Welcome to Smart Money! My name is Eric Fry, and I’m glad you’re here.

There’s no perfect investment method. If there were, we’d all be millionaires and you probably wouldn’t be reading this letter.

But there is a way to allocate your assets intelligently, so you set yourself up for the best chance at success…

There are multiple facets to this strategy, but the one I want to focus on today is stocks to buy and hold forever.

You should think of these investments as your core holdings – your “Forever Stocks.” Treat these Forever Stocks as your “Elite 8” or “Top 10” – or whatever number you decide on. In total, these stocks should represent about 25% to 35% of your total portfolio.

These are the stocks you hold through thick and thin, unless the rationale for owning them changes significantly or you decide to replace one of them with a different stock.

Obviously, Forever Stocks will suffer during a severe bear market, just like ordinary stocks. So any investor who holds onto stocks like these during a sell-off is likely to suffer mark-to-market losses.

But these losses are a small price to pay for big, long-term gains…

And today, I have seven stocks that I consider to be some of the best “Forever Stocks” out there.

Let’s get started…

Stock No. 1: Corning Inc.

If we were to play a word-association game and I said, “Artificial intelligence,” you might respond with something like “Nvidia,” or “Google,” or maybe “robots.” You probably would not say “Corning.”

But as it turns out, this iconic glass maker could benefit significantly from the AI boom, as a classic “picks and shovels” play.

For more than 170 years, the Corning Inc. (GLW) name has been synonymous with best-of-breed glass products. It has continuously innovated and set the industry standard for excellence.

In 1879, a 32-year-old Thomas Edison approached Corning with the concept of a lightbulb. This new invention would require a specialized glass that would be stronger than typical window glass but could also encase delicate filaments inside the bulb. Corning fulfilled the mission and became Edison’s sole supplier.

Over the ensuing decades, Corning produced a variety of glass-based marvels, dominating one industry after another. In the 1960s, for example, Corning was producing 100% of the world’s TV screen glass.

In 1970, Corning introduced the world to the company’s most marvelous marvel of all: low-loss fiber optics. With this groundbreaking invention, thin strands of Corning glass could replace copper wire in telecommunications networks and transmit millions of bits of information per second via photons (pulses of light), rather than electrons.

Thus, the world of optical communications was born… and it has continued to thrive ever since.

Today, the company operates in five different business segments – Optical Communications, Display Technologies, Environmental Technologies, Life Sciences, and Specialty Materials – each of which has been battling cyclical headwinds for the last three years.

Despite these challenges, third-quarter 2024 results exceeded expectations, being led by strong performance in Optical Communication. The segment saw a 55% year over year sales increase in its Enterprise business, fueled by growing demand for optical-connectivity products used in generative AI. Meanwhile, Display Technologies raised prices and projects segment net income of $900 million to hit $950 million in 2025, with a target net income margin of 25%.

But throughout good times and bad, Corning continuously invests in its future. In 2023, the company spent about $1 billion on research and development, just like it has every year since 2018.

These sizeable R&D efforts help fortify Corning’s dominant position in its primary markets. Additionally, the company’s innovative product refinements and launches enable it to advance the over-arching strategy it calls “more Corning.”

“We aren’t exclusively relying on people just buying more stuff,” CEO Wendell Weeks explains. “We’re putting more Corning into the products that people are already buying.”

One notable example of the “more Corning” strategy at work is the Mercedes-Benz hyper-screen dashboard display, which features a Corning “Gorilla Glass” cover nearly five feet wide. As a result of commercial successes like these, Corning now generates $100 of revenue per car on some models – up from just $15 a few years ago.

Now, AI has come to power a massive “more Corning” upgrade cycle.

“More AI”

The path from AI to Corning is fairly direct and intuitive. AI technologies require enormous processing power from data centers. Because this new source of demand is surging, the companies that operate data centers are ramping up their capacity by building new centers and/or boosting the capacity and speed of existing centers.

That means surging demand for the optical fiber and components that Corning produces. Importantly, the growing AI workloads not only require more data centers, but also more fiber optic connections per data center.

According to CEO Weeks, modern data center systems that rely on Nvidia Corp.’s (NVDA) popular Hopper H100 GPUs require 10 times more fiber optics than a conventional data center server rack.

As Weeks explained on CNBC, “We’ve invented new fibers, new cables, new connectors, and new custom integrated optical solutions to dramatically reduce installation costs, overall time and space, and carbon footprint.”

Therefore, it is easy to see how more data center processing power means “more Corning.” On average, Corning estimates that data centers running AI large language models (LLMs) will require five times more optical connectivity than they have today.

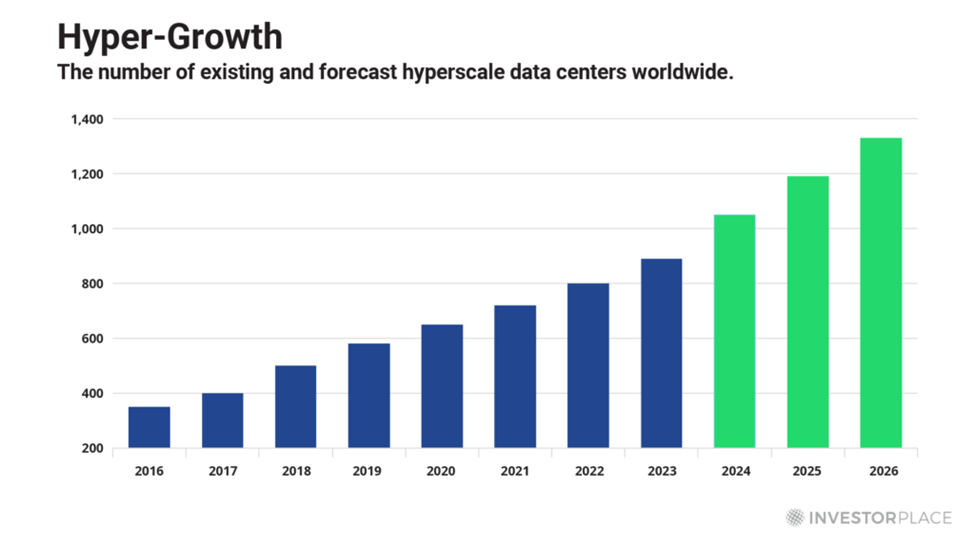

In 2024 alone, hyperscalers like Alphabet Inc. (GOOGL), Amazon.com Inc. (AMZN), and Meta Platforms Inc. (META) invested about $200 billion in data centers, hardware, and other technologies required to deploy generative AI models.

This massive investment caps a multi-year data center construction wave that has doubled the total capacity of hyperscale data centers during the last several years, according to Synergy Research Group. The Group predicts capacity will double again during the next few years, as 120-130 new hyperscale centers come online each year.

This building boom is finally showing up on Corning’s order books, with the company citing “strong adoption of our new optical connectivity products for Generative AI.”

Coincident with the data center boom, Corning is seeing trend improvements in its other major end markets, like smartphones. As a result, Weeks believes a $3- to $5-billion revenue surge will land on Corning’s income statement over the next year.

If these expected revenues arrive in a timely manner, Corning could earn as much as $3.00 per share within one year, and $3.50 within two years. At that level of profitability, Corning shares will be trading for 15 times 2026 earnings and just 13 times the 2027 result.

Obviously, this hoped-for revenue surge is not yet in the door. But the trajectory is very promising. If/As/When this revenue does materialize, Corning shares could easily double from the current quote.

In the wake of a favorable Barron’s story about Corning in June 2024, and the company’s subsequent upward earnings revision, the stock is no longer the “secret” AI play it once was.

However, it remains a relatively cheap and underappreciated AI play.

So, as these tech darlings like Nvidia and Amazon continue to prosper, I would favor the unloved Corning for the next phase of the AI boom.

Stock No. 2: Teradyne Inc.

Teradyne Inc. (TER) presents a rare and timely investment opportunity, combining cyclical upside in its core semiconductor testing business with a growing robotics segment that’s rapidly gaining real-world traction, including a potentially transformative partnership with Amazon. With strong fundamentals, strategic positioning in AI-driven automation, and a healthy balance sheet, Teradyne is poised to benefit from both short-term catalysts and long-term secular growth trends.

Teradyne is a global leader in Automated Test Equipment (ATE), essential for testing advanced chips in smartphones, AI servers, automotive electronics, and high-bandwidth memory (HBM). After a cyclical downturn, the semiconductor industry is beginning a recovery, as indicated by the company’s robust first-quarter results and resurgent capacity utilization rates in the semiconductor industry.

Teradyne’s semiconductor testing revenue rose nearly 25% year-over-year in the first quarter of this year, which signals resurgent momentum. As AI deployment drives up demand for memory and advanced chip testing, Teradyne’s testing division should continue to post double-digit revenue growth for several quarters.

But Teradyne is also a fascinating robotics play, thanks to its savvy acquisitions of Universal Robots (UR) in 2015 and Mobile Industrial Robots (MiR) in 2018. Now that these acquisitions are well integrated into the company, Teradyne is producing industry-leading collaborative and mobile robots. In fact, the robot leader, Amazon, has begun deploying Teradyne’s UR-powered robotic arms in its Vulcan robot, which it touts as a revolutionary breakthrough in warehouse automation.

Amazon stows 14 billion items a year by hand — and aims to automate 80% of that. Based on estimated deployment needs, this could mean 5,000+ Vulcan units, with potential revenue for Teradyne ranging between $600 million and $1.25 billion over time. Even a phased rollout could surpass Universal Robots’ entire current revenue. Importantly, Vulcan’s success could drive other companies to adopt similar solutions, positioning Teradyne as the premier “picks and shovels” supplier of the next wave of warehouse automation.

Teradyne’s ongoing collaboration with Nvidia is another key asset. Nvidia is integrating its Isaac platform into both Teradyne’s “universal robots,” the kind that operate alongside humans in industrial settings, and its “mobile industrial robots.” These robots can now think and react in real time, which is a necessity for chaotic environments like Amazon’s fulfillment centers. This collaboration with Nvidia gives Teradyne a major edge as AI-powered automation scales globally.

Currently, robotics contributes less than 15% of Teradyne’s revenues. But that percentage could ramp up quickly if the robotics industry enters the mega-growth phase many experts anticipate. Teradyne management has guided long-term EPS to $7.00–$9.50 by 2028, but the company’s history of conservative forecasts and industry-beating execution suggests upside potential.

If, for example, EPS reaches $11.00 by 2028 and TER trades at its historical 20x P/E, that implies a price of over $200 — or more than double its current price. If the robotics boom surprises on the upside, and Teradyne’s market share in the robotics industry grows, a $400 share price is not out of the question. As an added plus, the company boasts a rock-solid balance sheet with half-a-billion-dollars worth of net cash.

Teradyne offers investors rare dual exposure: a cyclical rebound in semiconductors and a secular growth story in AI-powered robotics. The company sits at the forefront of the next industrial revolution, providing essential technology for AI, automation, and robotics. With a growing pipeline, AI-powered product innovation, and a transformative opportunity with Amazon, Teradyne is a compelling play on the future of intelligent machines.

Stock No. 3: Block Inc.

Volatility can open the door to new buying opportunities.

That’s how I spotted Block Inc. (XYZ), which owns and operates the well-known payment app, Square.

The company’s story starts like this…

In 2009, Jim McKelvey, the founder of Mira Digital Publishing, ran into some trouble with his glass-blowing side gig. He wanted to sell an expensive set of glass bathroom faucets… but had no way of accepting his customer’s credit card. He spied a market opportunity.

In partnership with Twitter founder Jack Dorsey, the duo developed a square-shaped card reader that could plug into smartphones, eliminating the need for expensive card readers. It was a simple, elegant solution that cost just $0.97 in hardware and was given away to merchants for free.

In 2010, Square added 50,000 test merchants in a single summer. The following year, the firm was reportedly adding 100,000 new merchants every month.

Today, the company – now known as Block Inc.– helps merchants transact over $200 billion annually. Its point-of-sale systems are found everywhere from farmer’s markets to national retail chains. And the company has expanded far beyond the four-sided card readers that inspired its original namesake.

- Peer-to-peer payments. In 2013, Block launched Cash App, a peer-to-peer payments service that skyrocketed to popularity after offering lottery-style cash awards to users. In 2023, the mobile payment service available Cash App brought in over $248 billion of gross inflows, eclipsing Square by that metric.

- Small Business Software. In 2014, the company launched integration of payroll features. This would eventually grow into a full software suite that includes inventory management, business analytics and order tracking.

- Buy Now Pay Later. The company acquired Afterpay in 2022, a buy-now, pay-later service. This acquisition gave Block a toehold in the fast-growing market. Its BNPL segment contributed $1 billion in revenues last year.

- E-Commerce. The firm acquired web hosting company Weebly in 2018, which it would transform into an e-commerce website builder for small businesses.

- Crypto. Block has also made some moves into cryptocurrency, including starting a decentralized crypto platform, known as TBD, and a self-custody Bitcoin wallet, known as Bitkey.

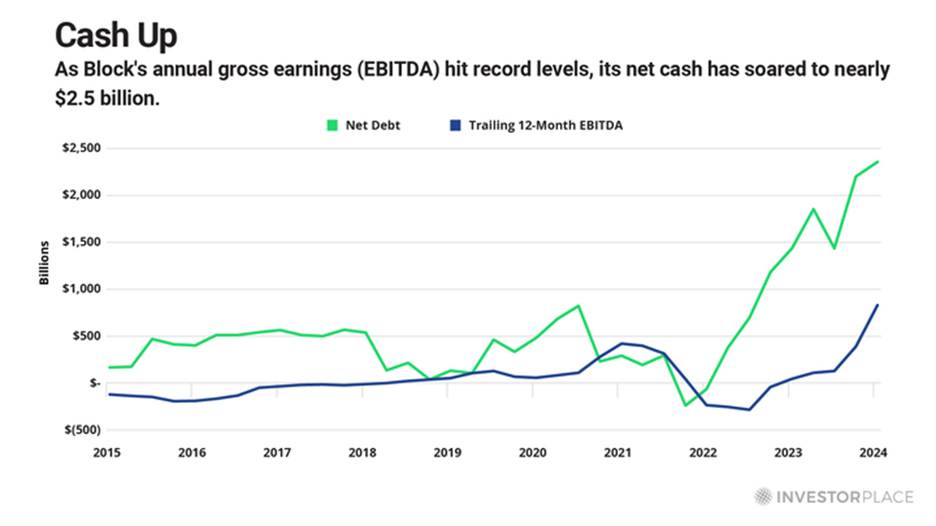

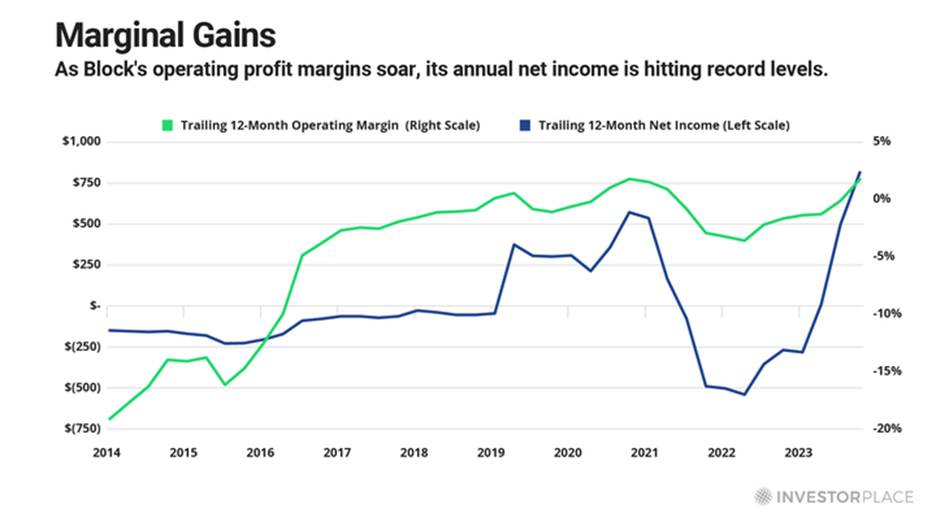

Thanks to Block’s sizeable multi-year spending on both capital investments and M&A, the company has become one of the world’s leading fintech companies. It has developed a comprehensive financial services ecosystem that serves both merchants and consumers, and has generated $230 million in free cash flow annually since 2019. Block now appears to have reached an important inflection point. Analysts expect free cash flow to essentially rise tenfold from historical levels to $3 billion in 2025. Now, the company is on a path to potentially grow beyond that.

In part, this hockey-stick-shaped growth is a reflection of the broader payment processing industry. The business tends to be highly scalable, since digital payment systems require large upfront investments that can eventually serve an unlimited number of additional customers at virtually zero marginal cost. (Block’s card readers also came with billions of costs in back-end investments). So, payment processors tend to become enormously profitable after they reach a certain scale.

But Block’s business model also exaggerates this growth trend, given its focus on flat fees, efficient client onboarding, and diversified software offerings. This creates more overheads, but also greater efficiencies once scale is reached.

In addition, the company’s Cash App product has gained a major adoption rate among younger demographic groups. It is the No. 3 app in the finance category on Apple Inc.’s (AAPL) App Store, and Gen Z’s and Millennials combined account for more than 70% of Cash App’s inflows. Additionally, Block is the only major fintech firm with a banking charter, and management recently announced intentions to roll out banking services for Cash App customers.

“It is about making Cash App our base’s primary financial tool,” Block CFO Amrita Ahuja said during his second-quarter earnings remarks, “which ultimately leads to stronger engagement and stronger inflows.” The Cash App card now has 57 million monthly transacting active users, making it even larger than many regional banks like TD Bank by that measure. This offering is an “option value” for future growth.

Best of all, shares of Block don’t yet reflect these truths. Investors rarely seem to reward forward-looking companies who “spend big” to gain market dominance and instead rely on the rearview mirror of past earnings and expenses. But this necessary evil is the exact process that companies like Amazon, Microsoft Corp. (MSFT), Netflix Inc. (NFLX), and others pursued to become legendary companies.

No. 4: Equinor ASA

Equinor ASA (EQNR) is the largest energy company in Norway and the ninth largest in the world, based on revenue. Importantly, it is Europe’s largest non-Russian supplier of natural gas, by far, and also a major crude oil producer.

The fact that this company operates next door to Russia used to be a footnote that barely deserved a mention. But that footnote became a headline after Russia invaded Ukraine.

At that time, Russia supplied about 40% of the natural gas Europe consumed every year. Norway was a distant No. 2 – providing 20% to 25% of Europe’s natural gas needs.

But as European countries have been phasing out Russian supplies of oil & gas, they have been phasing in additional supplies from Norway. Equinor benefits directly from this shift.

The company’s strong pipeline of development projects that will come on stream by 2030 will deliver around 6.5 billion barrels of oil equivalent (boe), at a breakeven level of $35 per barrel, while also producing a rapid average “payback” on investment of just two and a half years.

In keeping with that disciplined approach, Equinor recovered its investment in the recent Troll Phase III expansion in less than a year.

Additionally, the company has a long history of replacing reserves through disciplined exploration activities. During the last several years, Equinor achieved an average reserve-replacement ratio of 107%, In other words, it ended each year with 7% more reserves than when the year began. That’s an excellent record for a company of Equinor’s size.

Although the company strayed from its core oil & gas operations during the last few years to invest in “next generation” energy sources like wind and solar, it has been deemphasizing those activities recently.

I expect Equinor’s renewed focus on oil & gas production to position the company for solid earnings growth, assuming energy prices continue their recent uptrend.

At the current quote of nine times earnings, the stock is pricing in almost no upside. For perspective, Chevron Corp. (CVX) is trading for 20 times earnings, while Exxon Mobil Corp. (XOM) is priced at 15 times earnings.

Therefore, even in a “flattish” oil price environment, EQNR shares could trend higher to lift their valuation closer to its peers. In the meantime, the stock pays a hefty 5.4% dividend yield.

Stock No. 5: PayPal Holdings Inc.

PayPal Holdings Inc. (PYPL) is a titan of the digital payments industry.

The company traces its history to the year 2000, when Elon Musk merged his online bank, X.com, with Peter Thiel’s software company, Confinity, to form PayPal. The merged entity started spinning gold almost immediately for Musk and Thiel, as the inventive pair sold the company to eBay Inc. (EBAY) just two years later for $1.5 billion.

Then in 2015, eBay spun out PayPal as a separately traded company, which it has remained ever since. (Interestingly, 2015 was also the year that Musk and Thiel partnered up again to form OpenAI, the company that would go on to create the AI sensation, ChatGPT.)

PayPal’s platform has 434 million active accounts, while the annual volume of processed payments on its platform reached $1.68 trillion last year.

PayPal’s dominant position in the “branded checkout” segment has powered most of that growth. The “PayPal/Venmo” checkout button you might see when shopping online is an example of that business. 80% of the top 1,500 retailers in North America and Europe feature PayPal in their digital wallets.

But PayPal is not taking its success for granted. The company is fortifying its market leadership by integrating leading-edge AI and machine-learning processes into key aspects of its operations. For example, the company uses AI to detect fraudulent transactions and to boost the approval rate of valid transactions.

Buy Now, Pay Later

PayPal’s growth strategy relies on three key initiatives…

- Strengthening its core “branded checkout” solution.

- Growing its “unbranded checkout” solution.

- And developing and integrating AI processes that increase merchant sales, boost customer “stickiness,” and/or reduce operating expenses.

Branded Checkout is the foundation of PayPal’s business because of its high-margin fee structure. This business segment accounts for about one-third of the Total Payment Volumes (TPVs) the company processes, but it produces more than half of its total revenues.

PayPal is the market leader in branded online checkout with 36 million merchants on that platform. Although the company does not possess the commanding 99% merchant acceptance rate of legacy credit card companies like American Express and Mastercard, it has the largest acceptance rate of any “alternative payment method” (APM) provider. This category of payment solutions includes direct debit transactions, prepaid debit cards, and eWallets like PayPal, Venmo, Google Pay, and Apple Pay.

In 2020, PayPal launched a new “Buy Now, Pay Later” (BNPL) feature to bolster the appeal of its branded checkout offering.

This credit facility is similar to what established BNPL players like Klarna, Afterpay, and Affirm offer an immediate opportunity for shoppers to finance an online or in-store purchase at the point of sale.

Despite the brief operating history of PayPal’s BNPL offering, it has made rapid strides. Since launching BNPL, PayPal has issued loans to nearly 30 million customers. In 2022 alone, PayPal processed more than $20 billion of BNPL loans – up 160% from the prior year.

PayPal’s momentum in this market should propel it to undisputed leadership… and that’s no small matter in a sector that is growing as rapidly as BNPL consumerism.

Importantly, this category of transaction delivers an outsized benefit to merchants.

As PayPal attempts to expand its presence in the BNPL market, it will benefit from one major competitive advantage. The company has preexisting relationships with a huge swathe of the target market – both the merchants and the individual consumers.

Unlike its competitors, which must win new business to establish a BNPL relationship with a merchant, PayPal can deliver BNPL capabilities as a “bolt-on” to an existing relationship.

PayPal simply incorporates BNPL functionality into the existing checkout protocol. It is not a “new sale.” PayPal added BNPL capabilities to its existing relationship with Microsoft. Online shoppers at Microsoft’s Xbox Store can now access BNPL if they wish.

As CEO Dan Schulman explained…

Buy Now Pay Later continues to provide meaningful value to both our consumers and merchants. Over 32 million consumers have used our Buy Now Pay Later service since inception, at nearly 3 million merchants. We are now one of the most popular Buy Now, Pay Later services in the world… growing at 70% [year-over-year] on a currency-neutral basis.

Prudently, PayPal is working to “externalize” these loans by selling them to a third party, rather than retaining them on their own balance sheet. By selling the loans, PayPal removes the risk of holding bad loans.

The company took a giant step forward toward achieving that goal when it struck a deal to sell up to €40 billion of BNPL loans to the global investment firm KKR.

Under the terms of the agreement, KKR acquired PayPal’s existing European BNPL portfolio, along with future originations of eligible BNPL loans. PayPal will continue to conduct all the customer-facing activities of the loans, including underwriting and servicing.

This major transaction not only removes a large dollop of credit risk from PayPal’s balance sheet, but it also frees up capital to accelerate BNPL originations in Europe and/or to conduct shareholder-friendly activities like buying back stock.

Paving the Way

In addition to fortifying its leadership position in branded checkout, PayPal is expanding in the rapidly growing Unbranded Checkout segment.

The company refers to this solution as the PayPal Complete Payments (PPCP) platform, and it opens the door to a vast, new opportunity. Because this solution primarily serves small to mid-sized businesses, the total market opportunity is enormous. PayPal estimates the Total Addressable Market (TAM) to be roughly $750 billion.

The PPCP platform enables small businesses to accept credit cards and digital wallets as well as a range of Venmo and PayPal services. In April of 2023, PayPal gave this platform a major upgrade by adding Apple Pay to it.

That means that small businesses using PayPal as the backend for their payment processing can now accept Apple Pay alongside various other popular payment options.

Additionally, PayPal merchants can use their iPhone as a mobile point of sale terminal without the need for a dongle or other accessory device. Apple launched the technology in February of 2022.

CEO Schulman says that growing the unbranded checkout business has become a “strategic imperative” for PayPal – not just because it adds incremental revenue but also because it broadens and deepens customer relationships.

These expanded relationships produce vast troves of data that can fuel future AI enhancements.

Stock No. 6: Bristol-Myers Squibb Co.

Bristol-Myers Squibb Co. (BMY) is one of the largest pharmaceutical companies in the world, with a number of drugs that treat diseases in immunology, cardiovascular, and oncology. This portfolio includes blockbuster drugs like Eliquis, a blood anticoagulant for stroke patients, and Opdivo, used for the treatment of advanced-stage non-small cell lung cancer.

Artificial intelligence has not yet created a new blockbuster drug from start to finish – from drawing board to pharmacy – but it has made major contributions to the drug development process. A recently approved therapy from Bristol-Myers benefited from such a contribution.

Here’s the story…

In the early 1990s, biopharma firms Eli Lilly and Co. (LLY) and Novo Nordisk A/S (NVO) discovered a new drug they called xanomeline. Early tests found it was helpful in slowing cognitive decline related to Alzheimer’s and reducing the delusions and hallucinations that come with the disease.

There was, however, a major problem. The side effects associated with xanomeline were so severe that more than 50% of Phase 2 study participants dropped out. Patients suffered debilitating nausea, vomiting, diarrhea, excessive salivation, sweating, and intense gastrointestinal problems.

Xanomeline was eventually shelved. But that wasn’t the end of the story…

Almost a decade later, a Boston-based company named PureTech got interested. They realized that xanomeline’s efficacy came from its ability to bind to certain receptors inside the brain, while its side effects were caused by activating receptors outside the brain. The company bought the rights to the drug from Eli Lilly for just $100,000, which by then had turned its Alzheimer’s efforts to other therapies.

“Conceptualizing the problem that way, it felt like if we could find a way to selectively activate receptors in the brain without activating them on the periphery, that felt like a solution,” PureTech executive Andrew Miller said in an interview with Fierce Pharma. “That leads to this ah-ha moment of this concept of KarXT, where we have two drugs that have the same target but the opposite effect — one activates the target, the other blocks the activation of the receptor.”

At that point, the issue transformed from a conceptual problem into a practical one.

The PureTech team had identified at least 65 binders and 114 suppressors that could be combined to offset xanomeline’s side effects. And they knew that testing all 7,410 combinations would have been impossible in real life.

To come up with a solution, PureTech’s team turned to predictive algorithms, a form of AI.

The details of their machine-learning process continue to be kept a trade secret, but we know that their formula eventually came up with a solution: a molecule named trospium chloride, a generic drug for bladder control that was previously approved by the U.S. Food and Drug Administration in 2004.

Coming Out Ahead With AI

It turned out that PureTech’s AI had stumbled onto a perfect combination.

Trospium chloride was not absorbed into the central nervous system, but otherwise bound itself to the same receptors as xanomeline. So, this second molecule was able to counteract xanomeline in the body, while leaving xanomeline to perform its work in the brain. In addition, the newly created drug’s ability to reduce delusions and hallucinations proved useful in a separate disease, schizophrenia.

These results were presented in a landmark Phase 2 trial in 2019.

Meanwhile, the business side of PureTech was also at work. The company spun out this division as Karuna Therapeutics, which Bristol-Myers acquired late last year for a stunning $14 billion. In turn, Bristol-Myers would finalize approvals with the U.S. Food and Drug Administration, which it received for schizophrenia.

It’s hard to overstate how important this drug, now known as Cobenfy, will become.

Cobenfy is considered the first medication for schizophrenia with a novel mechanism of action in more than 30 years. Analysts at Cantor Fitzgerald forecast Cobenfy to generate more than $1 billion in annual revenue by 2026.

In addition, Bristol-Myers plans to retest Cobenfy for its original purpose of treating Alzheimer’s, as well as bipolar disorder. Stifel analyst Paul Matteis believes that could help the drug achieve peak annual sales of $10 billion, which would suggest total lifetime sales north of $100 billion. If that were the case, Bristol-Myers’ initial $14 billion outlay would look like a rounding error.

All this was made possible by AI-powered drug development, and we foresee even greater innovations to come over the next decade as this technology improves.

Lilly – the original developer of xanomeline – has since become a leader itself in AI-powered drug discovery. That makes sense. They’ve seen one AI-developed blockbuster slip through their fingers… and are determined to avoid repeating that error again.

But Lilly’s loss is Bristol-Myers’ massive gain. The FDA’s approval of Cobenfy marks the start of a new chapter for the company. Investors may not fully appreciate the impact. Cobenfy is already a blockbuster drug, with the potential to become an even larger blockbuster.

As such, this new therapy is a great first step toward offsetting the “patent cliff” Bristol-Myers is facing.

Many of the company’s leading drugs are losing U.S. patent protection. Specifically, Eliquis, Opdivo, and Yervoy fall off patent during the next three years. Those three drugs, by themselves, account for more than half of Bristol-Myers sales.

That’s why investors have been steering clear of the stock. But even as revenues from these legacy drugs trend lower, the company’s “Growth Portfolio” of newly approved therapies is trending higher. Growth Portfolio revenues are growing more than 20%, year-over-year. Cobenfy’s approval will accelerate that trend.

A promising pipeline of additional drug therapies will likely add to this momentum. Therefore, taking into account both the dwindling revenues from legacy products and growing revenues from new products, Bristol-Myers is on track to post adjusted earnings per share of about $7.10 this year, then continuing to trend higher in the out years.

At that level of profitability, the stock is trading for a miserly eight times 2025 estimated earnings, while yielding more than 4.3%. I do not expect that depressed valuation to persist for long, especially not if other potential blockbusters in the Bristol-Myers pipeline gain approval.

Stock No. 7: Royalty Pharma Plc

Now that the healthcare industry has entered the “Age of AI,” the opportunities to capitalize on it are popping up like weeds in a garden, or perhaps like bacteria in a Petri dish.

The biotech sector, in particular, is offering a compelling and timely opportunity. But investing in this high-risk sector can be a confusing and challenging endeavor.

A unique company named Royalty Pharma Plc (RPRX) removes some of the risk and confusion from the equation. As its name implies, the company manages a portfolio of royalties on both approved and development-stage drugs.

Typically, Royalty Pharma obtains royalties on a specific drug in exchange for providing financing to a university or pharmaceutical company. But sometimes, it simply purchases an existing royalty.

The company’s royalty partners include academic institutions like University of California, Los Angeles and New York University, as well as leading pharmaceutical firms like Sanofi SA (SNY), Pfizer Inc. (PFE), AstraZeneca Plc (AZN), and Merck & Co. Inc. (MRK).

Royalty Pharma is the largest company of its type, by far. In royalty deals above $500 million, it has a massive 77% market share. Including the small deals under $500 million, the company’s share drops to 53%. But the No. 2 small-deal royalty investor only has a 13% market share.

Importantly, Pharma is not merely dominant; it is enormously successful. Since going public in 2020, the company had invested $13 billion by 2024 to acquire royalties on 34 unique therapies, 17 of which are either currently or projected to be blockbusters.

The New York-based company’s royalty-based business model generates exceptionally high profit margins. Last year, for example, the company’s $3 billion of portfolio receipts produced $2.7 billion of portfolio cash flow, equivalent to a margin of 89%. On an earnings-per-share basis, the company posted net income of $1.88 last year. The stock is also yielding 2.8%.

Looking ahead, Royalty Pharma’s sales and profits should continue to grow as the development-stage drugs in its portfolio gain approval. Currently, it holds a total of 49 royalties, 35 of which are for approved drugs and 14 for development-stage drugs.

Additionally, RPRX continues to expand its pipeline by purchasing royalties on promising drugs in development.

During the last two years, for example, the company added royalties on eight therapies, including incremental royalties on a blockbuster drug called Evrysdi – a prescription medicine developed by Roche Holding AG (RHHBY) to treat spinal muscular atrophy (SMA) in children and adults.

Other notable royalty purchases include:

- A 5.1% royalty on Adstiladrin from the Swiss company Ferring Pharmaceuticals. The FDA approved Adstiladrin in late December 2022 as a gene therapy for BCG-unresponsive non-muscle invasive bladder cancer. This royalty will increase to 8% this year.

- A 9.15% royalty on Skytrofa, the first FDA-approved growth hormone therapy, from Ascendis Pharma A/S (ASND).

The frenetic M&A activity in the biotech sector adds an additional tailwind to Royalty’s profit growth. That’s because a takeover often accelerates the development timeline of drugs that are subject to royalties the company owns.

For example, immediately after Bristol-Myers purchased Karuna in 2023, it fast-tracked development of Cobenfy, the new schizophrenia treatment that gained FDA approval in September. RPRX holds a 3% royalty on the first $2 billion of potential Cobenfy sales, and a 1% royalty thereafter.

The recently announced Novartis AG (NVS) takeover of MorphoSys AG (MOR) also could accelerate development and commercialization of therapies where RPRX holds a royalty. Notably…

- A 3% royalty on the worldwide sales of Pelabresib, a novel and potentially practice-changing treatment option for patients with myelofibrosis.

- A 3% royalty on the worldwide sales of Tulmimetostat, an early-stage investigational therapy for patients with solid tumors or lymphomas.

Looking ahead, the company plans to invest another $10 billion to $12 billion in new royalty deals over the next five years. But it will also spend a few dollars buying back stock.

As Royalty Pharma CEO Pablo Legorreta stated…

Our priority, as we’ve said multiple times in the past, is to actually make great investments because that’s what’s going to drive growth and value creation for all of our investors, including ourselves.

But then what we have also seen is a big disconnect in the intrinsic value of Royalty Pharma, our portfolio and our ability to continue to generate value by deploying capital, and that was what prompted this $1 billion share buyback program…But we are obviously going to prioritize going forward new royalty investments over buying back shares.

Despite the management team’s impressive track record, and the company’s earnings growth trajectory, the stock seems conspicuously undervalued. It is trading for less than six times this year’s estimated adjusted earnings per share of $4.39.

For perspective, that brutish valuation is less than one-quarter the valuation of the S&P Pharmaceutical Index. This gaping valuation disparity will not last.

Moving Forward

I’m so glad that you decided to further your journey to wealth by joining Smart Money.

While these seven stocks are sure to fortify your portfolio in 2025 and beyond, those aren’t the only benefits of this free e-letter…

Nearly every Monday, Wednesday, Thursday, and Saturday, you’ll receive an email from me or Thomas Yeung, wherein we’ll share insights on the latest market “megatrends,” how to hedge against inflation, which stocks you should avoid, and more.

Get started by visiting your Smart Money website here.

Regards,

Eric Fry