Shares of Micron (NASDAQ:MU) have been bludgeoned over the last six months. Since topping in late-May near $64, MU stock is down almost 50%. That’s terrible performance, but underscores an important theme: A low valuation is not the sole catalyst to a higher stock price.

All too often I hear and read investors pushing the “cheap stock” angle as a reason to buy a stock. However, just because a stock is cheap does not mean it’s something we should buy. In fact, all too often a cheap stock is cheap for a reason — and it can continue to get cheaper over time.

This doesn’t mean we should ignore cheap stocks. Take AT&T (NYSE:T) or JPMorgan (NYSE:JPM) for instance. I own both of these stocks for their dependability and their yield. JPM is yielding over 3% with a low valuation and solid growth, while T is yielding over 6% with solid free cash flow and a low valuation, making them compelling to me.

However, stocks like General Motors (NYSE:GM), Ford Motor (NYSE:F) and Micron continue to fall despite these low valuations.

All of this is to say that the valuation is a part of the thesis, not the thesis. We have to take in various factors and considerations when looking at a stock. Otherwise, we may very well end up holding onto a stock that keeps getting cheaper.

Is MU stock one of those stocks?

Evaluating MU Stock

It’s no secret that MU stock is one of the cheapest names in the market. That’s because, historically, the company has been very cyclical as it rides the continuous boom-bust waves of the memory market. Part of that equation is demand from end users — DRAM and NAND buyers — but another factor is supply.

Micron and Samsung make up a majority of the DRAM business, which represents about 70% of Micron’s revenue mix. The rest is from NAND, where Micron competes with Samsung, Toshiba, Western Digital (NASDAQ:WDC

) and Intel (NASDAQ:INTC). If these companies produce too much product for either market (NAND or DRAM), it lowers price, which hurts these companies’ margins. And that’s how Micron ends up in these boom-bust cycles.

But because of continuous demand and tight supply, Micron has benefited from a ballooning revenue base. Two big buyers of DRAM are Cisco Systems (NASDAQ:CSCO) and Hewlett Packard Enterprise (NYSE:HPE).

When answering a question from Katy Huberty, managing director of the research division at Morgan Stanley (NYSE:MS), during the company’s most recent conference call on Dec. 5, HPE president and CEO Antonio Neri said, “Ultimately the elevated DRAM price is still there, although now started declining.” Earlier in the call, CFO Tarek Robbiati said that “DRAM costs have peaked and are starting to come down.”

On Nov. 14, Cisco CFO Kelly Kramer said, “We bought inventory ahead. We did everything we could to try to minimize the impact [of memory prices]. We had big purchase commitments and we are still seeing year-over-year price increases in this quarter.” She added that memory prices are still a bit of a headwind, but expects this to become a tailwind in the second half of Cisco’s fiscal year.

Valuing MU Stock

So what does all of this mean? It means that Micron will probably have a good quarter when it reports on Tuesday, Dec. 18 after the close, but guidance is vulnerable. Ultimately, that’s the problem. Investors keep thinking the story for Micron is over and, as a result, they have one foot out the door.

Hence, valuation has not supported the share price. MU stock currently trades at 3.5 times earnings. Estimates now call for an 18% earnings decline this year and a 12% decline in fiscal 2020 — this despite just a slight decline in sales this year and next year, meaning margins are expected to come under significant pressure. At what point, though, is that priced in?

Any sort of better-than-expected future outlook should lift the stock, given its dire valuation.

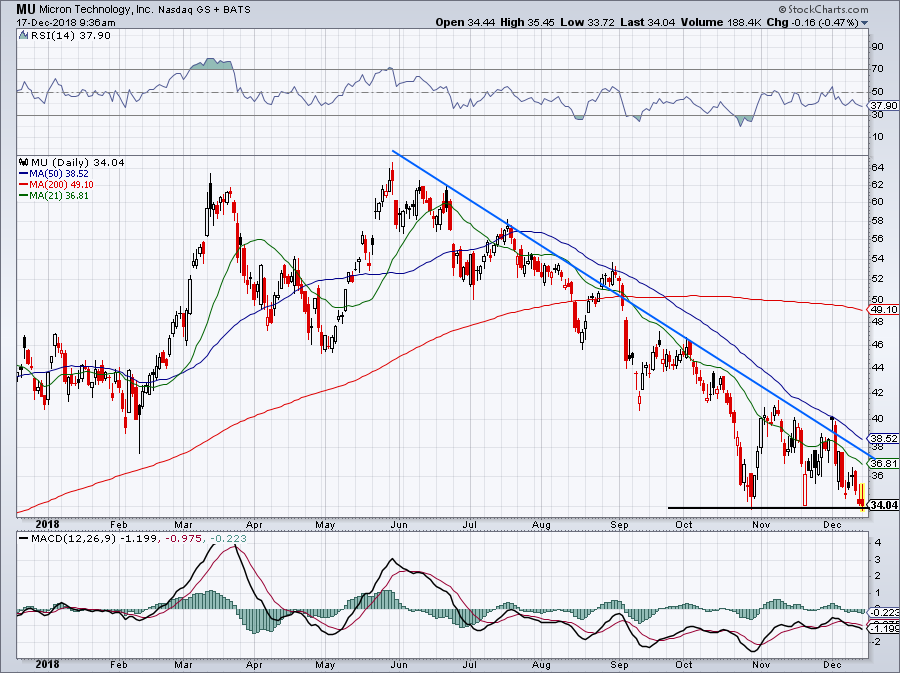

Trading Micron Stock

Click to Enlarge

MU stock remains locked in a brutal downtrend. I certainly don’t love that resistance (blue line) is squeezing Micron into support (black line). One of these two marks will have to give way. The question is, which will it be?

Below $34 and MU stock is in trouble. Over downtrend resistance and the 50-day moving average, and bulls can get optimistic again.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long JPM and T.