A handful of stocks have been driving the stock market’s gains for the past two years. Many call it the “Magnificent 7,” though investors haven’t been too enthusiastic about Tesla (NASDAQ:TSLA) or even Apple (NASDAQ:AAPL) up until its AI announcement. I believe the true favorites right now are the ones that still have an overwhelming amount of “Buy” and “Outperform” ratings despite their recent rally.

A large number of bullish analysts usually indicate that Wall Street has a positive consensus about certain stocks. Indeed, most of the stocks we will be talking about today are in the “Magnificent 7” and have gained a lot. It makes sense to play these favorites if you think the rally will go on. Here are my opinions about each of them:

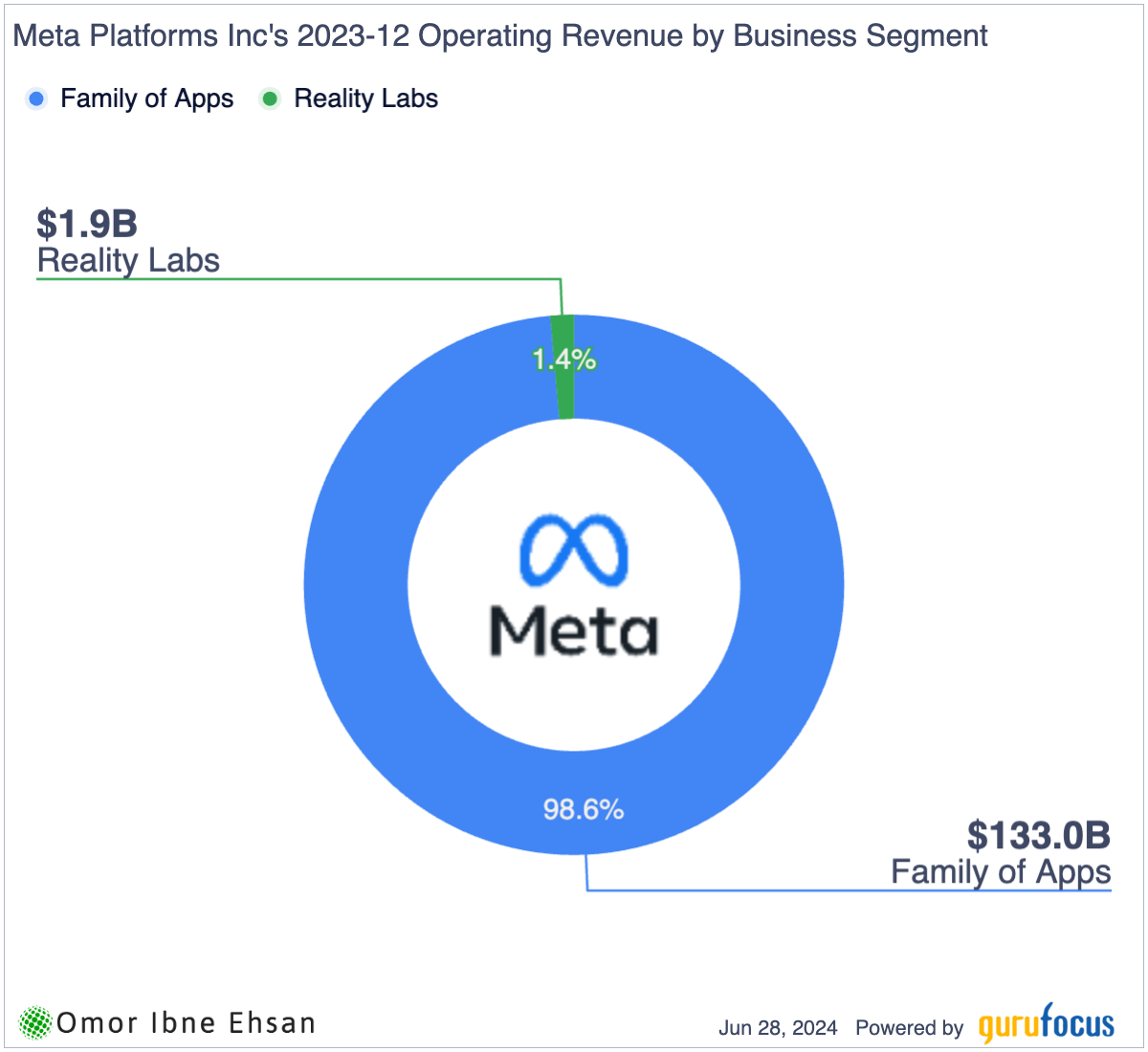

Meta Platforms (META)

Meta Platforms (NASDAQ:META) operates social media and communication apps like Facebook, Instagram, WhatsApp, and Messenger. The stock has staged a remarkable recovery from the depths of despair in late 2022 when I was banging the table as it sank below $100. Back then, the market myopically fixated on Meta’s money-losing metaverse bets while losing sight of the bigger picture. Losses on Reality Labs matters very little.

Click to Enlarge

Now at $519, I believe Meta’s valuation premium is justified, given its incredibly strong Q1 results. Revenue surged 27% year-over-year to $36.46 billion, beating estimates by $232 million. EPS of $4.71 also trounced expectations. Meta’s “Family of Apps” remains robust cash cows that are still growing, with over 3.2 billion people using at least one of them daily.

Looking ahead, a potential TikTok ban could be a huge tailwind. While Meta isn’t immune to broader market corrections, I’m convinced it’s a rock-solid long-term investment poised to keep pace with the market. Zuckerberg’s AI ambitions with Meta AI also seem promising.

Amazon.com (AMZN)

Amazon (NASDAQ:AMZN) is a global technology giant focusing on e-commerce, cloud computing, digital streaming, and artificial intelligence. As one of Wall Street’s most hyped “Magnificent 7” stocks, Amazon has finally broken above its 2021 peak, and I believe it will soon surpass the $200 level. The company’s latest earnings report was impressive, with revenue growing 13% year-over-year to $143.3 billion and operating income skyrocketing 221% to $15.3 billion.

While e-commerce remains a core pillar, Amazon’s growth story extends far beyond online shopping. AWS, the company’s cloud-computing platform, continues to dominate the market. Moreover, Amazon’s investments in AI through Anthropic are paying off, with its cutting-edge “Claude 3.5” model outperforming OpenAI’s GPT-4.

On the e-commerce front, Amazon’s plans to launch a low-cost apparel and home goods storefront to rival Shein and Temu could unlock significant growth potential. It’s self-explanatory why Wall Street loves the stock.

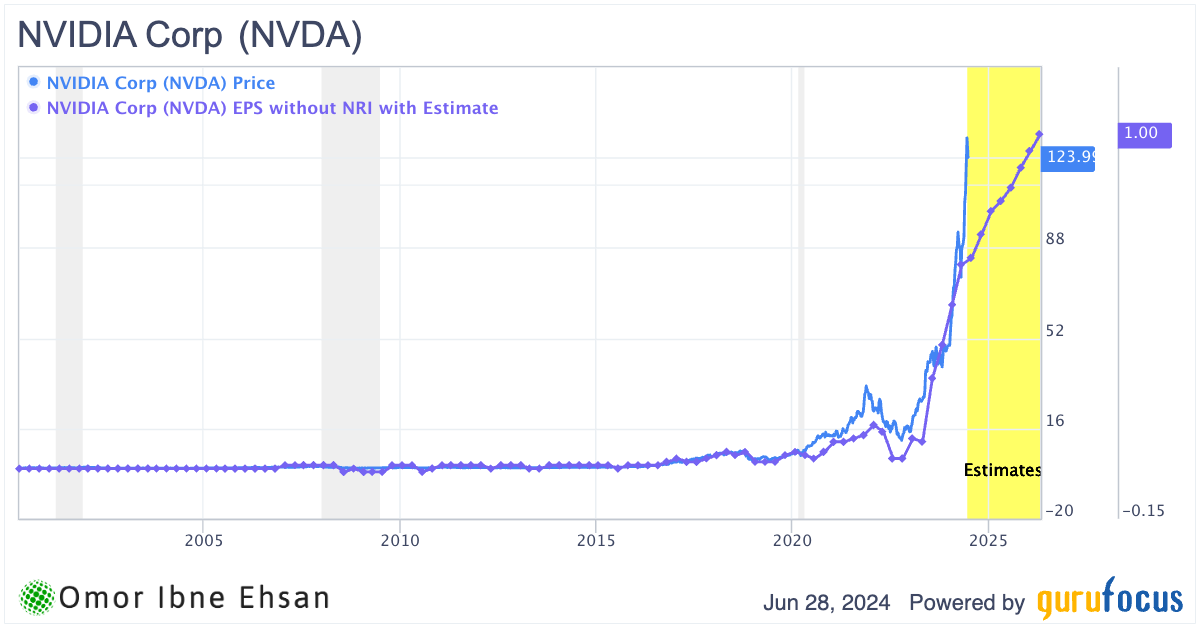

Nvidia (NVDA)

Nvidia (NASDAQ:NVDA) is a semiconductor company that designs graphics processing units (GPUs) for gaming and professional markets and system-on-a-chip (SoC) units for mobile computing and automotive markets. And, of course, AI chips. The stock has been the biggest winner of the AI hype cycle.

Nvidia’s Q1 2025 results were nothing short of spectacular, with revenue surging 262% year-over-year to a record $26 billion. The Data Center segment was the star of the show, rocketing 427% to $22.6 billion as major cloud providers and enterprises rapidly adopted Nvidia’s cutting-edge AI chips. Gross margins expanded to a stunning 71.6%, fueling a mind-boggling 843% explosion in earnings per share to $2.05.

While the growth story here is undeniably impressive, I have reservations about chasing this rally at a nosebleed-inducing $3 trillion valuation. Semiconductor companies are notoriously cyclical, and this feels like a classic case of market exuberance detaching from fundamentals. Even if it keeps beating estimates in the long run, the premium is pretty hefty already. Those estimates could also see big changes if we see chip demand start slowing down.

Click to Enlarge

Tech giants are developing in-house AI chips and competition could start nipping at Nvidia’s heels. Betting on Nvidia at these levels requires a leap of faith. It briefly surpassed Microsoft (NASDAQ:MSFT) as the world’s most valuable company before pulling back.

Microsoft (MSFT)

Speaking of Microsoft, I think it is hands-down the best long-term tech stock you can buy right now. Microsoft delivered record Q3 results, powered by the continued strength of its cloud business. The company’s early bet on OpenAI is starting to pay off handsomely, with over 65% of the Fortune 500 now using Azure OpenAI Service. Microsoft’s “Copilot” AI features are already transforming productivity across its software suite. I believe Microsoft is emerging as the biggest enterprise AI play.

With Azure taking share and Arc streamlining cloud migrations for major customers, Microsoft’s intelligent cloud segment grew a robust 22% to $27.1 billion. Even the mature Productivity and Business Processes segment accelerated to 16% growth, driven by AI-enhanced Office 365 and Dynamics 365. This shows the stickiness of Microsoft’s enterprise offerings. Windows may finally be seeing a revival thanks to the AI-powered “Copilot” assistant.

While Microsoft faces stiff competition on multiple fronts, from Google in AI to Amazon in cloud, I believe its unrivaled enterprise footprint and vertical integration give it a major advantage. The breadth of Microsoft’s portfolio is simply unmatched. With $20.1 billion in Q3 operating income, up 17%, this tech titan’s moat looks as formidable as ever.

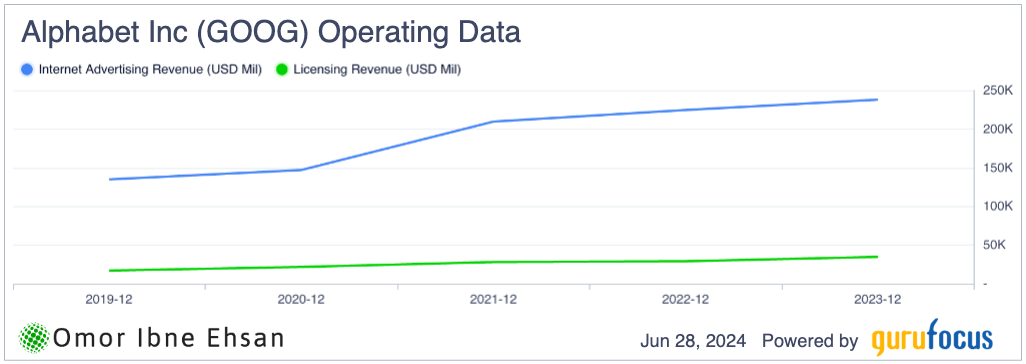

Alphabet (GOOG, GOOGL)

Alphabet (NASDAQ:GOOG, NASDAQ:GOOGL) operates Google and YouTube, two of the most irreplaceable tech platforms today. Despite having a muted start to the “Magnificent 7” rally, GOOG has been delivering solid gains. I believe it’s one of the best long-term stocks you can own, with an unassailable moat.

In Q1, Alphabet delivered impressive results with EPS of $1.89, beating expectations by 39 cents, and revenue of $80.54 billion, up a robust 15.41% year-over-year. Search continues to power the company’s growth engine, and management expects YouTube and Cloud to exit 2024 at a combined $100+ billion annual run rate. Advertising revenue growth has also remained strong.

Click to Enlarge

Even Microsoft’s AI advantage and integration of GPT-4 into Bing has not dented Google’s search dominance. YouTube also remains peerless, with an unrivaled content library that creates an incredibly high barrier to entry for any would-be competitors. It’s a stock you can buy for the long run with your eyes closed.

Palo Alto Networks (PANW)

Palo Alto Networks (NASDAQ:PANW) is a leading global cybersecurity company. In my view, this is one of the most promising areas of the market, with the cybersecurity industry projected to grow from $190.4 billion in 2023 to $298.5 billion by 2028 at an impressive 9.4% CAGR. Palo Alto’s latest earnings results underscore its position as one of the fastest-growing players in this critical space.

The company delivered strong Q3 FY2024 numbers, with EPS of $1.32, beating estimates by 7 cents, and revenue of $1.98 billion, growing 15.33% year-over-year and exceeding expectations by nearly $18 million. While Palo Alto undoubtedly trades at a premium valuation, I believe its robust growth trajectory could be sustained. Analysts are modeling for EPS and revenue to increase at a compelling 20% and 17% annual clips on average, respectively, over the coming decade.

However, it’s important to recognize that if broader market sentiment deteriorates, high-multiple names like Palo Alto could face a substantial correction.

Advanced Micro Devices (AMD)

AMD (NASDAQ:AMD) is a semiconductor company that designs high-performance computer processors and graphics cards. The AI revolution has recharged AMD stock, which has surged nearly 45% in the past year despite pulling back nearly 25% from its March highs. I believe this pullback presents an attractive entry point for long-term investors who are bullish on AMD’s AI prospects.

In Q1, AMD displayed impressive strength, with revenue jumping to $5.5 billion and both data center and client segment sales skyrocketing over 80% year-over-year. The 80% growth in data center revenue to a record $2.3 billion particularly caught my eye, driven by robust demand for AMD’s cutting-edge Instinct MI300X GPUs and EPYC server CPUs.

While AMD’s rally has been electrifying, I’m tempering my enthusiasm until we see concrete evidence of startup adoption for AMD’s AI chips. Nvidia’s dominance in this space is formidable, and AMD needs to prove it can capture meaningful share to justify a richer valuation. However, if the AI boom persists and AMD executes, I believe this semiconductor powerhouse has room to run.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.