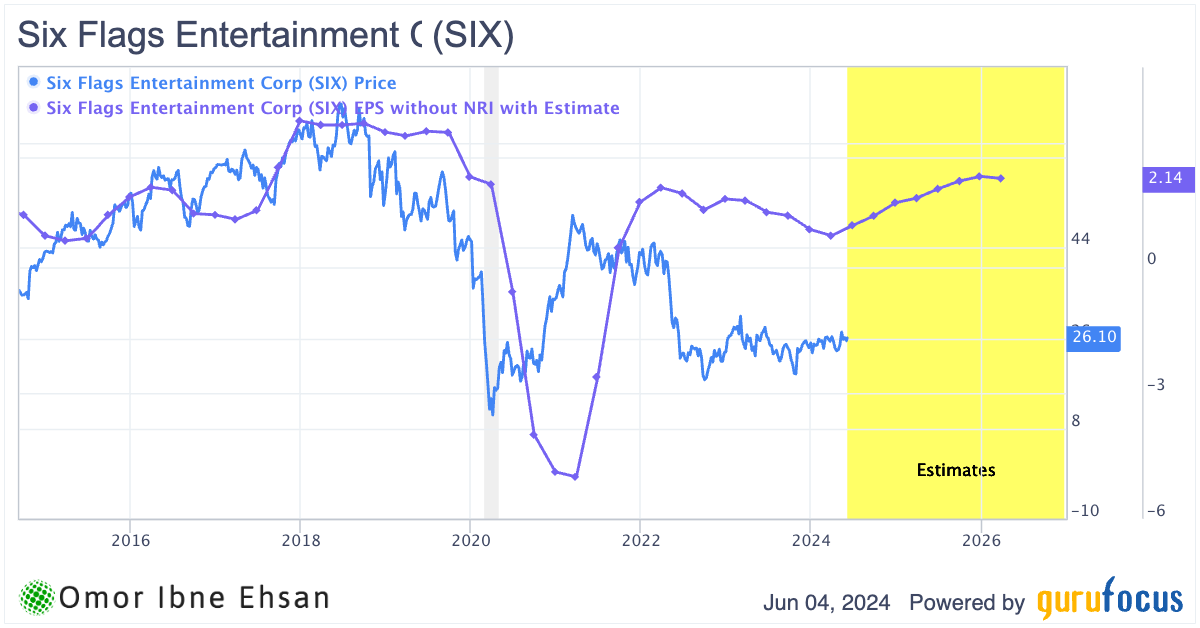

Six Flags Entertainment (SIX)

Six Flags Entertainment (NYSE:SIX) operates regional theme parks across North America. The stock has been mired in a brutal downtrend since 2018, with the pandemic delivering a crushing blow that it’s still recovering from. However, I believe brighter days lie ahead as travel demand resurges. In Q1, Six Flags’ season pass sales jumped double-digits, with both unit sales and average prices rising. Group sales have also rebounded over 20% year-over-year, nearing pre-COVID levels.

Most encouraging, in-park spending per guest climbed 5% when excluding discontinued memberships, driving record Q1 in-park revenues. Management’s “premiumization” strategy of enhancing park offerings and infrastructure seems to resonate as guests stay longer and spend more. Rising EPS should also lift the stock in the long run.

Click to Enlarge

I believe Six Flags’ attendance and margins can keep recovering as interest rates eventually ease and consumer discretionary spending picks up. For patient investors, this battered stock could deliver meaningful upside.

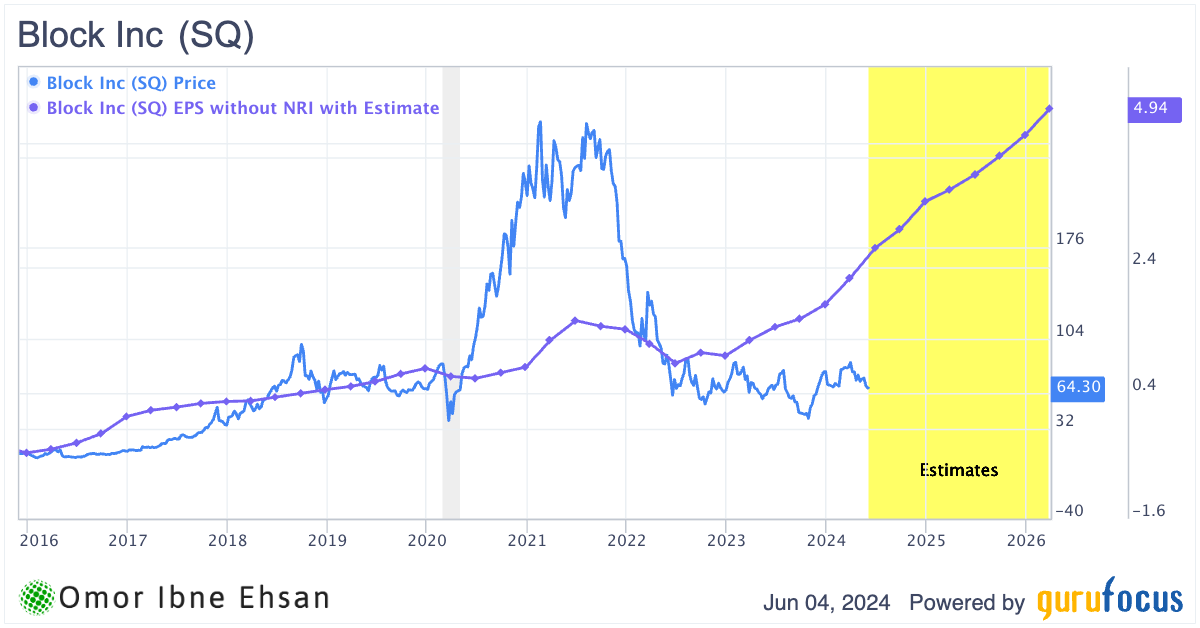

Block (SQ)

Block (NYSE:SQ) provides mobile payment solutions for businesses and individuals. The company delivered impressive Q1 results, beating on both the top and bottom lines with EPS of 85 cents and revenue growth of over 19% YOY to $5.96 billion.

While Block was often viewed as a high-growth but unprofitable alternative to PayPal (NASDAQ:PYPL), I believe the stock is deeply undervalued and poised for a sharp recovery. The recent pullback in shares alongside other fintech names misrepresents Block’s robust fundamentals.

Block has not only turned the profitability corner, but also maintained strong double-digit top-line momentum. Analysts expect 14% revenue growth for 2024 and expect EPS to skyrocket from $3.40 this year to $15 by 2033. It’ll be very hard for the market not to reward the profitability.

Click to Enlarge

Block looks like a compelling buy trading at these beaten-down levels.

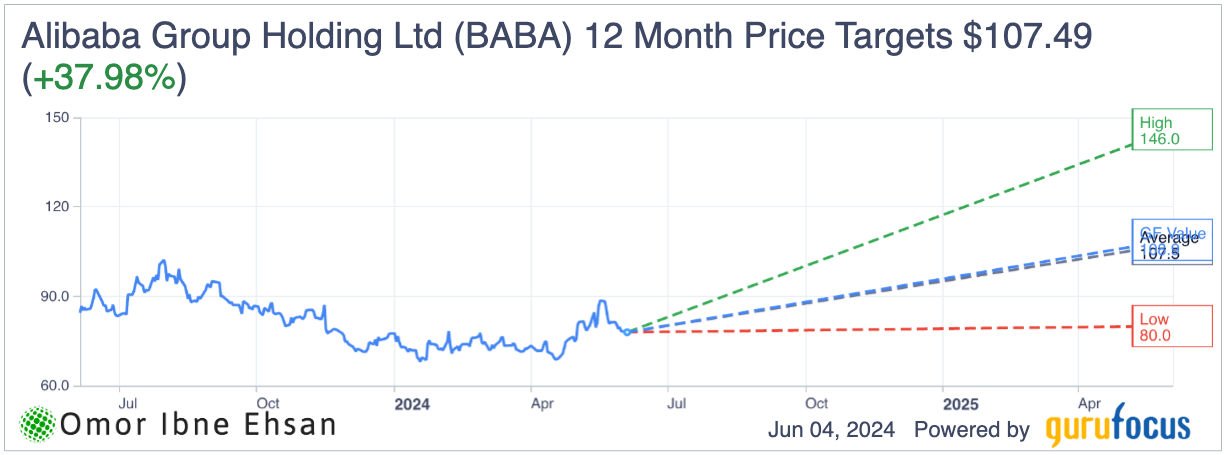

Alibaba (BABA)

Alibaba (NYSE:BABA) is one of China’s largest tech giants, and I believe the stock is a screaming buy at these depressed levels. The broader Chinese market has been struggling, but there are clear signs of a recovery as the government eases monetary policy. Alibaba reported robust results this quarter, with its core Taobao and Tmall businesses achieving double-digit GMV growth. International commerce revenue surged 45%, and cloud revenue saw strong double-digit gains, driven by triple-digit growth in AI-related sales.

I’m confident Alibaba will outperform going forward as it slashes cloud service prices to boost adoption. With China’s vast data industry unlikely to rely on foreign tech, Alibaba is perfectly positioned to dominate this market for years to come. Management expects a gradual return to healthy GMV growth in fiscal 2025 as the shopping experience improves. While new monetization products won’t launch until the second half, I believe Alibaba’s investments in pricing, supply, and service will pay off hugely in the long run. Analysts also see solid upside.

Click to Enlarge

It is definitely one of the most deeply undervalued stocks at these levels.

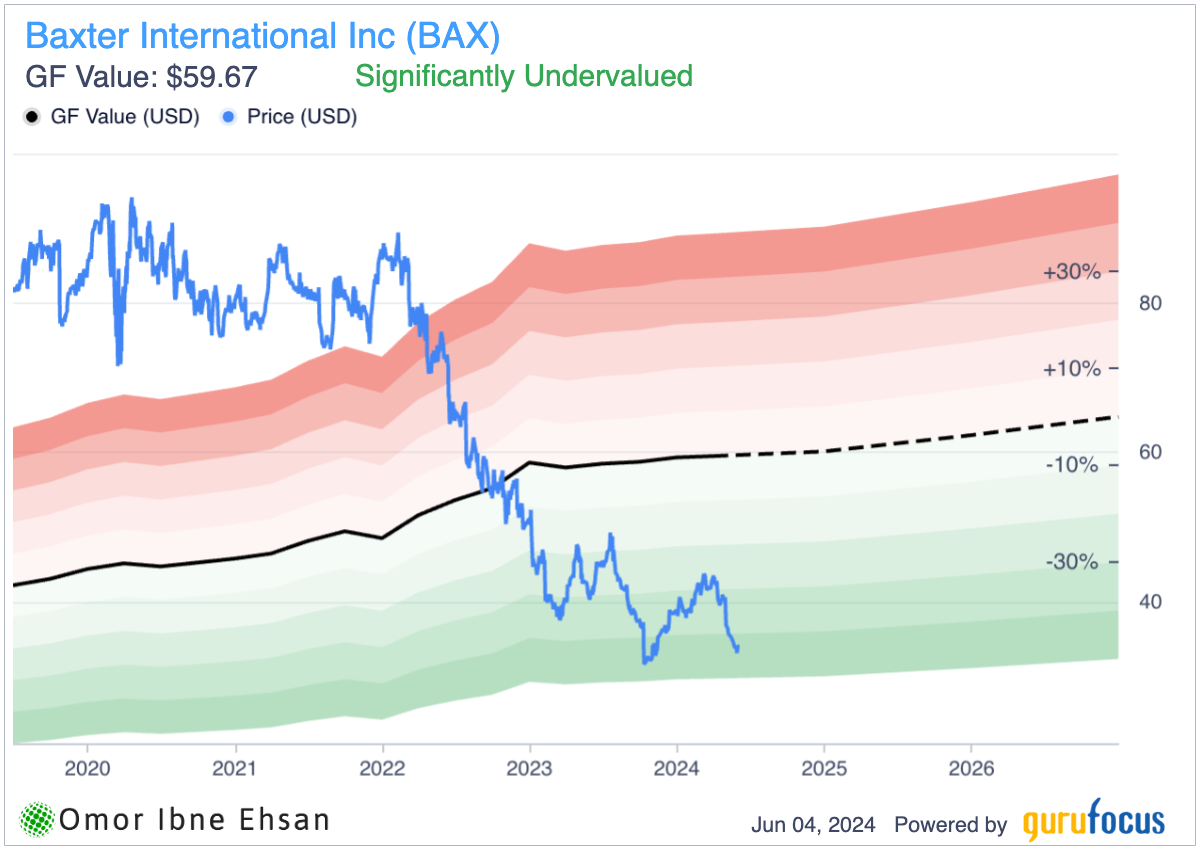

Baxter International (BAX)

Baxter International (NYSE:BAX) is a leading global medical products company. I believe Baxter is a deeply undervalued stock poised for significant upside. The healthcare industry is booming due to an aging population, new drug innovations, and increasing health challenges. Baxter is well-positioned to benefit from these tailwinds in the long term.

In Q1, Baxter delivered solid results, beating on both revenue and EPS. Sales grew 3% in constant currency, driven by broad-based demand and pricing strength. Margin improvement initiatives are also gaining traction. Baxter’s essential product portfolio and newly streamlined operating model provide durability and strategic clarity.

The stock has been unfairly punished, down 61% from 2020 highs. But at these levels, the downside appears limited, with considerable recovery potential.

Click to Enlarge

Baxter also offers an attractive 3.4% dividend yield.

While the Healthcare Systems & Technology segment underperformed, I’m encouraged by the recent FDA clearance of Baxter’s next-gen Novum IQ infusion pump platform. As hospitals upgrade aging equipment, this should drive growth.

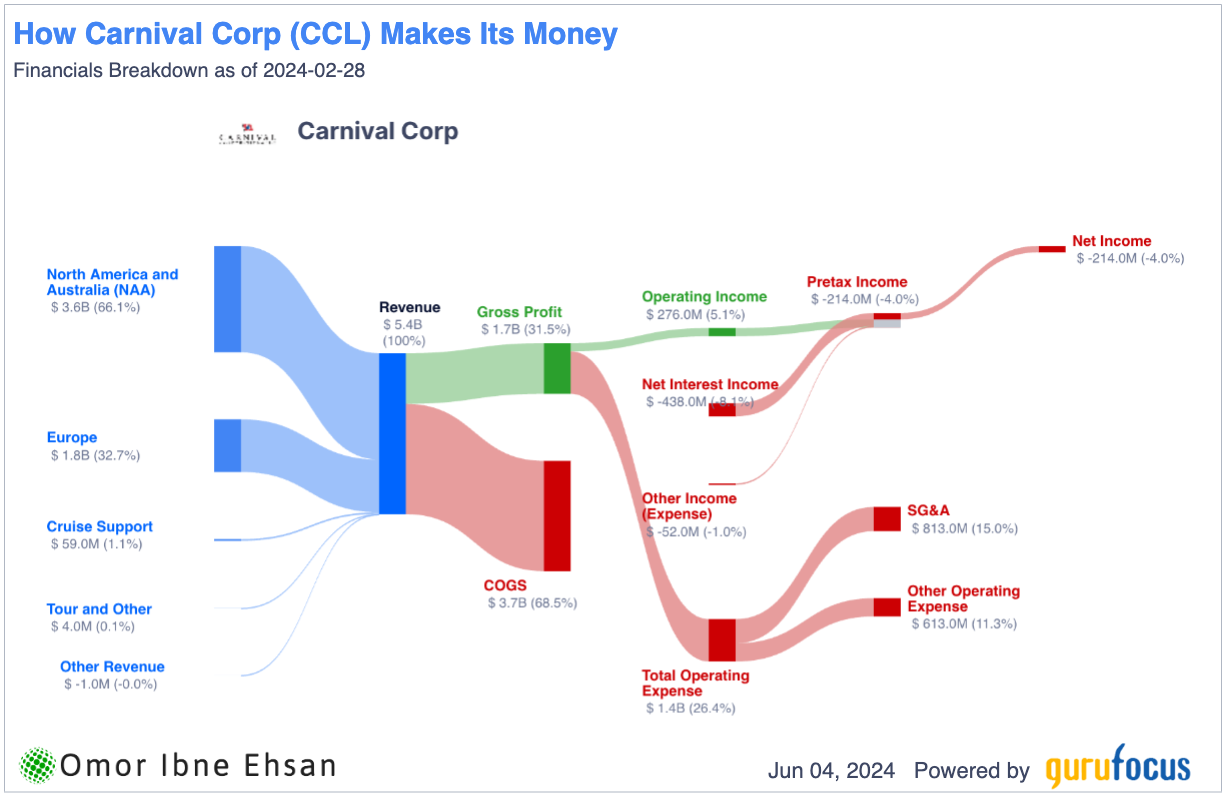

Carnival Corporation (CCL)

Carnival Corporation (NYSE:CCL) is a cruise travel company. I believe Carnival stock is deeply undervalued and poised for a significant recovery. The company delivered record revenues, bookings, and customer deposits in Q1, with yields increasing over 17% YOY. Carnival is capturing more new guests than ever.

The stock is still down 66% from pre-pandemic levels but has climbed 30% in the past year as the cruise industry rebounds. With the Fed signaling potential rate cuts ahead, Carnival seems primed to benefit, given its hefty debt load. Lower interest rates would ease the burden of interest payments and free up more cash flow. It should easily return to positive margins as rates come down.

Click to Enlarge

As people flood into cruise-heavy markets like Florida, Carnival should see a surge in bookings and pricing. Management is already pulling the booking curve forward to support higher overall pricing. I expect Carnival to sail towards much smoother waters, but it is currently one of the most deeply undervalued stocks, at least in my eyes.

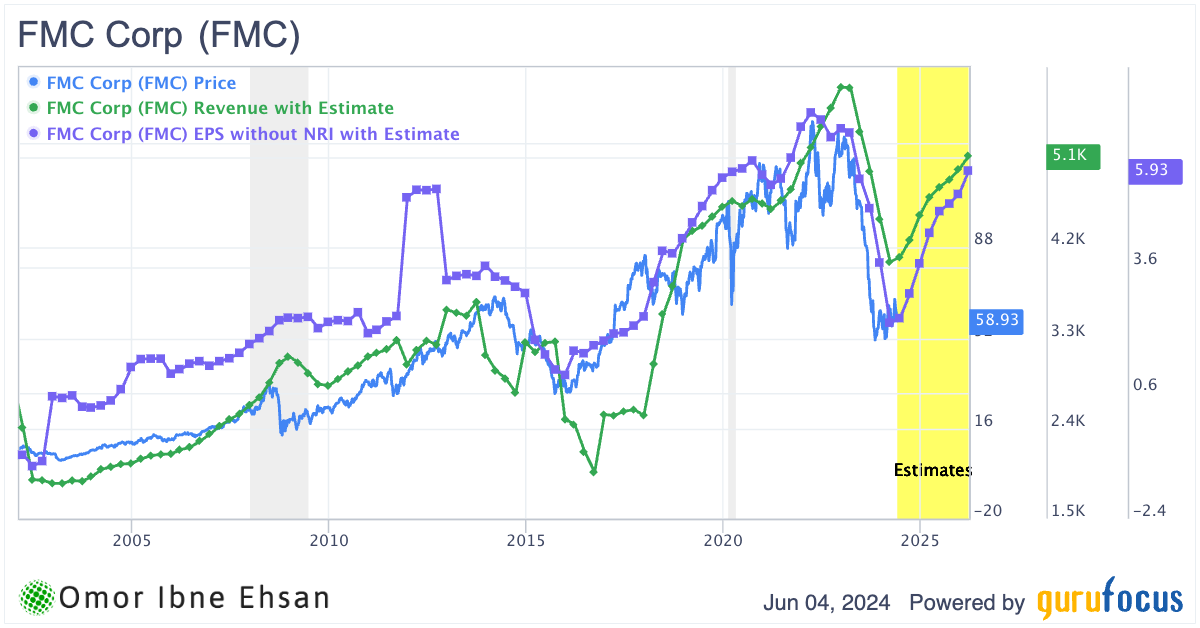

FMC Corporation (FMC)

FMC Corporation (NYSE:FMC) makes crop protection products. The stock has plummeted by nearly 60% since the beginning of 2023, but I believe there’s a compelling case for a turnaround. While Q1 revenue missed expectations due to ongoing channel destocking, the long-term outlook remains promising.

Growers have delayed purchases to manage bloated inventories, temporarily crushing demand. However, as excess supplies are depleted and the channel stabilizes, FMC is well-positioned to capitalize on the anticipated market recovery starting in Q2.

Despite the 32% YOY revenue decline, FMC delivered EBITDA at the high end of guidance and EPS above the midpoint. Restructuring actions are on track to deliver $50-75 million in net savings this year. Moreover, free cash flow showed remarkable improvement compared to Q1 2023. I believe we’ll see a solid price recovery with revenue and EPS rebounding.

Click to Enlarge

Branded diamides posted double-digit growth in Latin America, while the Xyway and Adastrio fungicides excelled in North America. As headwinds dissipate and these offerings gain traction, FMC’s fundamentals should strengthen considerably. The recent selloff seems like a solid entry point. It also has a 3.94% dividend yield.

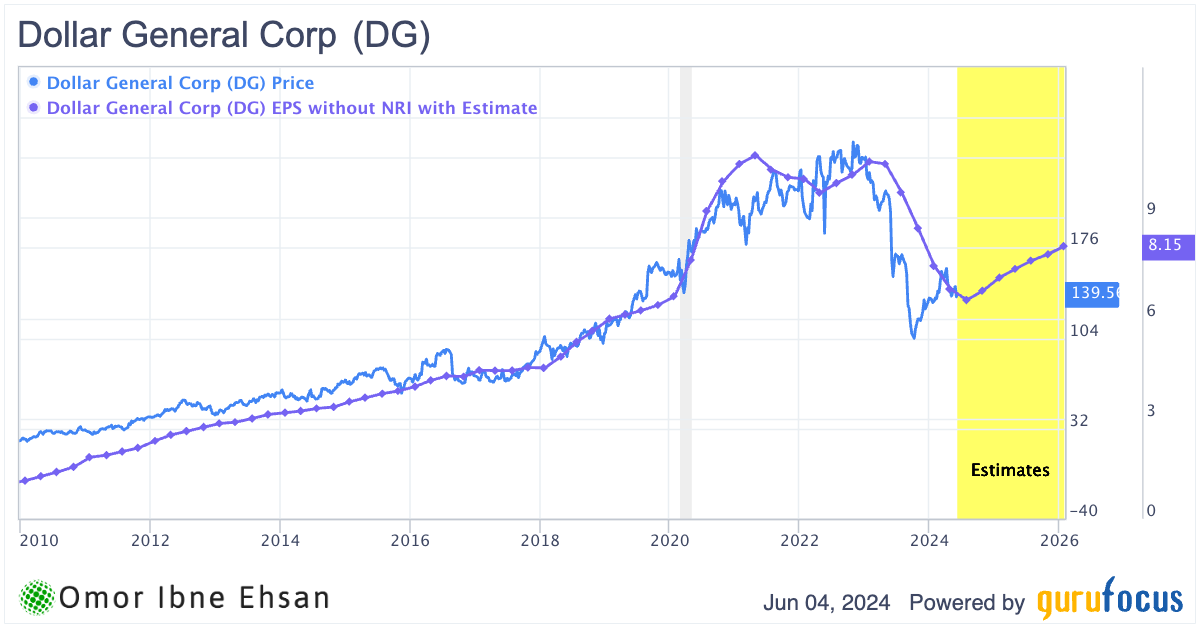

Dollar General (DG)

Dollar General (NYSE:DG) operates a chain of discount retail stores across the United States. The stock has been unfairly punished in the recent market selloff and is trading at a bargain price.

In Q1, DG delivered an impressive 6.1% sales growth to $9.9 billion while expanding its footprint with 197 new stores. Same-store sales also beat expectations, rising 2.4% on strong 4%+ customer traffic growth. The company can attract shoppers in basically any economic climate. Plus, TTM EPS is expected to start recovering soon.

Click to Enlarge

Management noted that budget-conscious consumers are increasingly relying on DG for essential consumables, driving market share gains. DG is well-positioned to keep winning over customers who are trading down from higher-priced retailers.

While near-term headwinds have weighed on the stock, I believe this is a classic case of the market overreacting. DG’s long-term growth story remains firmly intact. Patient investors who buy this dip should be handsomely rewarded as this best-in-class retailer gets back on the path to delivering market-beating returns. The stock also has a 1.69% dividend yield to sweeten the deal.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.