There is a common pattern in new technology cycles, and it goes like this:

The innovation itself appears. Then, a bottleneck emerges. Next, capital floods in to solve the problem. Finally, the regime changes.

We saw this “regime change,” or complete reorganization of stock market winners and losers, in the in the dot-com bust phase.

Capital rotated out of the high-profile names and into a variety of other sectors, including base metals, precious metals, energy insurance, and utilities. Those sectors delivered solid double-digit or triple-digit returns over the early part of the 2000s, even while the Amazons, Intels, and Ciscos of the world fell 80% or more.

Another regime change is happening now.

Since the early AI revolution, the Magnificent Seven companies have been sat securely on the throne. The group includes Alphabet Inc. (GOOGL), Amazon.com Inc. (GOOGL), Apple Inc. (AAPL), Meta Platforms Inc. (META), Microsoft Corp. (MSFT), Nvidia Corp. (NVDA) and Tesla Inc. (TSLA).

But their seat is soon to be usurped. We are starting to see a rotation out of some of the highest profile, high beta tech stocks and into more real-world, asset-backed sectors.

Let’s look at a singular, but powerful, example: In the past six months, Corning Inc. (GLW) – a supplier of the data center buildout – is up 81%. On the other hand, Nvidia – a customer of Corning – is only up a 4%.

Investors are rotating away from AI chips and toward AI picks and shovels. Corning is essentially the “glass backbone” of AI data centers, which is why investors are rediscovering it.

The fiber-optic, hard-asset company is eclipsing the gains of the Wall Street darling with ease. Nvidia would need huge upside surprises to keep rising, while Corning simply needs to show steady AI-driven growth.

That’s a Mag 7 killer.

This dynamic will only increase as we move forward. That means it’s important to own the companies that are providers or suppliers to this massive AI buildout, rather than the companies that spending the money to do build.

And this regime change will soon shift into high gear.

That’s why, inside this report, I list three of my favorite stocks that are significantly outperforming the Mag 7 so far this year.

These “asset heavy” companies are a bellwether of the regime change that I predict will soon kick off after the next wave of earnings announcements from the AI hyperscalers.

Now, I want to be clear that I am not listing these companies as “Buy” recommendation today. Rather, I believe they will rise in rank as Big Tech household names continue to fall and, therefore, deserve our attention.

Let’s dive in…

Mag 7 Killer No. 1: A Prolific Energy Producer

Our first Mag 7 killer is one of America’s most prolific energy producers, and it’s firmly positioned to fuel America’s AI buildout.

As the big tech companies build ever-larger and ever-more-numerous data centers, they are struggling to secure the dedicated power supplies these centers require.

Because of power bottlenecks like these – both current and prospective – Big Tech is turning to every and any possible power source to satisfy their needs.

Even nuclear power is making a comeback. Amazon, Alphabet, Microsoft, and Meta have all inked deals to obtain dedicated nuclear-powered electricity.

But nuclear power alone won’t solve the problem. “Not in my back yard” issues, coupled with the lengthy permitting and construction process, ensure that nuclear power will not become more than a partial solution.

That’s why these big tech companies are also implementing an array of other power-generation technologies – ranging from solar-plus-storage to hydrogen fuel cells to natural gas “peeker plants.” Even geothermal systems are powering some data centers.

Natural gas is the clear winner in the push to generate power directly at data centers

According to a recent report by Cleanview, a market intelligence platform, nearly 75% of the power equipment planned to be used on site at data centers is natural gas.

The natural gas market offers three major advantages over competing technologies…

- It is abundant.

- It is cheap, especially in the Delaware Basin, one of the world’s most productive oil and gas regions located in West Texas and southeastern New Mexico.

- It is a proven technology with relatively rapid permitting processes.

Data center demand for natural gas could become especially acute in the Delaware Basin, with a new “Data Center Alley” potentially blossoming in the region.

That brings me to Devon Energy Corp. (DVN).

As one of the leading producers in the Delaware Basin, Devon is well-positioned to benefit from structurally improving pricing trends in the region.

For the last few years, the Delaware Basin has been rapidly boosting its production of both oil and gas. Unfortunately, gas volumes have overtaken pipeline capacity. As a result, much of the gas from the Delaware Basin is “stranded” — the oil and gas industry’s polite way of saying “worthless unless you can move it.”

Producers flared it. Trucked it. Discounted it to oblivion. As such, the Delaware Basin has behaved for years like a brilliant student stuck in detention. It held enormous potential, but had no way to express it.

But detention is ending.

Two major pipeline projects are improving the economics of the Delaware Basin, especially for Devon.

First came the Matterhorn Express, a 580-mile pipeline capable of moving 2.5 bcf/day from Waha to the Houston area. Devon secured long-term transport capacity from this pipeline, once it entered service earlier this year.

Next comes the Blackcomb Pipeline, a 365-mile system that will send gas south to the Agua Dulce hub near Corpus Christi – a gateway to multiple liquefied natural gas (LNG) terminals. Together, these infrastructure upgrades give Devon a direct highway to premium Gulf Coast pricing.

This pipeline capacity would not only accommodate all of Devon’s current gas production in the Delaware Basin, but also leave meaningful headroom for future growth.

Devon did not stumble into this moment. It spent years preparing for it. The 2021 acquisition of WPX Energy gave the company a massive 400,000-acre footprint in the Delaware Basin. From there, Devon methodically built midstream relationships, invested in gathering and processing, and co-funded critical pipeline capacity – all while retiring nearly $1 billion of debt and returning hundreds of millions of dollars to shareholders.

Its fundamentals are also solid. The company recently beat fourth-quarter earnings estimates. It performed exceptionally well on the production side, although it warned that several major winter storms would cut production for the first quarter.

Still, that hasn’t stopped the oil & gas company from outperforming the hyperscalers that require the kind of power that Devon provides.

The Roundhill Magnificent Seven ETF (MAGS), the ETF that tracks the Mag 7 companies, is down around 6% since the start of the year. In contrast, Devon is up over 20% year-to-date.

The bottom line is that AI-driven power demand is quietly rewriting the natural gas story, and Devon is positioned to thrive. In a market obsessed with the digital future, Devon represents something rarer: a hard-asset business, finally unshackled, standing at the center of a real-world demand shock.

Mag 7 Killer No. 2: An Oil & Gas Offshore Driller

Our second Mag 7 killer is a leading global offshore contract drilling company for the oil and gas industry.

Now, oil prices certainly impact the fortunes of offshore drilling companies, but offshore drilling activity does not necessarily mirror oil prices day-by-day. Instead, oil companies contract with driller companies in order to pursue their multi-year exploration and production goals.

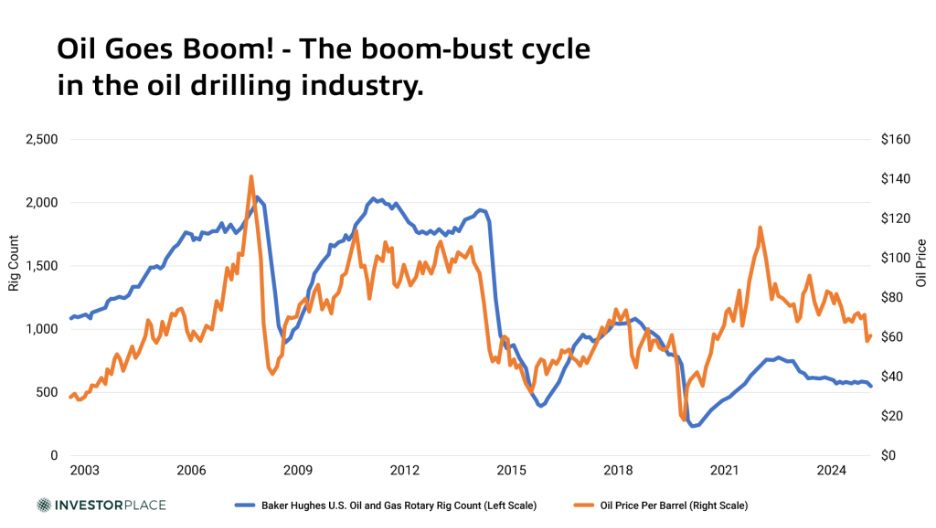

That said, oil drilling tends to be a deeply cyclical industry that oscillates from boom-time conditions to bust-like ones, or even actual busts.

The current reading of 551 rigs is less than a third of the number that were operating at the 2014 peak. The chart below illustrates the cyclicality of oil drilling over 20 years, from 2003-2024.

but it also shows how rapidly trends can reverse. For example, during the oil market lows of 2010 and 2016, drilling activity rebounded abruptly and powerfully.

History may be on the verge of repeating itself, which is why I consider Valaris Limited (VAL) to be an excellent speculation.

Despite the feeble price trends in the crude market, Valaris has been posting impressive revenue and earnings for several quarters… and anticipates continuing growth.

On an annual basis, Valaris’ revenues have risen 33% since 2023, while gross earnings (EBITDA) have quadrupled. Despite these solid results, however, the stock has not moved as high as you would expect. It “roundtripped” from $60 in early 2023 to a peak of $80 in 2024 before plummeting below $40. Only recently have markets begun to realize its value.

The company’s recent blockbuster merger announcement could create the most powerful deep-sea drilling company in history. In early February, Valaris received a takeover offer from rival Transocean Ltd. (RIG).

Under the terms of the $5.8 billion takeover, Valaris shareholders will receive 15.2 shares of Transocean stock for each share they own – a roughly 32% premium based. Upon completion and on a fully diluted basis, Transocean shareholders will own approximately 53% of the combined company, with Valaris shareholders owning the remaining 47%.

The deal will create the world’s largest offshore rig contractor by market value, as well as by number of rigs – with an offshore fleet of 73.

I anticipate Valaris to be one of the bellwethers of the regime change. The offshore driller is already up over 80% in the first three months of the year. I expect Valaris shares to continue gaining ground over the months ahead.

Mag 7 Killer No. 3: An International Mining Company

Our third and final Mag 7 killer is a company digging up the one material that every AI data center needs: copper.

Copper has always been the wiring of the world. But suddenly, the world is demanding more wiring than it has at any point in history. Every macro trend that feels futuristic, electrified, digitized, or decarbonized runs straight through a fat bundle of copper.

- Power grids and data centers. The International Energy Agency (IEA) expect global power demand to grow by more than 3.5% per year on average over the rest of this decade, as AI data centers, semiconductor fabs, and other large industrial loads connect to the grid.

- U.S. utilities. According to Morningstar and the Edison Electric Institute, utilities are entering a CapEx “super-cycle,” with roughly $1.1 trillion planned between 2025 and 2029 and about $1.4 trillion expected by 2030 – nearly double the investment of the prior decade as utilities expand to meet surging demand from AI data centers.

- AI and cloud computing. A modern hyperscale data center is essentially a copper-and-aluminum exoskeleton wrapped around racks of silicon. These facilities consume enormous volumes of copper wiring, busbars, and switchgear. Estimates suggest data centers alone could require hundreds of thousands of tonnes of copper per year by 2030, with individual AI-focused hyperscale facilities consuming up to 50,000 tons each.

- Not surprisingly, the copper market is tilting toward long-term deficits.

Looking down the road, the IEA’s latest critical-minerals outlook cites copper as one of the biggest “problem children” in the commodity world. Even if every currently announced copper project advances into production, the IEA still sees a 30% supply gap by 2035.

But while demand accelerates at a breakneck pace, the copper supply faces daunting structural constraints…

- Declining grades. Ore grades at many of the world’s big mines have been falling for years, forcing producers to move more rock to generate the same amount of copper.

- Long lead times. The IEA estimates it takes 17-19 years on average to move a copper discovery from exploration to full production. That timeline does not shrink just because AI demand surged. Arizona’s $10 billion Resolution Copper project illustrates the point: Discovered decades ago, it still will not enter production until around 2030.

- Rising costs. New projects are getting more expensive, more remote, more politically sensitive, or all three. Environmental reviews, community opposition, and infrastructure needs add billions of dollars to project timelines.

- Concentrate bottlenecks. Even where mine output is growing, smelting and refining capacity is becoming a bottleneck. The International Copper Study Group (ICSG) expects refined copper supply growth to slow toless than 1% in 2026, turning a modest 2025 surplus of 178k tons into a 150k-ton deficit.

The IEA’s conclusion is blunt: Copper is one of the most vulnerable links in the global supply chain for the energy transition and AI build-out. Without more than $200 billion of new investment, the world simply won’t have enough copper.

So, the short-term story is simple; demand is growing faster than expected, supply is growing slower than expected, and the market is already slipping into deficit.

Freeport-McMoRan Inc. (FCX), a metals mining company with a focus on copper, is maximizing this opportunity by boosting copper production in every way possible. For example, the company has developed cost-effective methods for extracting commercial quantities of copper from waste rock through advanced leaching techniques.

Freeport uses AI to optimize ore sequencing, mill throughput, equipment uptime, and geological modeling across massive copper operations. Algorithms improve recovery rates, reduce energy consumption, and minimize downtime.

Because mining is capital intensive and operationally complex, small efficiency gains can scale into enormous dollar impact. AI helps Freeport decide which rock to move, how fast to process it, and when to service machinery.

The company also applies machine learning to geological data, improving reserve estimates and guiding long-term mine planning.

This is applied intelligence in its purest form: more output from the same ore body, with fewer people and lower costs.

For 2026, Freeport expects 3.4 billion pounds in copper sales, with a ramp in production to 800 million pounds by 2030. That level of production would drop about $1.6 billion to the bottom line.

While the hungry, hungry Mag 7 companies that eat up Freeport’s copper are in the red as a whole, Freeport is up over 20% year-to-date – and will continue to benefit from the feeding frenzy.

A small portion of the coming regime change has already taken place. Valaris’, Devon’s and Freeport’s killer gains over the Mag 7 prove just that.

Regards,

Eric Fry